Should You Take Social Security Early Or Late?

Published Monday, February 20, 2012 at: 7:00 AM EST

Assuming the Social Security system continues to operate without a hitch, you can begin receiving your retirement benefits early, late, or right on time. The best option depends on your personal circumstances.

The age at which you’re eligible to receive full Social Security retirement benefits—often known as the normal retirement age, or NRA—is linked to your date of birth. The NRA ranges from age 65 for people born in 1937 or before to age 67 for those born in 1960 or after. However, everyone also has the option of receiving reduced benefits as early as age 62, or waiting longer to start—delaying benefits until as late as age 70—in return for larger monthly payments.

If you choose to start Social Security benefits earlier than at your NRA, the benefits are reduced by five-ninths of 1% for each month before that age, for up to 36 months. Begin taking benefits more than three years before your NRA and your benefits are further reduced by five-twelfths of 1% for each additional month.

Suppose your NRA is age 66 and you begin receiving benefits at age 62. Because you have 48 months until your NRA, benefits are reduced for each of the first 36 months by five-ninths of 1%—a total reduction of 20%. For each of the additional 12 months, benefits are cut by five-twelfths of 1%, or a total of 5%. Add the two together for a 25% reduction from what would have been your monthly Social Security benefit at your full retirement age. So you’re locking yourself into a lifetime of payments only three-quarters as large as you could have received if you’d waited four more years. Of course, you will also get four years’ worth of benefits that you would otherwise have missed.

Or you could decide to delay your Social Security benefits until after your NRA. Each year your wait increases your benefit by 8%. So, if your NRA is age 66, and you delay benefits until age 68, your payments will be 16% larger than if you’d begun taking payments at 66.

Or you could decide to delay your Social Security benefits until after your NRA. Each year your wait increases your benefit by 8%. So, if your NRA is age 66, and you delay benefits until age 68, your payments will be 16% larger than if you’d begun taking payments at 66.

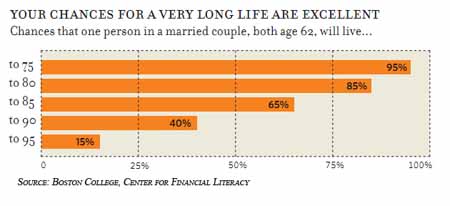

These calculations get even more complicated for married couples, who also have to weigh whose benefit, based on lifetime earnings, will be higher. For anyone, married or not, the ultimate payout you receive depends not only on when you start but also when you finish. If you start taking benefits early, your payments will be reduced, but if you die at a relatively young age, you may end up getting more back from Social Security than if you’d waited longer. In contrast, waiting as long as possible to start benefits may earn you the largest possible payout if you live a long time.

But there are also other factors to ponder. Consider these questions.

Do you need the money? If you have other income to sustain you in the meantime, it may pay to wait as long as possible to begin benefits.

What’s your break-even point? Eventually, waiting longer to receive higher benefits will result in a larger payout. But when you’ll break even depends on the amount of your benefit and is also affected by tax considerations and whether (and how) you invest the money you get from the government.

Are you still working? If you take benefits before your NRA, your payments will be further reduced by $1 for every $2 you earn that exceeds a specified annual maximum ($16,920 for 2017). In the year in which you reach your NRA, the reduction is $1 in benefits for every $3 in earnings above a higher limit ($44,880 for 2017). After that, you won't be penalized.

Are you still working? If you take benefits before your NRA, your payments will be further reduced by $1 for every $2 you earn that exceeds a specified annual maximum ($16,920 for 2017). In the year in which you reach your NRA, the reduction is $1 in benefits for every $3 in earnings above a higher limit ($44,880 for 2017). After that, you won't be penalized.

Are you covered by Medicare? Starting at age 65, Medicare will be your primary health insurance. But you’ll pay a monthly premium for that coverage that will be deducted from your Social Security benefits. You can also opt for Medicare Part D coverage for prescription drugs; there’s an additional cost for Part D that will further reduce the size of your Social Security check.

Is your decision irrevocable? If you started benefits early, you can opt to pay back what you’ve received from the government and then select a later start date. But this option is limited to one year’s worth of benefits. Whether that makes sense depends on your age, life expectancy, and tax status—and, of course, you’ll have to come up with the cash to make the repayment.

With all of Social Security’s complex rules and so many financial factors affecting individual outcomes, it’s never easy to decide what to do. We can work with you to consider what may work best in your situation.

© 2024 Advisor Products Inc. All Rights Reserved.