Market Data Bank

Click image to enlarge

Despite months of frightening financial headlines, the third quarter ended with the stock market only -1.6% off its all-time record high.

Including the bear market plunge suffered last Christmas, when the value of the Standard & Poor's 500 index decline bottomed with a -19.8% loss from its previous high. The index of America's largest public companies, over the 12 months ended September 30th, returned +2.2%.

That's not much for a 12-month return. Since 1926, when a monthly record of common stock prices was first tracked systematically, stocks have averaged about a +10% average annual rate of return.

But that's just a bad snapshot to look at, as we will discuss in the next minutes.

In the first three quarters of the year, the S&P 500 returned +19%, overcoming a rising tide of fear about the trade war with China, an inversion of the yield curve, a growing chorus of recession predictions, and political crisis.

Click image to enlarge

Maybe a good place to start is by noting that the stock market did not drop on worries about the China trade confrontation, manufacturing slowdown, or on concerns about the U.S. political situation - the major bad-news narratives currently haunting markets as Halloween sweeps by fast.

All three stock market drops in the past year followed Federal Reserve Board pronouncements.

Since the Fed backed off its forecast for rising rates and inflation in January, consumer spending and income have been about as strong as they have ever been in post-War American history!

For months now, the actions of the Federal Reserve, as it works to extend the economic expansion into 2020, have driven the stock market - both up and down.

Point is, it's always been wise not to get emotional about the news affecting markets, which may seem so dismal at any bleak moment in history.

The +2.2% return over the 12-month period is a great example of how one snapshot of stock returns may be way below historic norms, but always comes back.

While past performance is not indicative of your future returns, we believe the long arc of history gives you a framework for modeling the future based on economic fundamentals.

That's what we will try to impart in this brief presentation.

Click image to enlarge

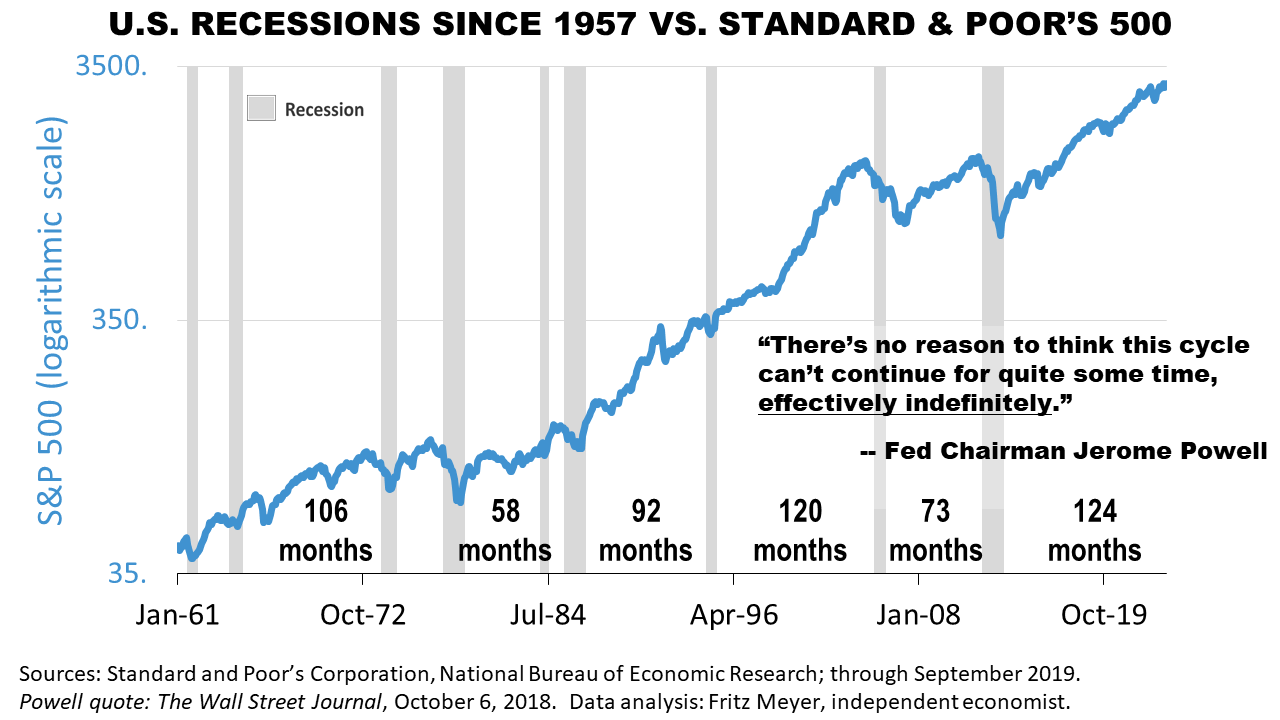

At 123 months, this is the longest business cycle in modern history, and growth of about +1.8% is sustainable as long as the Fed does not make a policy mistake, which is always possible.

Fed mistakes have caused every recession in modern history.

A Fed mistake in December 2018 caused the inversion of the yield curve!

Fortunately, the Fed quickly recognized its policy was not working and eased rates twice by a quarter point since then.

The Fed is what matters most in the current situation.

One important but subtle trend illustrated in this chart is that the nation's central bank has been able to lengthen the business cycle in recent decades.

Fed Chairman Powell has publicly stated that the Fed could possibly extend this current cycle of growth in gross domestic product well beyond the 123 months already achieved.

Central banks have learned how to better manage national economies, a sign of progress in the modern era that has unfolded slowly in the post-War period.

Click image to enlarge

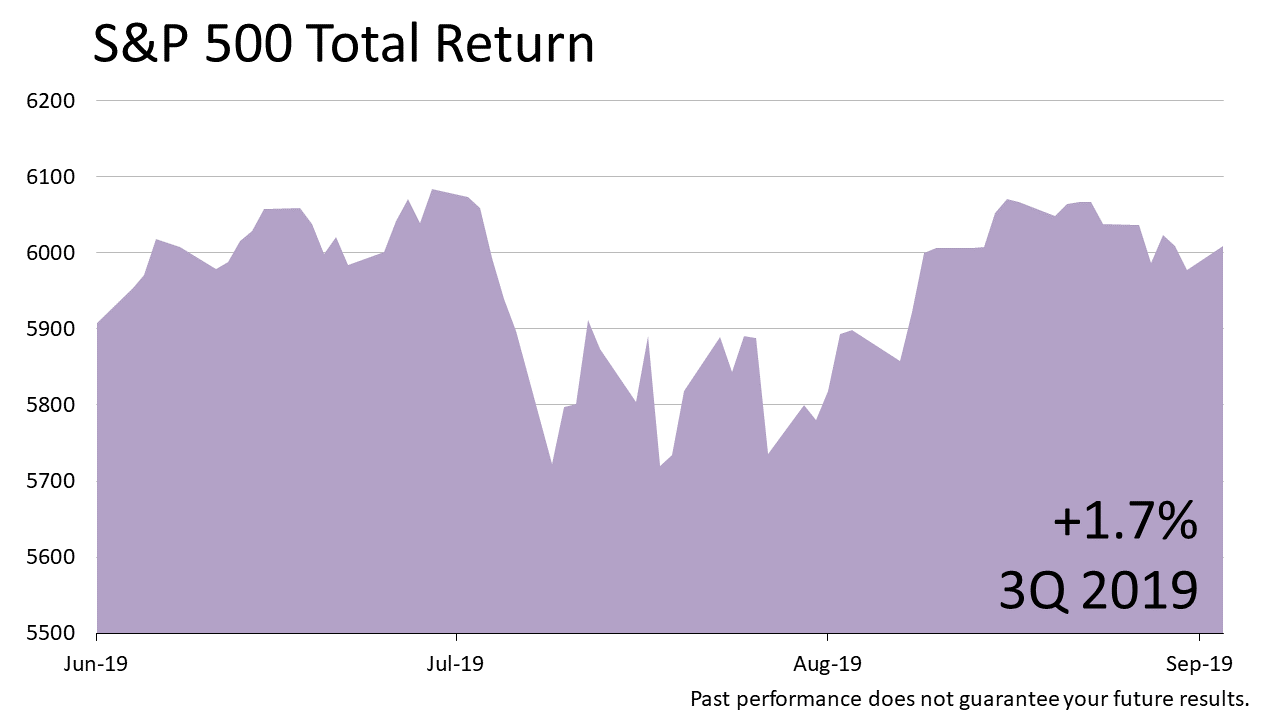

For the quarter, stocks posted a +1.7% gain. It followed a +4.3% gain in the second quarter.

Click image to enlarge

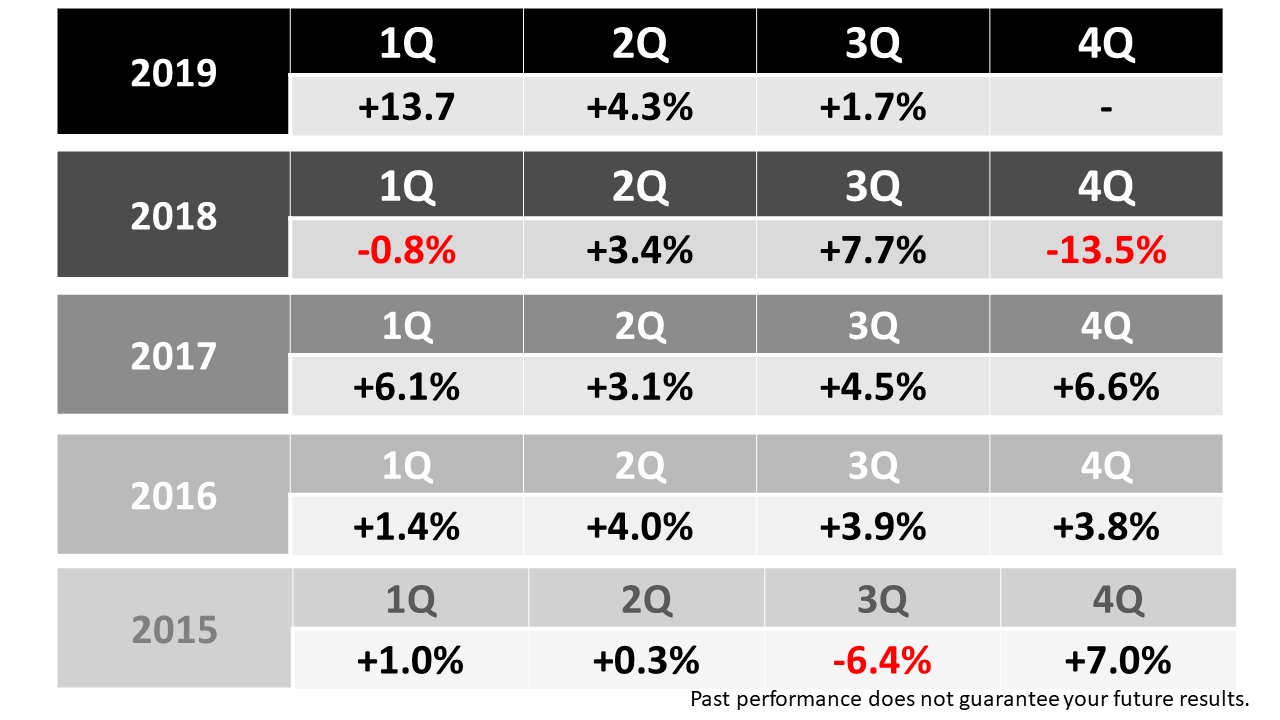

Looking back at the last the 23 quarters - five and three-quarter years - shows us how unpredictable the stock market is.

In 2015, the S&P 500, a barometer of the investment value of the largest investable companies in the United States, underperformed the average return annually since 1926 of about +10%. But the next calendar year was spectacular!

Similarly, the gigantic +13.7% gain in the first quarter of 2019 followed an equally gigantic -13.5% loss in the fourth quarter of 2018.

The unevenness of the returns quarter-to-quarter that you see here is typical of the spasmodic gains of a bull market, which are unpredictable.

Click image to enlarge

Three risks hung over markets all quarter: the trade war with China, yield curve inversion, and a manufacturing slowdown.

Let's look at those three risks.

Click image to enlarge

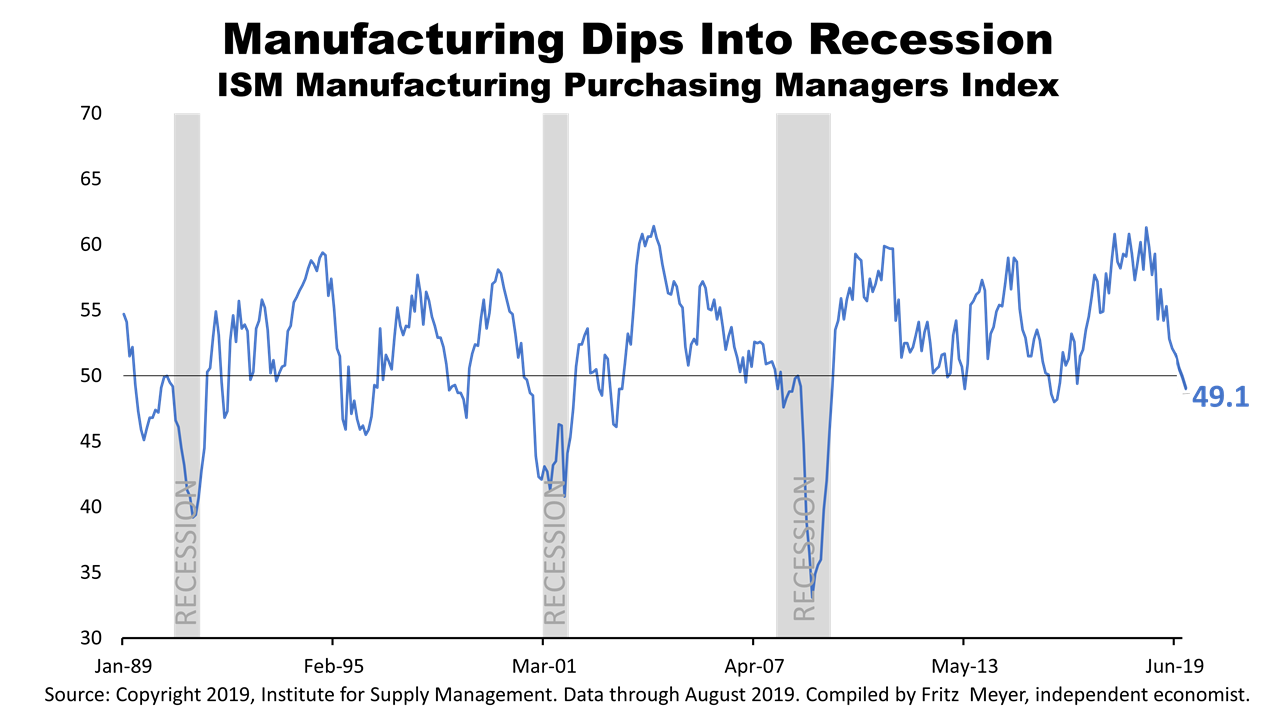

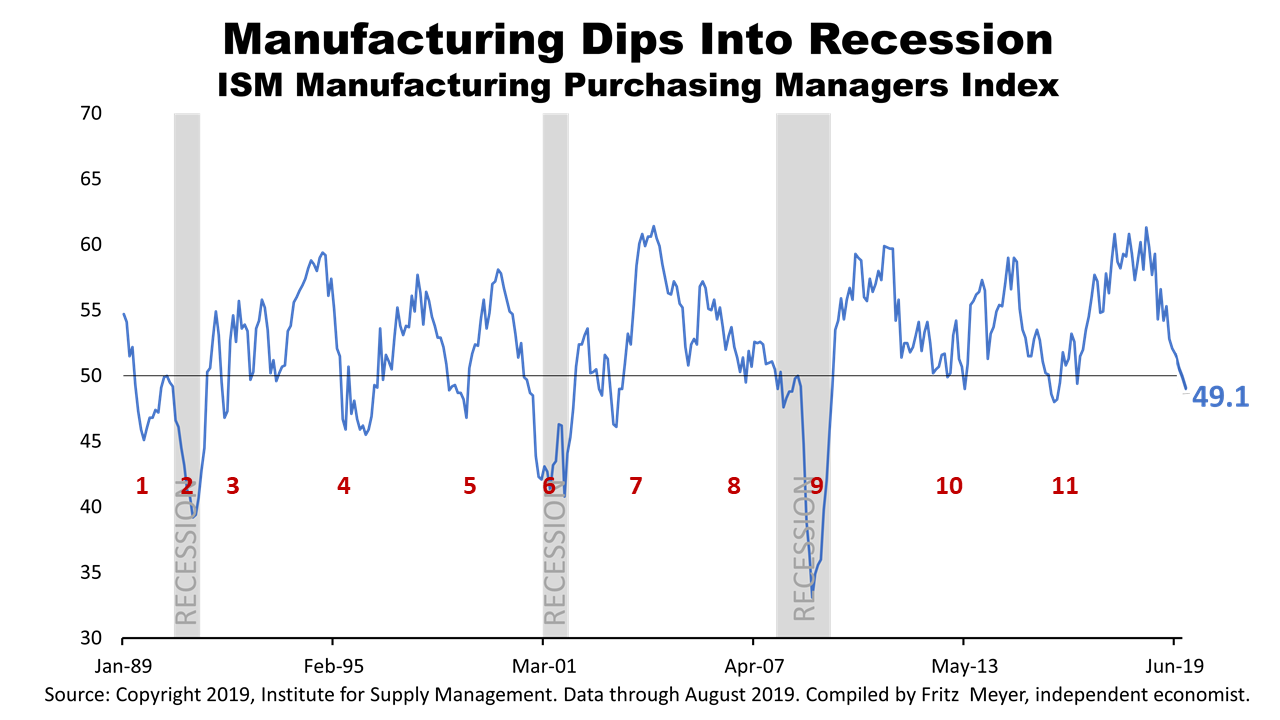

Since September 2018, manufacturing activity plunged from a record high of +61.3%.

That trend continued in July, August, and September.

Click image to enlarge

This monthly manufacturing data series from the Institute of Supply Management, which certifies corporate purchasing management professionals, is designed to signal a recession when it falls to less than 50.

It literally predicted eleven of the last three recessions!

Over the last three economic cycles, the ISM manufacturing index dipped below 50% eleven times but was followed by a recession only three times.

Rather, manufacturing rebounded after the index fell below the 50% recession signal.

This is important context missing from the press coverage.

Without that context, you are left to think a recession is right around the corner when it's not.

This was one of the three risks creating fear last quarter.

Click image to enlarge

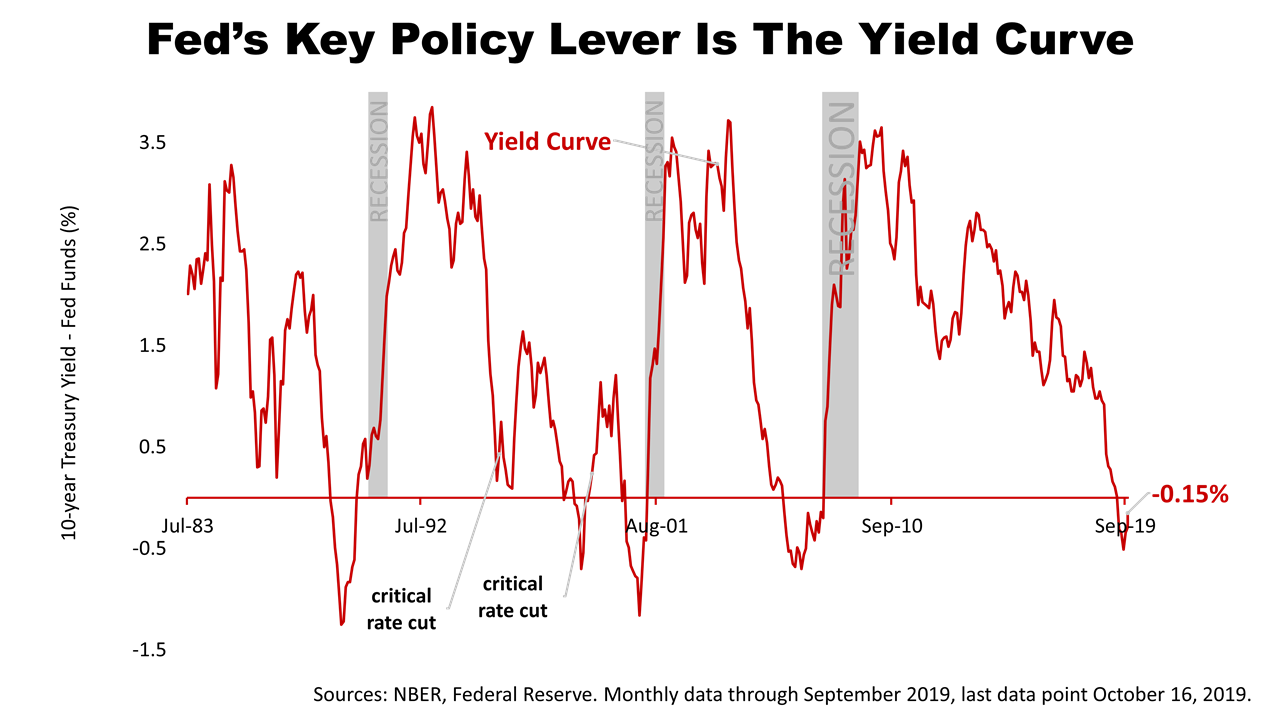

Another fear in the news in the third quarter was the inversion of the yield curve.

In the past few decades, when the yield curve inverted it was because investors saw fundamental economic measures slowing down.

So, when the yield curve inverted on Wednesday, August 14th, financial headlines turned grim.

Neil Irwin, an economics columnist at The New York Times, explained the inversion like this: "Longer-term rates below shorter-term rates are a clear signal from bond investors that they think the United States economy is on the downswing, that its future looks worse than its present."

Click image to enlarge

An inversion is when long-term bonds yield less than short-term bonds and investors are not rewarded for "term risk," the risk of owning longer-term bonds, a condition that makes no financial sense.

You should get paid more for the risk of owning longer-term bonds than risking your money for months.

While it is true that over the last several decades every recession was preceded by the inversion of the yield curve, not every yield curve inversion has been followed by a recession, and this may be one of those times.

Click image to enlarge

In 1995 and 1998, for example, the Fed changed course, cutting the fed funds rate after the yield curve inverted and averting recession.

Although the yield curve inverted in August, there was no slump in fundamentals and the Fed may have acted in time to prevent a recession.

Click image to enlarge

While the yield curve is an important economic forecasting tool, it may not be the best tool to forecast the future right now.

You don't want to be driving your car from your rear view mirror, and you don't want to use an indicator that worked in the past but may not indicate what's directly ahead!

Click image to enlarge

Look at what's really going on:

Sales at U.S. retailers fell three-tenths of 1% in September, but retail sales are volatile month to month and September was the first decline in seven months.

Retail sales excluding gasoline - because its price volatility distorts the retail sales picture - rose in the 12 months through September 30th by an astounding +4.7%!

That was the same 12-month rate of gain as in August!

And it was significantly higher than the +3.8% retail sales growth rate in July!

While the one-month decline in September was not good news, the 12-month rate is much more important in judging the trend.

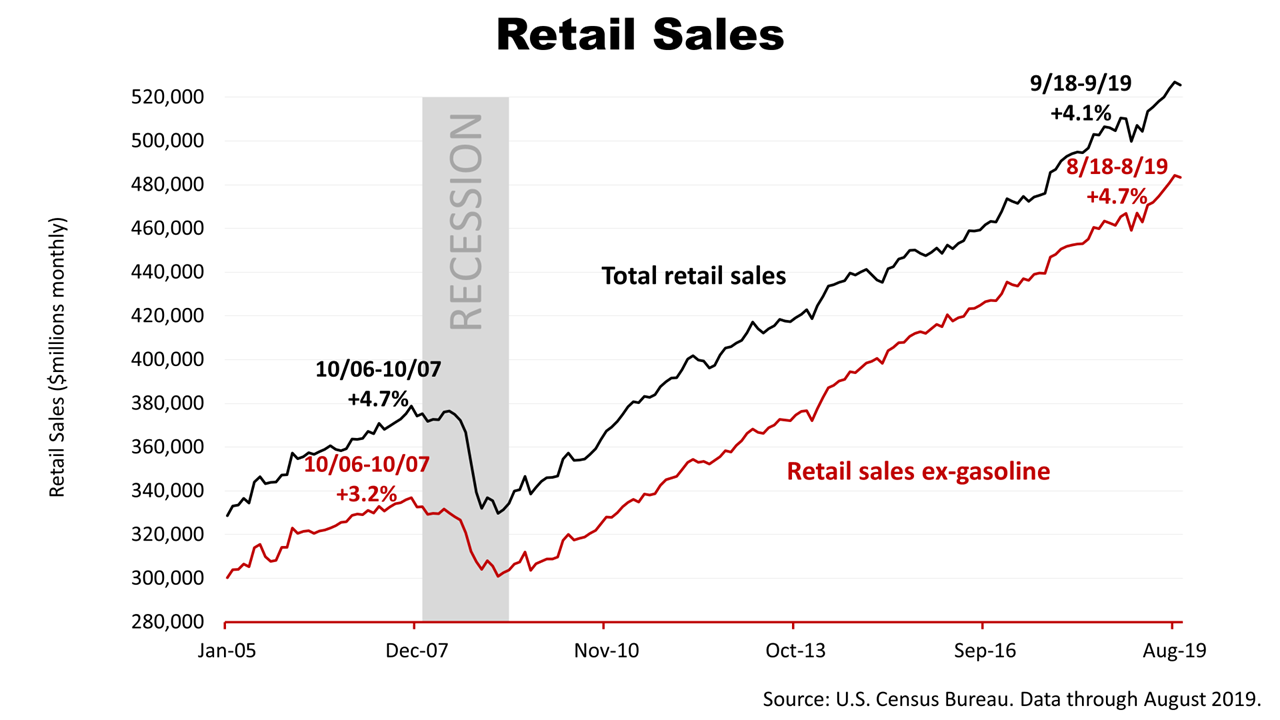

Click image to enlarge

Real retail sales after inflation, as you see in this chart, have actually been surging for many months.

Real retail sales excluding gasoline in August were up +3.2% year-over-year, from +2.4% year-over-year in July.

You just cannot have a recession when retail sales are so strong.

Click image to enlarge

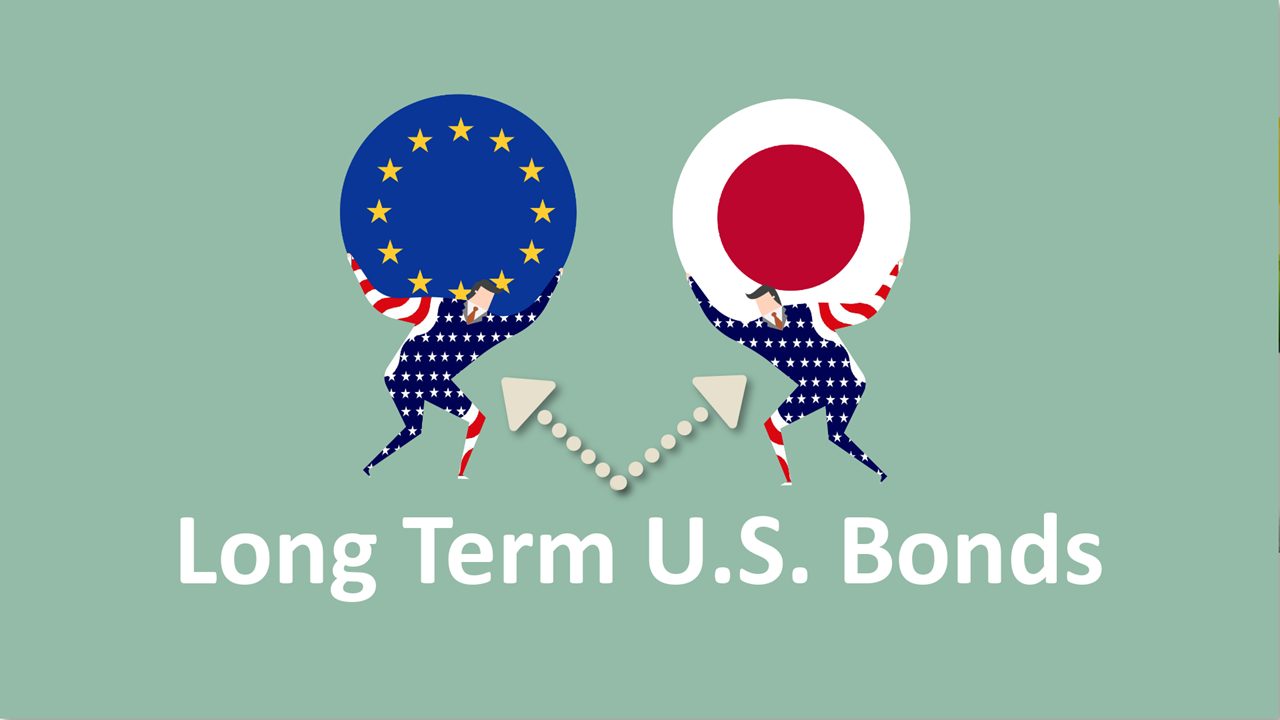

Things really are different this time, because the recent yield curve inversion is caused by an unprecedented condition:

Negative yields in Europe and Japan are depressing yields on long-term U.S. bonds - causing the yield curve inversion!

What investors expect of the economy over the next 10-years is not really bleaker than what they expect over the next three months, but negative yields in Europe and Japan have attracted capital to U.S. bonds and depressed yields in the U.S.

That makes this yield curve inversion different from those in the past.

Click image to enlarge

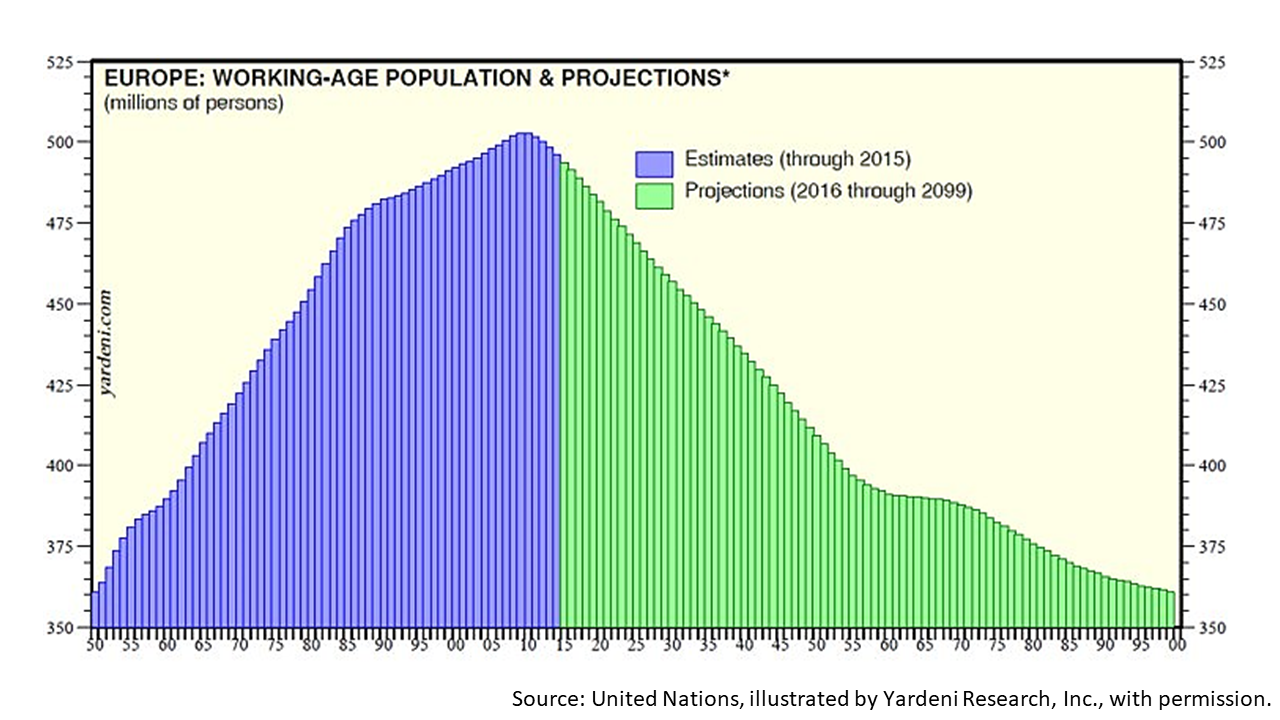

Negative yields in large developed economies across the globe - namely, Germany, India, Japan, and China - are mainly caused by the declining working-age population in these nations.

The growth of a country's labor force factors heavily into its gross domestic product.

Weak demographics have forced low rates abroad, which in turn has forced U.S. interest rates lower.

Economic conditions are not causing the low yields.

The recent yield curve inversion has been caused by financial market - investment - conditions.

While this means you can probably expect lower returns on bonds in your portfolio, it does not mean a recession is imminent.

Click image to enlarge

Investors could be in for permanently lower yields on bonds because the low-yield trend is tied to slow-moving demographic trends.

In contrast, however, the U.S. baby boom will spawn an echo-boom generation that is unique among the world's major economies. That's a strong positive fundamental economic factor to consider for long-term American investors.

Click image to enlarge

The other fear haunting investors at Halloween was the U.S. trade war with China. But the fright is worse that the bite.

Click image to enlarge

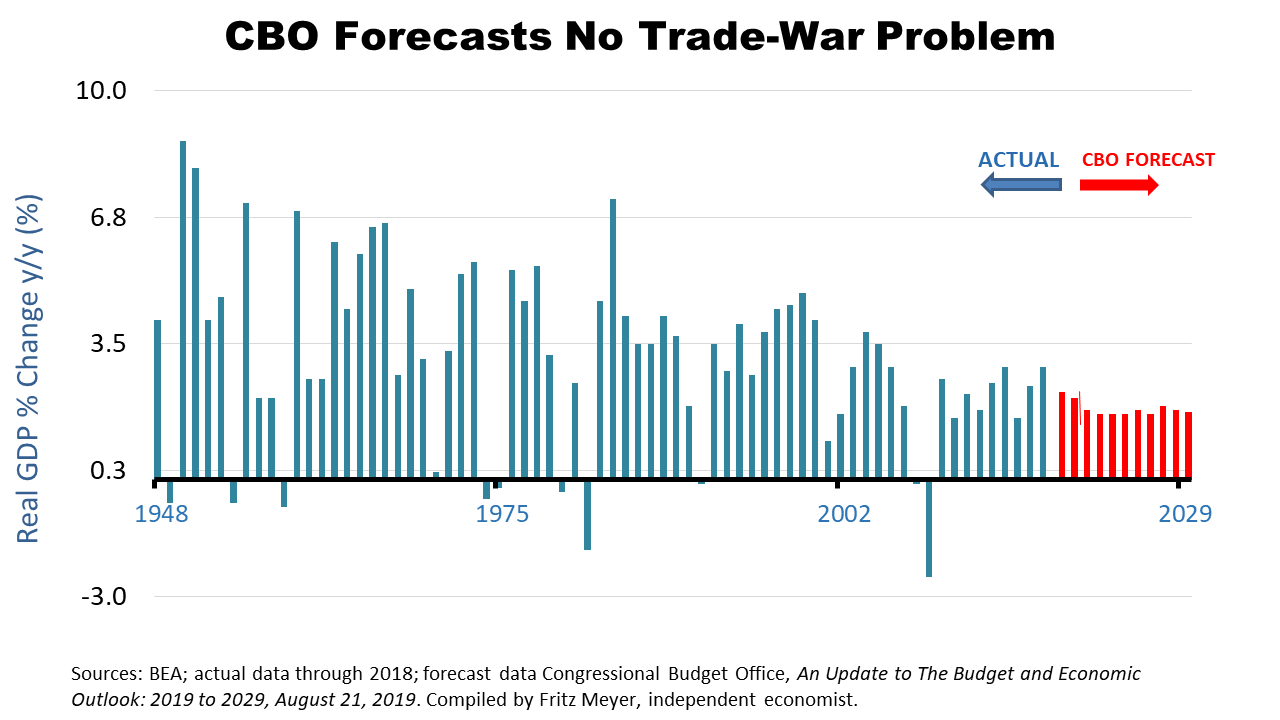

CBO is predicting the U.S. in 2019 will grow +2.3% - despite the U.S. China trade war.

To be clear, CBO publishes a 25-page report quarterly on the long-term debt and annual federal budget deficit, and it includes the 2019 growth forecast.

The latest CBO forecast confirms that the China trade war isn't about to sink the economy, though the financial press is dominated by news of the international trade clash.

This was important economic news, but it wasn't in the financial press.

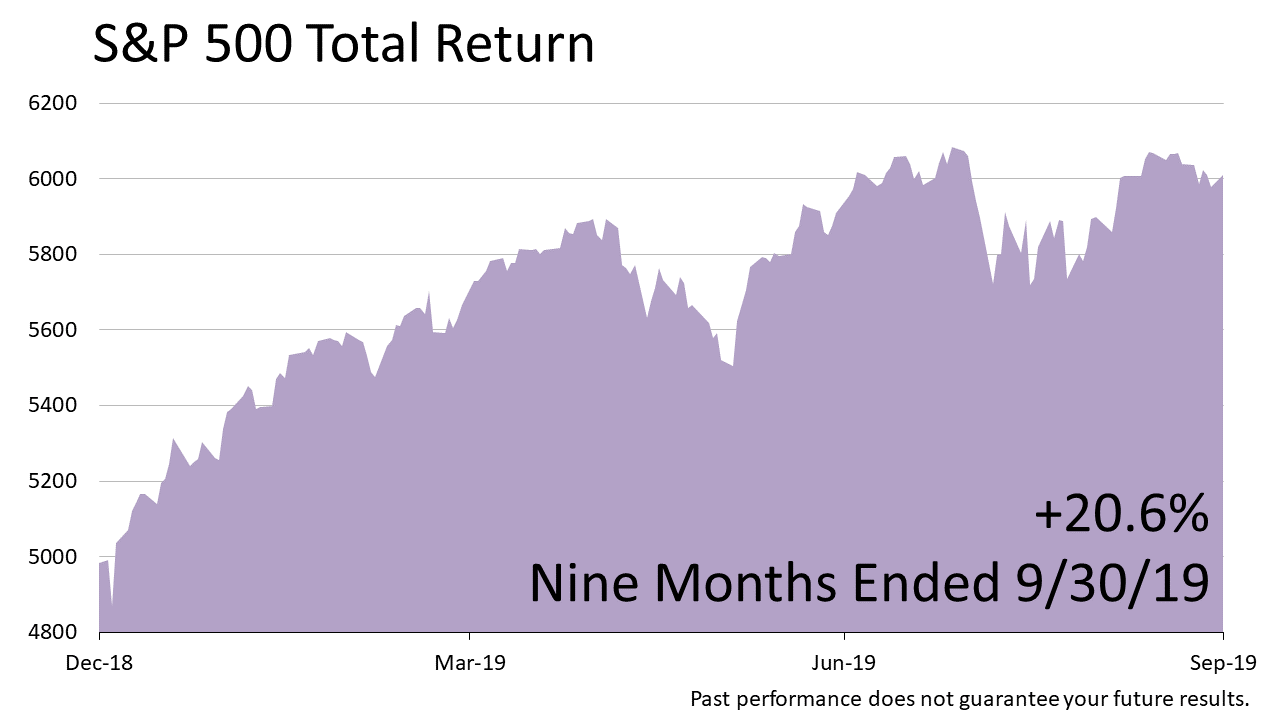

Looking at the returns of the first nine months of the year, the S&P 500 posted a +20.6% gain.

Stocks historically averaged a +10% return in the calendar years since 1926, so a +21% return in nine months is extraordinary.

However, it followed the -13.5% plunge in the fourth quarter of 2018.

Click image to enlarge

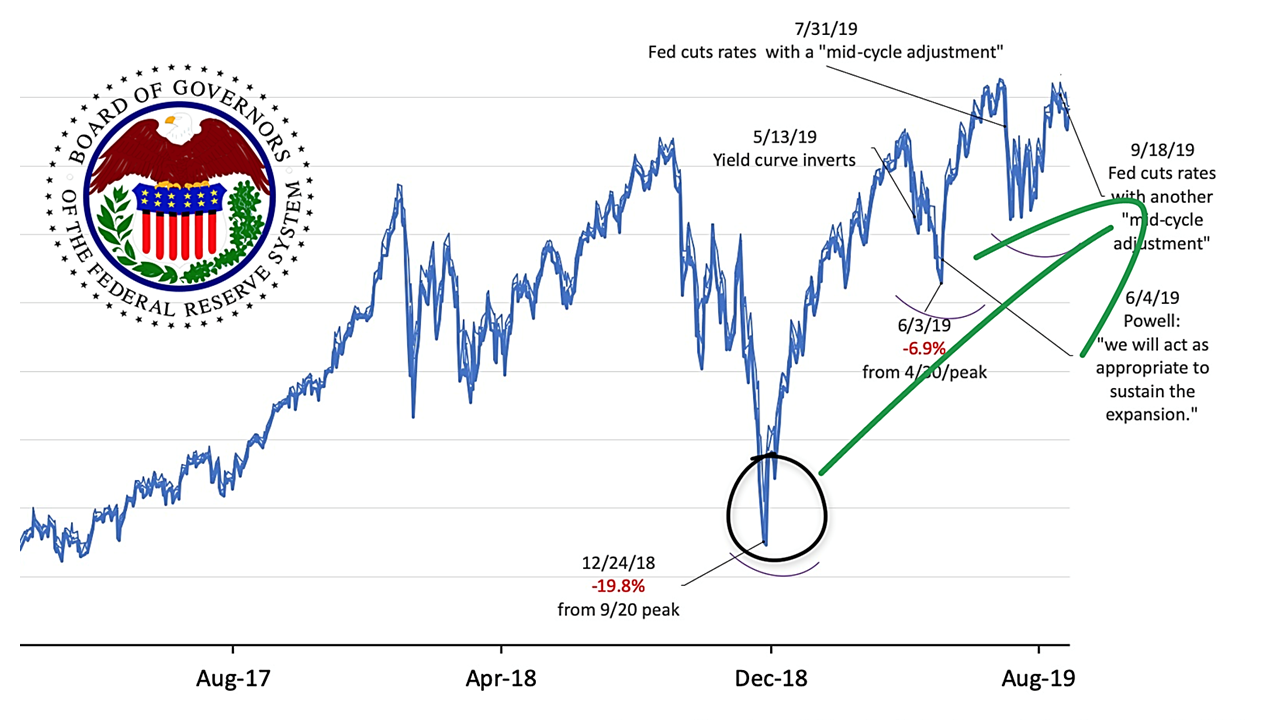

The S&P 500 had broken a new record high on September 20th, 2018, whereupon it dove to a Christmas Eve low, down -19.8%.

The plunge was exacerbated on December 19th, when the Fed raised rates a quarter point and reaffirmed its plan to raise the fed funds target rate to 3% in 2019.

Investors sold stocks in alarm on this news because hiking the short-term rate to 3% would result in an inverted yield curve, which has been the key precursor to every recession in the post-WWII era.

The Fed reversed course on January 4th, signaling that it would give up on its previously-announced 3% target rate for fed funds, the rate it lends to banks.

That buoyed markets but the December rate hike, by May 2019, pushed down long-term bond yields so low that the yield curve inverted.

That, coupled with President Trump's threat to impose tariffs on Mexican imports, took stocks down -6.9% from their April peak.

President Trump then canceled the Mexico tariff threat and Federal Reserve Bank Chairman Jerome Powell reaffirmed in June that the Fed will "act as appropriate to sustain the expansion."

Subsequently, stocks hit a new record all-time high late in July and reapproached that peak in September, as the Fed's more accommodative stance took hold.

Click image to enlarge

After trading sideways for approximately two years in 2015 and most of 2016 - hitting two air pockets during that period - the stock market broke out of its range after the November 2016 election, and it rose steadily to an all-time peak on September 20th, 2018.

Over the next three months, the S&P 500 declined on growing fears of an economic slowdown, yet the Fed announced that it would stick to its plan to hike the rate at which it lends to banks to 3% and hiked rates a quarter point on December 19th, which triggered a sharp selloff.

Selling of stocks accelerated in mid-December, and by Christmas Eve stocks had plunged -19.8% from their peak, technically qualifying as a bear market.

On January 4th, 2019, the Fed signaled rates were on hold, whereupon stocks rallied for seven months, putting in a new record high on July 26th, 2019.

In addition to the worries created by the Fed's hiking rates throughout 2018, the trade war with China added to volatility.

After the President's statement on March 1st, 2018 that "trade wars are good and easy to win," stocks often were whipsawed after the President's tweets about the details and timeline for tariffs on Chinese imports.

Over the last five years, including dividends, the S&P 500 total return index has gained +67%, compared with a gain of +51% for the commonly quoted S&P 500 price index, with the 16% difference attributable to reinvestment of dividends quarterly.

The five-year gain of +67%, or +13.4% per year, is substantially greater than the stock market's long-term annual total returns of approximately +10% going back 200 years, as described by Wharton professor Jeremy Siegel in his seminal book, Stocks for the Long Run.

However, at the close of the third quarter 2019, the S&P 500 was in line with its long-term +10% compound annual return trajectory for the past 30 years.

Click image to enlarge

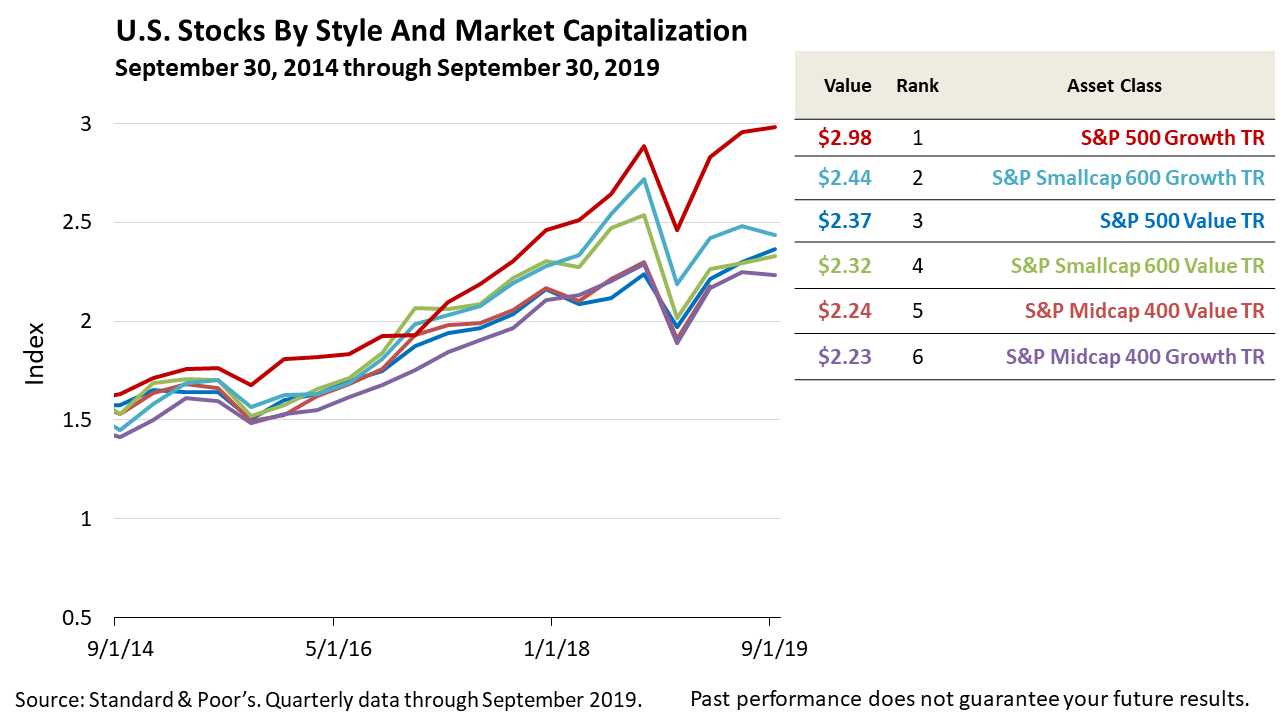

Large-company growth stocks sharply outperformed other types of stocks over the last five years ended September 30th, 2019.

Value stocks - with large-, mid-, and small-sized - lagged significantly.

The difference in returns is unusually large, but growth stocks tend to outperform in periods of strong economic growth like we've experienced in this five-year period.

Click image to enlarge

Looking at the line chart shows the underlying volatility of the results better than the bar chart.

Click image to enlarge

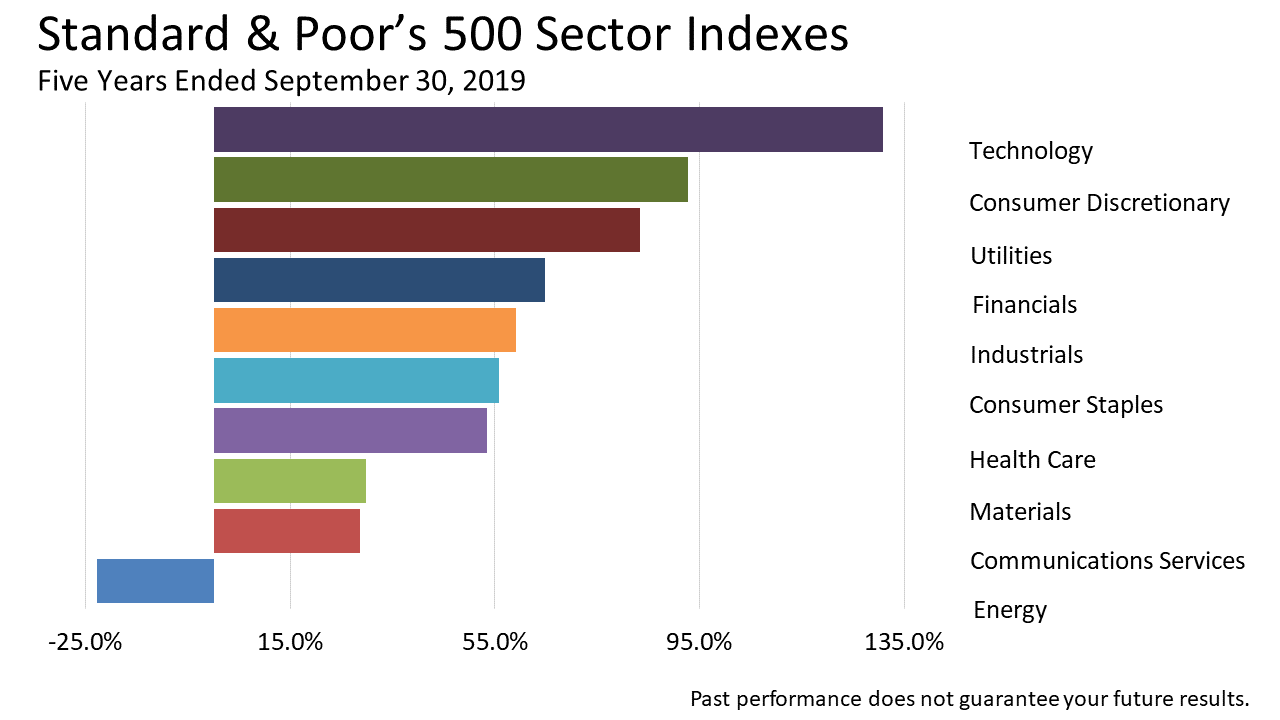

This five year snapshot of returns on different industry sectors of the S&P 500 stock index shows the tech sector - dominated by Apple, Amazon, Facebook, and Netflix - showed an astounding +131% return in the five years shown. These higher-risk growth companies paid off in a big way!

Of the 10 sectors, energy shares actually lost 23% of their value in these five years of bull market returns.

If you are employed in the tech sector, it's wise to examine your overall exposure personally to its risk. If you work in the tech sector, your job is obviously tied to the continued growth of the sector. Plus, you also may receive shares or incentives to buy your company stock as part of your compensation plan.

The growth in value of your tech investments could lead you to concentrate too much of your wealth in one sector.

It's just a risk that is often overlooked.

Longtime workers in the energy industry who concentrated their wealth on the oil economy for the past five years are undoubtedly regretting that they overlooked that risk.

Click image to enlarge

Click image to enlarge

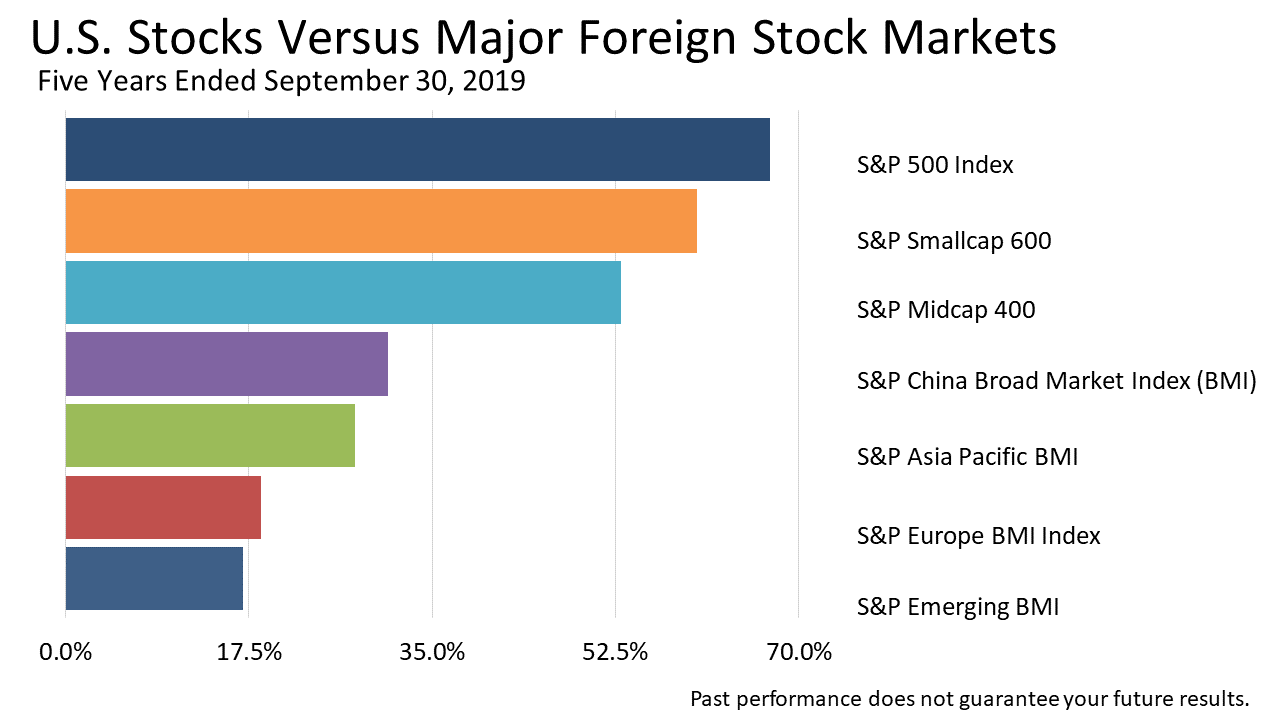

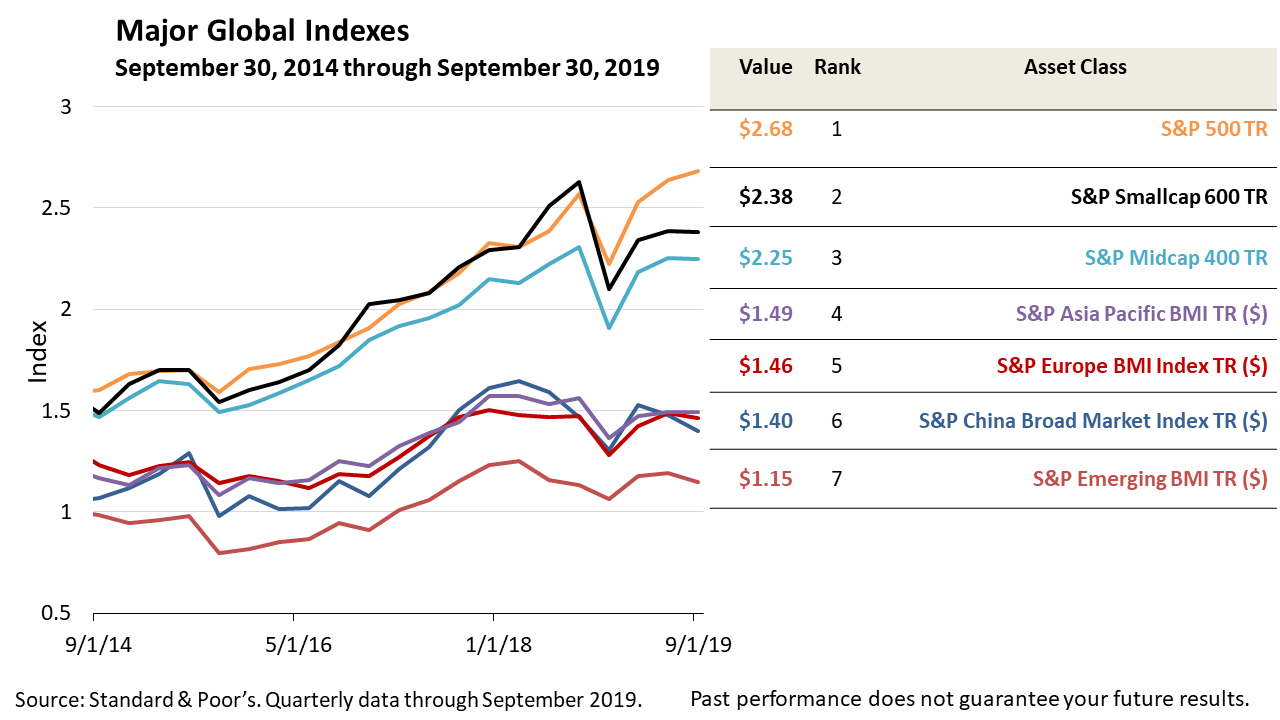

American blue-chip companies were the winners among major global share markets.

Since the financial crisis of 2008, the U.S. has led major world economies in its growth, and that's propelled large-cap S&P 500 companies as well as U.S. small- and mid-sized companies to outperform stock indexes of the other major economies of the world.

Europe over the past five years was stuck in slow-growth, a condition that may not change in the years ahead.

China's fledgling stock market showed the strongest returns of the foreign stock markets. However, Chinese control over the share market makes Chinese stocks subject to unusual financial as well as political risk.

Click image to enlarge

Click image to enlarge

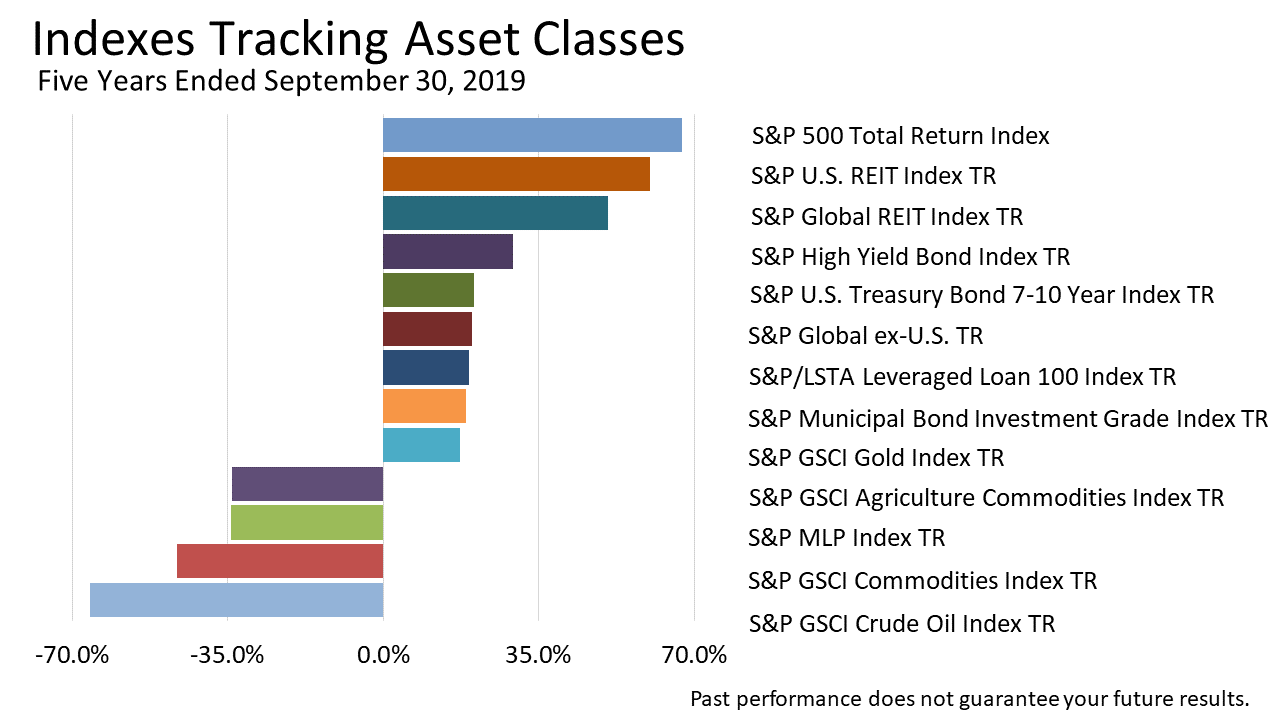

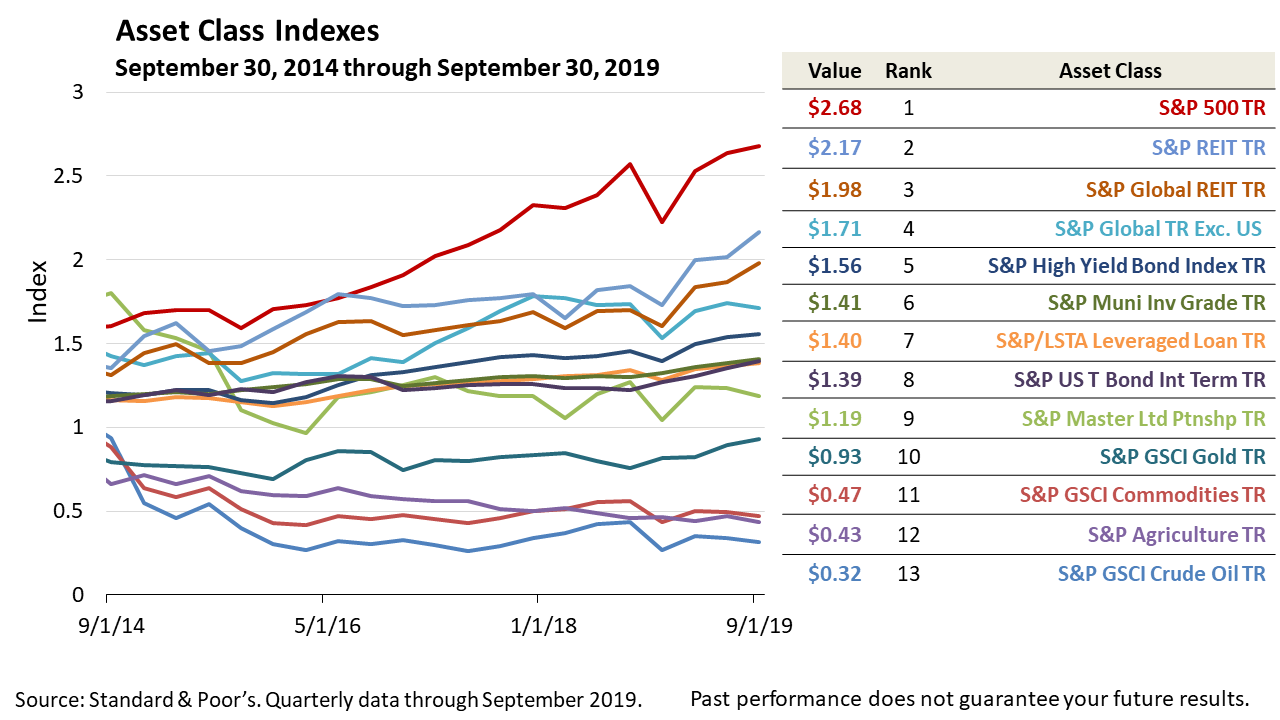

The 13 asset classes shown here ranked by returns make a case for diversification.

The risk of being overweighted in shares of commodities-related companies, that make the raw materials of tangible goods we buy and food we eat, were huge losers.

Shares in crude-oil-related companies in the five years ended September 30th, 2019 lost a stunning two-thirds of their value.

MLPs mostly own energy-related investments, which explains why they fell in value.

Click image to enlarge

Click image to enlarge