Financial Briefs

Email This Article To A Friend

Can You Avoid Estate And Gift Tax?

Are you hoping to pass investment assets to your heirs without any tax damage? Under the current rules, you have plenty of leeway to avoid estate and gift taxes on the federal level, although state taxes may be another story. However, keep in mind that your investment returns may outpace the inflation adjustments to the personal gift and estate tax exemption - and this could mean that your wealth will grow enough to be subject to taxes when you die.

There are two main estate and gift tax breaks: the annual gift tax exclusion and the unified estate and gift tax credit.

1. Annual gift tax exclusion. You can give each recipient, such as a younger family member, assets valued up to $14,000 a year without paying any gift tax (or even having to file a gift tax return). The exclusion is doubled to $28,000 for joint gifts made by a married couple. So, if you and your spouse each give the maximum $14,000 to five other family members, you can reduce your taxable estate by $140,000. And you can do this year after year.

The annual gift tax exclusion is indexed for inflation but rises only when the cost of living increases enough to result in a $1,000 bump to the exempt amount. With inflation very low in recent years, increases have slowed to a crawl. The last adjustment was made in 2013, from $13,000 to the current $14,000.

2. Unified estate and gift tax credit. This generous credit can wipe out either estate taxes, gift taxes, or a combination of the two.

After a decade of gradual increases, Congress permanently locked in the exemption amount at an inflation-adjusted $5 million. For 2017, the exemption is $5.49 million. That means a couple easily can shelter more than $10 million in assets from estate tax, although any lifetime gifts exceeding the annual gift tax exclusion will reduce the amount available to help an estate avoid estate taxes.

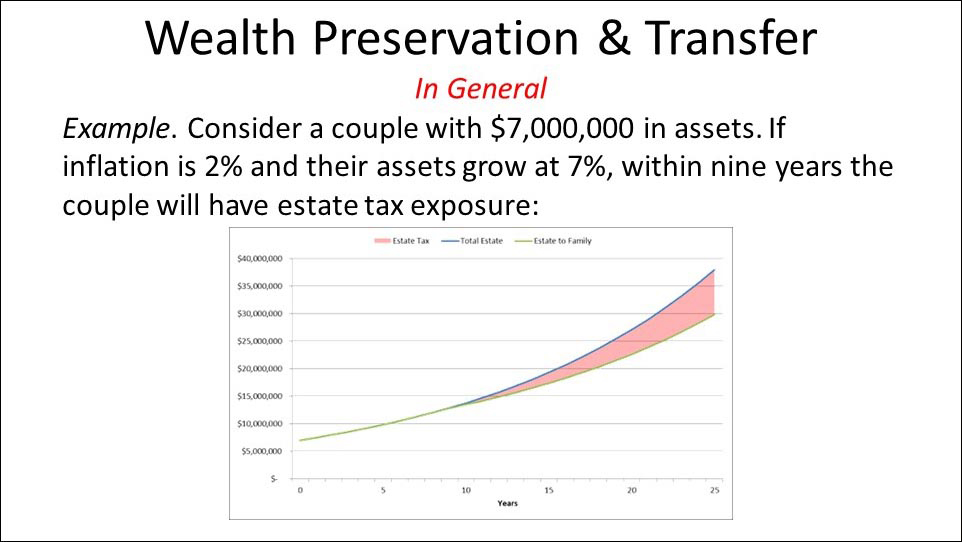

But you can't simply take this tax shelter for granted. Remember that your assets may appreciate in value at a rate greater than the annual inflation adjustments for the estate tax exemption. (Of course, assets also might decline in value.) This is especially true if the recent trend in low inflation persists. For example, suppose a couple has $7 million in assets and earns an annual average return of 7%. If the inflation rate remains at 2%, it will only take nine years for the couple to face federal estate tax exposure.