Market Data Bank

Click image to enlarge

Stocks posted a surprising +13.7% gain in the first quarter of 2019 after a fourth quarter 2018 loss of -13.5%.

Click image to enlarge

As the quarter ended, investor psychology showed signs of a change, and stock market indexes hovered near all time highs.

Click image to enlarge

Barron's ran a cover story saying the 10-year old bull market could go on for years and optimistic headlines appeared all over the media.

Click image to enlarge

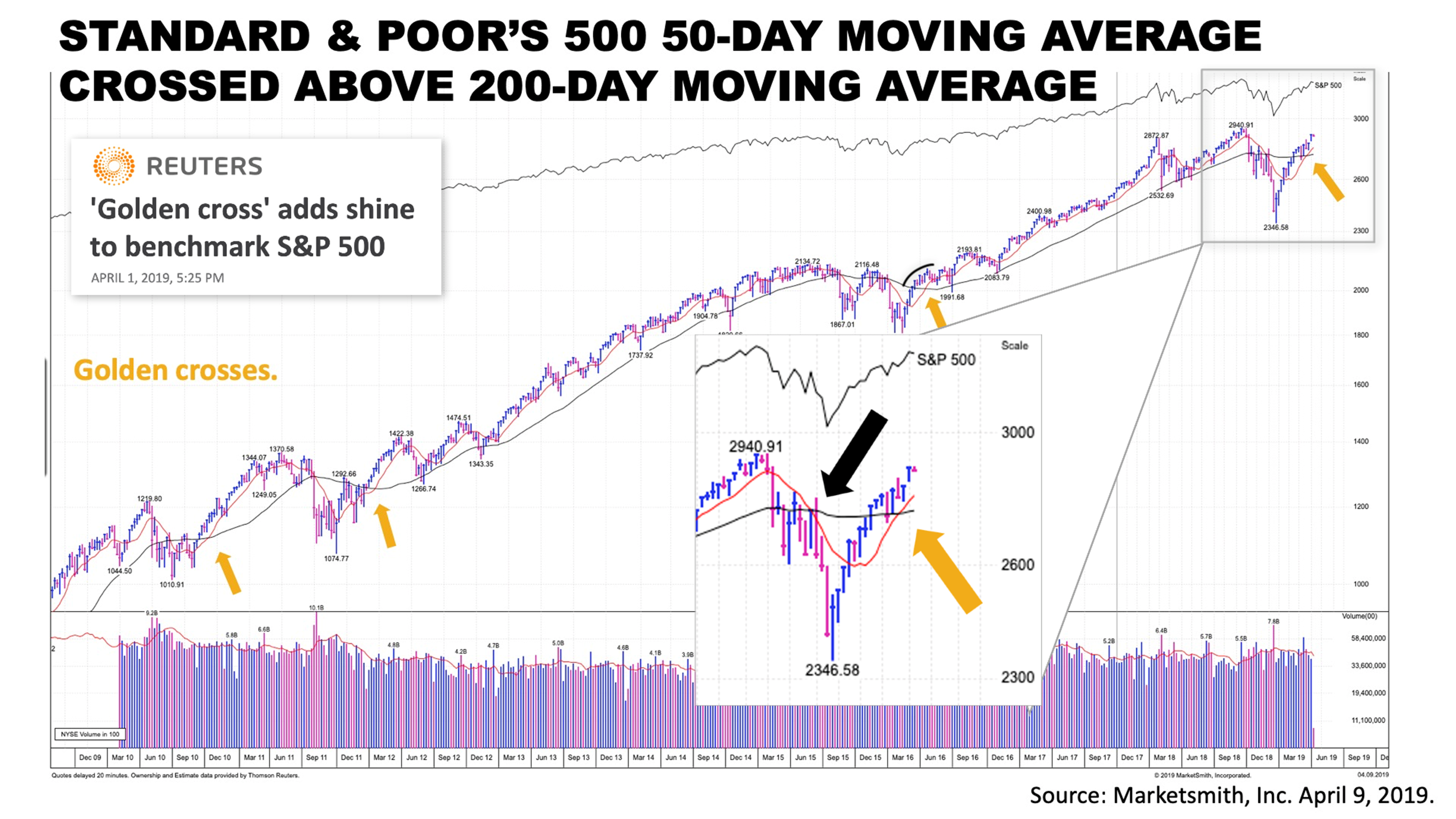

Adding pizzazz to the bullish banter, a "golden cross" was formed on April 1st, when the S&P 500's 50-day moving average crossed above its 200-day moving average.

Golden crosses occur infrequently. The last one was in April 2016 and a strong bull run followed suit.

Golden crosses and dreaded death crosses, which are believed to form at the end of bull markets, have been a fairly reliable market forecasting signal.

Click image to enlarge

Golden crosses and bullish that go on for years are all well and good, but ultimately, the economy drives stock market prices, and the underlying economic fundamentals are indeed signaling strength ahead.

Click image to enlarge

The National Federation of Independent Business latest monthly survey of small-business owners, who create 75% of all new jobs, were less optimistic compared to a year ago, but 2018 was the all-time peak and business owner optimism remained strong by long term historical standards.

Click image to enlarge

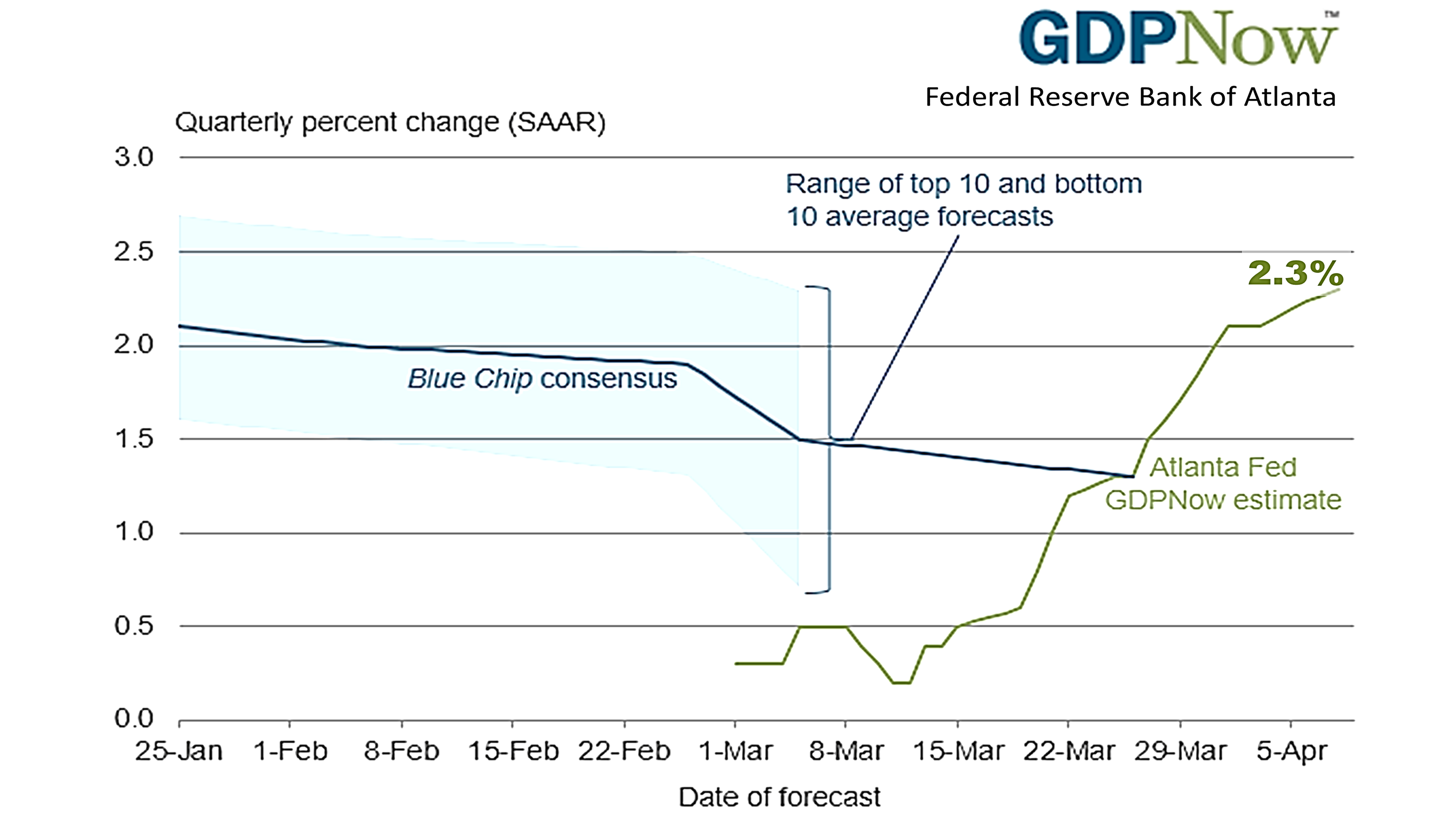

The 60 economists surveyed monthly by The Wall Street Journal in early April boosted their forecast from a month earlier for first-quarter growth from 1.3% to 1.5%.

Click image to enlarge

A similar survey by Blue Chip Econometrics also forecast 1.3% first-quarter growth, but a good economic surprise may be under way.

Click image to enlarge

The Atlanta Fed's GDPNow forecast, which grows more accurate in the days after the end of a quarter but before the Commerce Department announces the official figure, was forecasting a first-quarter growth rate of 2.3%. It meant the forecast from the consensus of economists could be wrong and surprising strength was possible.

Click image to enlarge

As the quarter ended, job openings remained near a record high and March jobs openings remained near unprecedented highs while the unemployment rate stayed at a low not seen in many decades.

Click image to enlarge

An abundance of new jobs during a period of low unemployment creates upward pressure on wages, which fuels consumer spending, and consumer spending drives growth.

Click image to enlarge

The economy is strong - not roaring but growing at a sustainable rate.

Reviewing performance of the stock market, as we are about to do, requires a reminder to stay focused on fundamentals and not get caught up in the swings in sentiment from fear to greed.

That's as important in times of bullish sentiment like we've seen in the first quarter as in bear market plunges.

Click image to enlarge

We view investing through a lens prescribed by an academic body of knowledge called Modern Portfolio Theory.

MPT means a lot of things to different people and it's not a guarantee of success. Academics can be wrong and there's plenty of room for disagreement over details of how to apply MPT to get the best results. However, we believe a quantitative, statistically-driven approach based on economic fundamentals and a respect for history, along with prudent judgment about current and expected conditions is sensible.

Looking at this bar chart, we see three month results. Three-month results are not really important. It's a short time in the life of a portfolio you probably are planning to hold for the rest of your life. To be blunt, even in your 90s, you probably don't plan on dying within the next 10 years or maybe even 15 years, and that means you're a long-term investor.

Logically, a prudent investor doesn't make judgments about a long-term portfolio based on just a single quarter's results. However, we like to keep an eye on the short-term results as a professional who wants to understand the development of long-term trends.

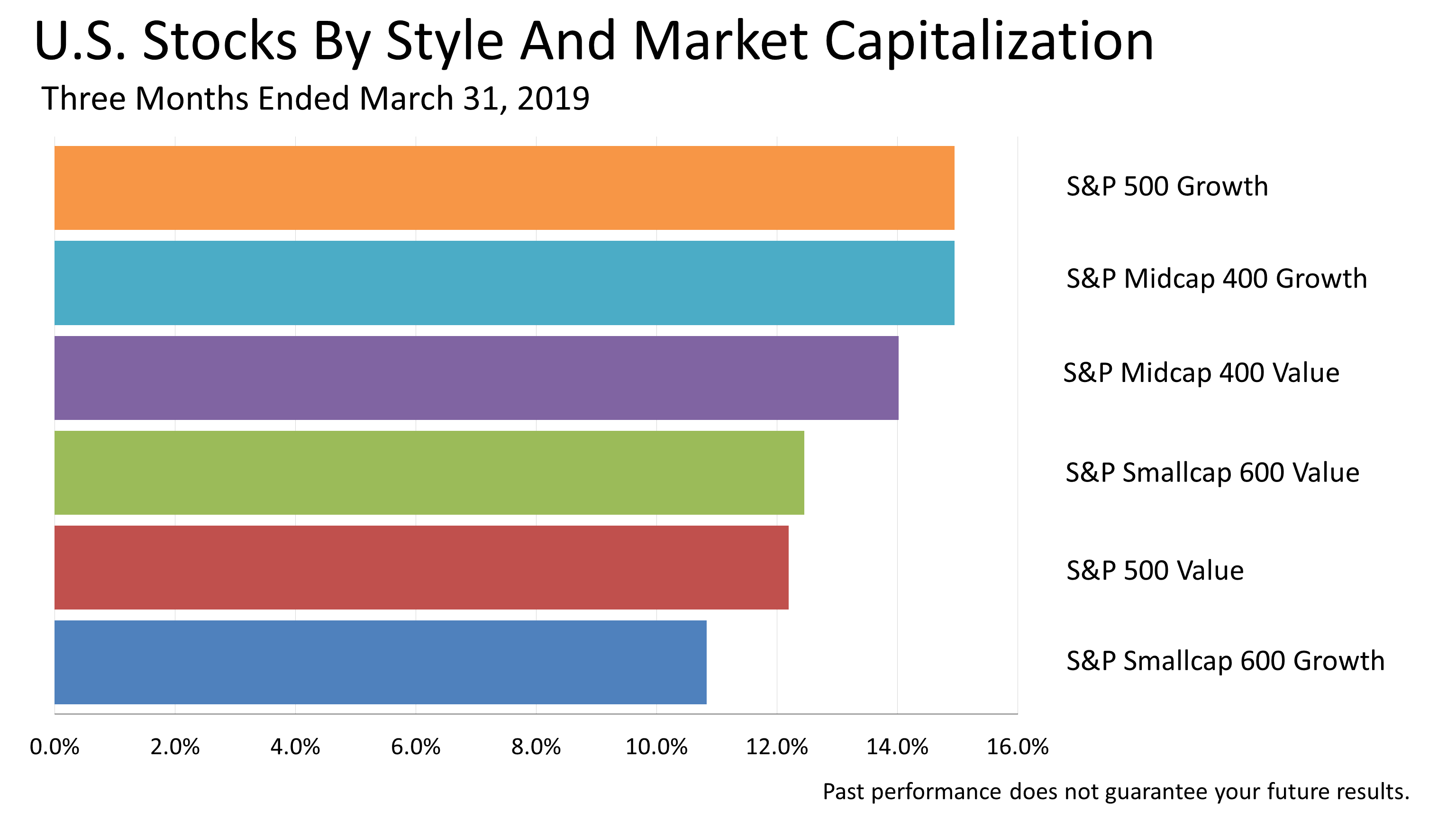

More important than the three months results is the divvying up of the Standard & Poor's 500 - an index of America's largest publicly-held companies - by public market value and a statistically-driven growth profile categorizing companies based on earnings as good values or growth investments.

This chart shows that, in the first quarter, investors were rewarded for owning companies characterized as growth investments with a 15% total return. With The S&P 500 since 1926 averaging just less than 10% - over 93 years through 2018 - the 15% return in three months was totally unexpected following the disastrous fourth quarter when stocks plunged -13.5%.

That growth companies showed the best return is to be expected in an economic expansion. Risk assets like the S&P 500 often are strong performers in good times. Thus, the riskier portion of the stock market, growth stocks, outperformed in the quarter. But value companies were a close second.

Click image to enlarge

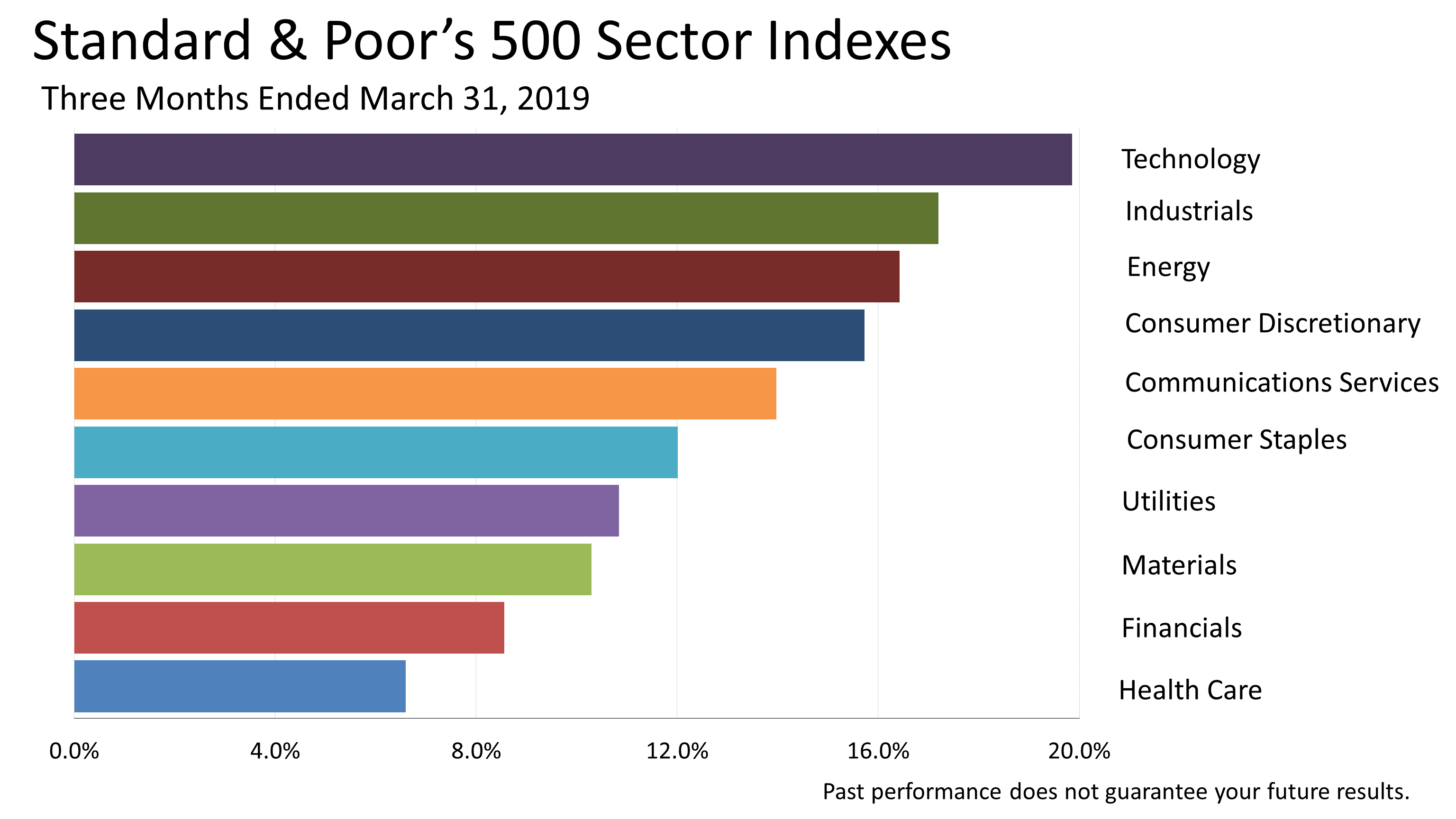

With the economy growing and the long bull market back on track after the fourth quarter fall, tech stocks led.

Click image to enlarge

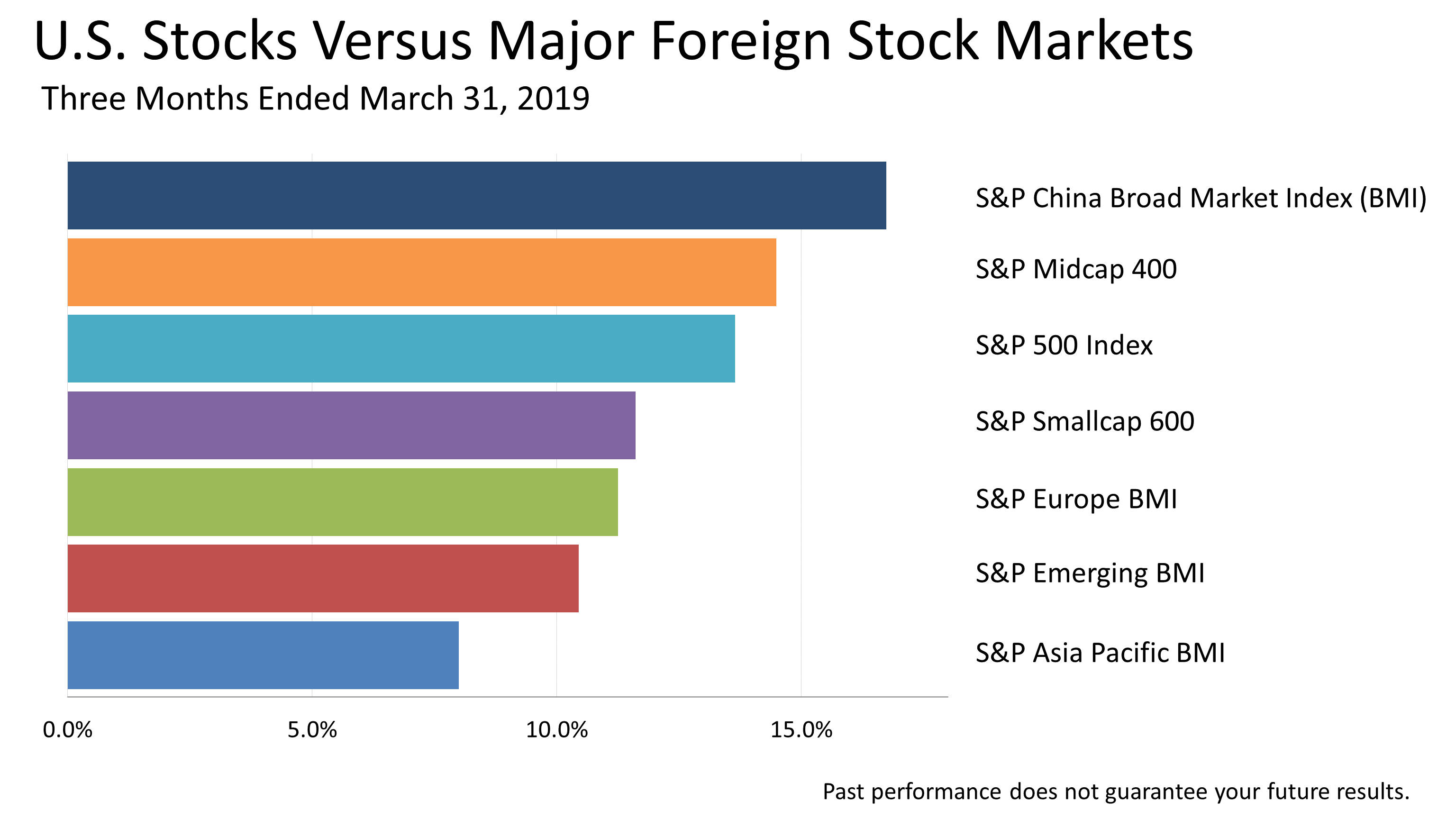

The fledgling Chinese stock market returned more than U.S. shares in the three months, as fears of a U.S. China trade war subsided.

More importantly, fears of a global recession also subsided.

Click image to enlarge

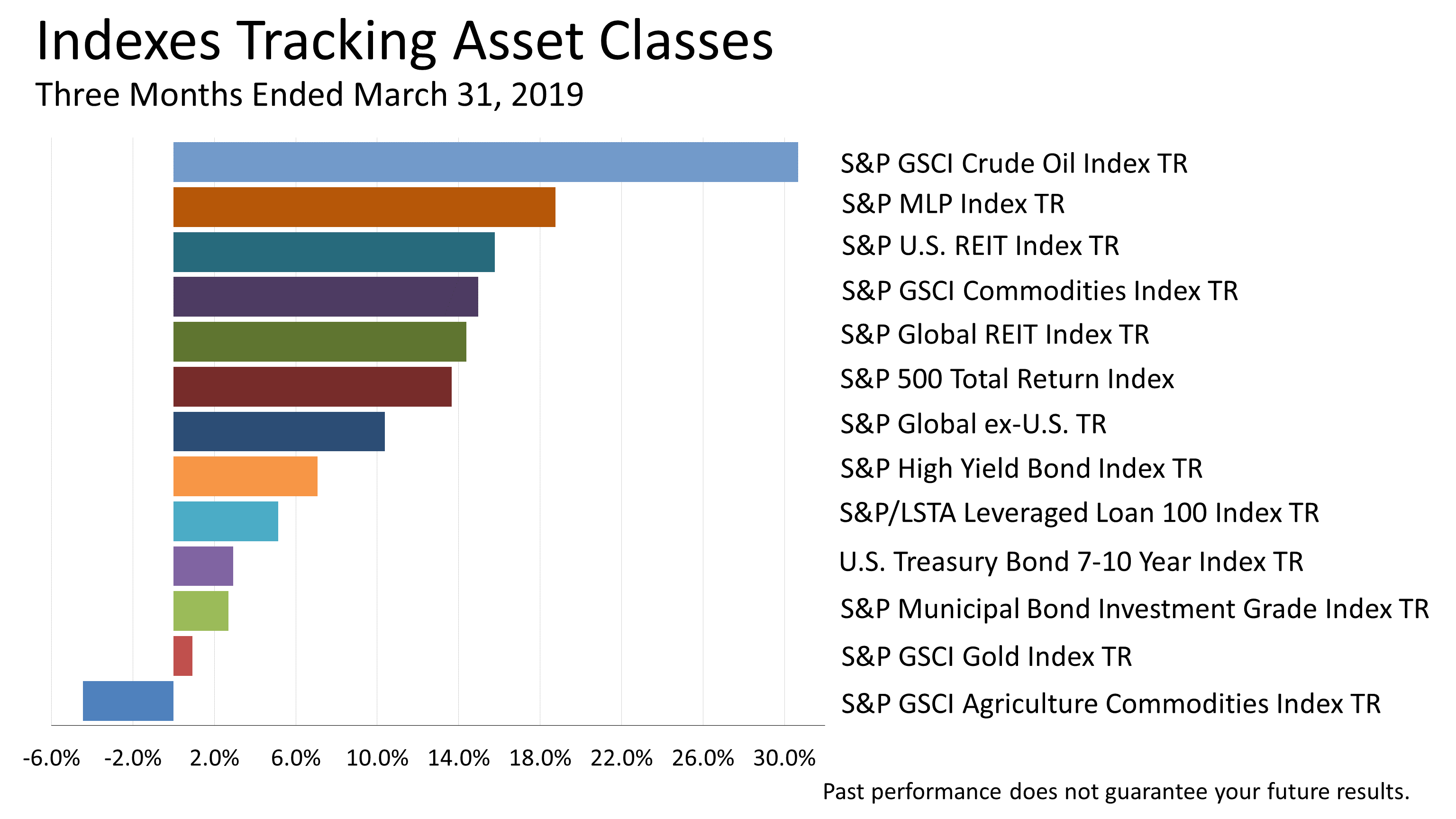

In a sign of good times for investors, just one of the 13 indexes tracking a broad array of assets classes - representing an array of different investments - showed a loss.

Companies investing in agricultural commodities lost 4.5% of their value in the quarter, based on the Goldman Sachs index, but companies in the Goldman Sachs crude oil index returned 30.7%. The variation of returns between two commodities highlights the unpredictability of investing, supporting a broadly diversified framework for a long-term investor.

Click image to enlarge

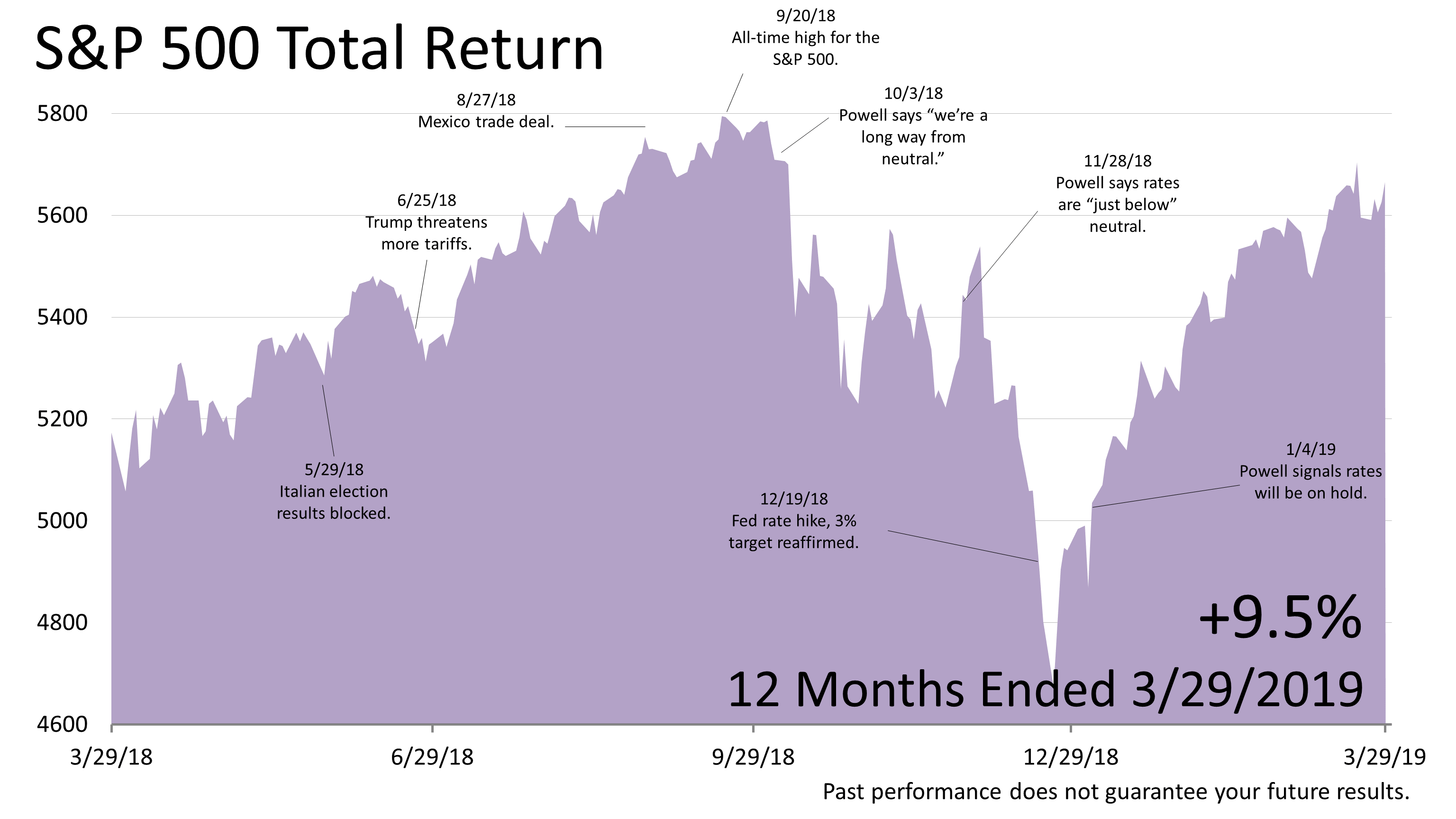

The S&P 500 hit a record all-time high on September 20, 2018, then dropped to a Christmas Eve low, down -19.8%.

Rounding makes it qualify as a bear market drop of 20%.

But it was a short bear run.

The stock plunge occurred in response to the Fed's December 19, 2018 decision to raise lending rates a quarter of 1%, sticking to its plan to raise the fed funds target rate to 3% in 2019.

Investors sold stocks in alarm on the Fed's decision because hiking 90-day Treasury Bill rates to 3% seemed likely to send short-term lending rates higher than the rate on 10-year Treasury Bonds, resulting in an inverted yield curve, which presaged every recession in the post-WWII era.

On January 4th, the Fed reversed course. It would no longer pursue its previously announced 3% target rate and hold off on further rate hikes until conditions were more favorable. Since then, the stock market has almost fully recovered to its September 20th all time peak.

Click image to enlarge

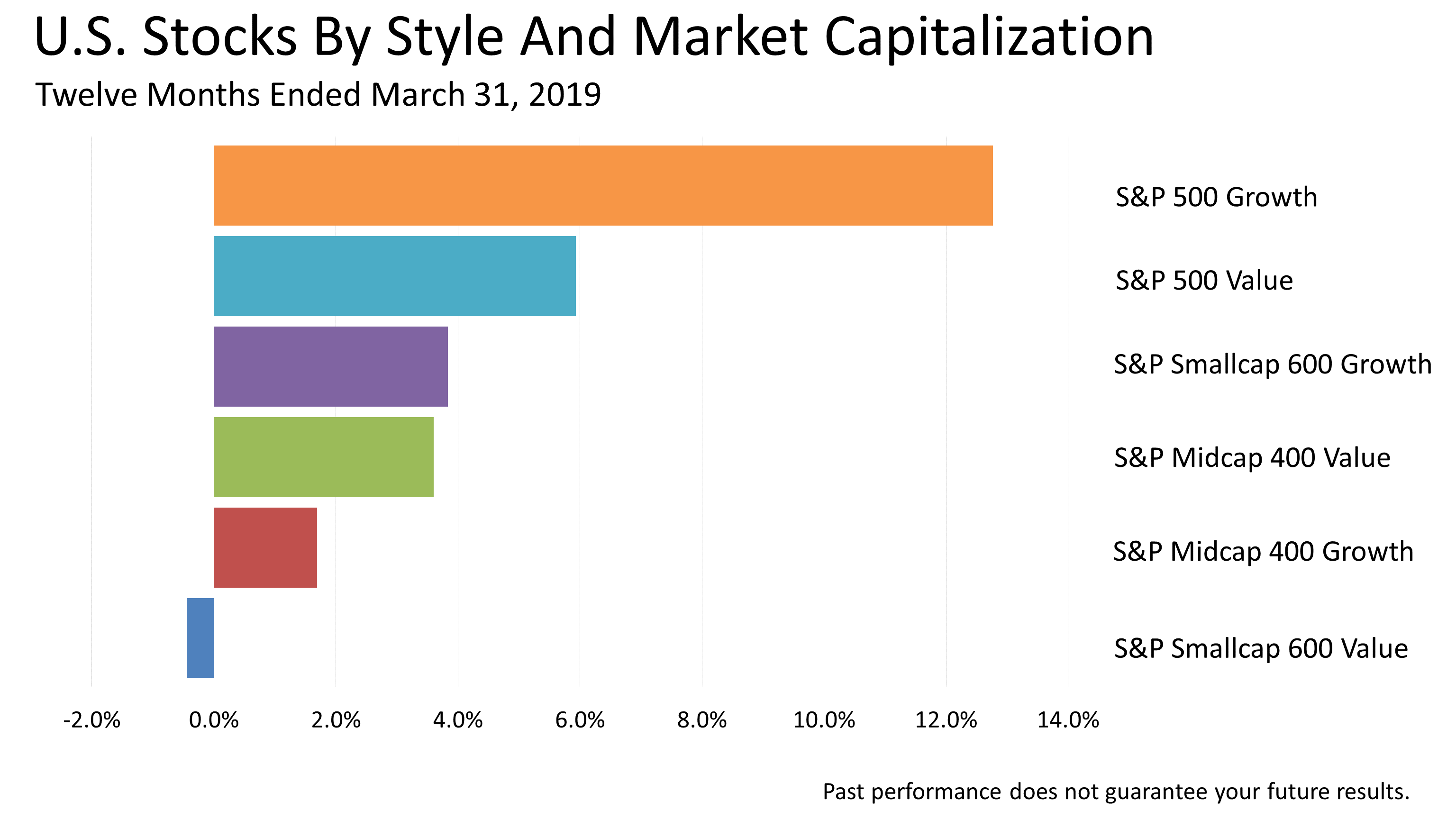

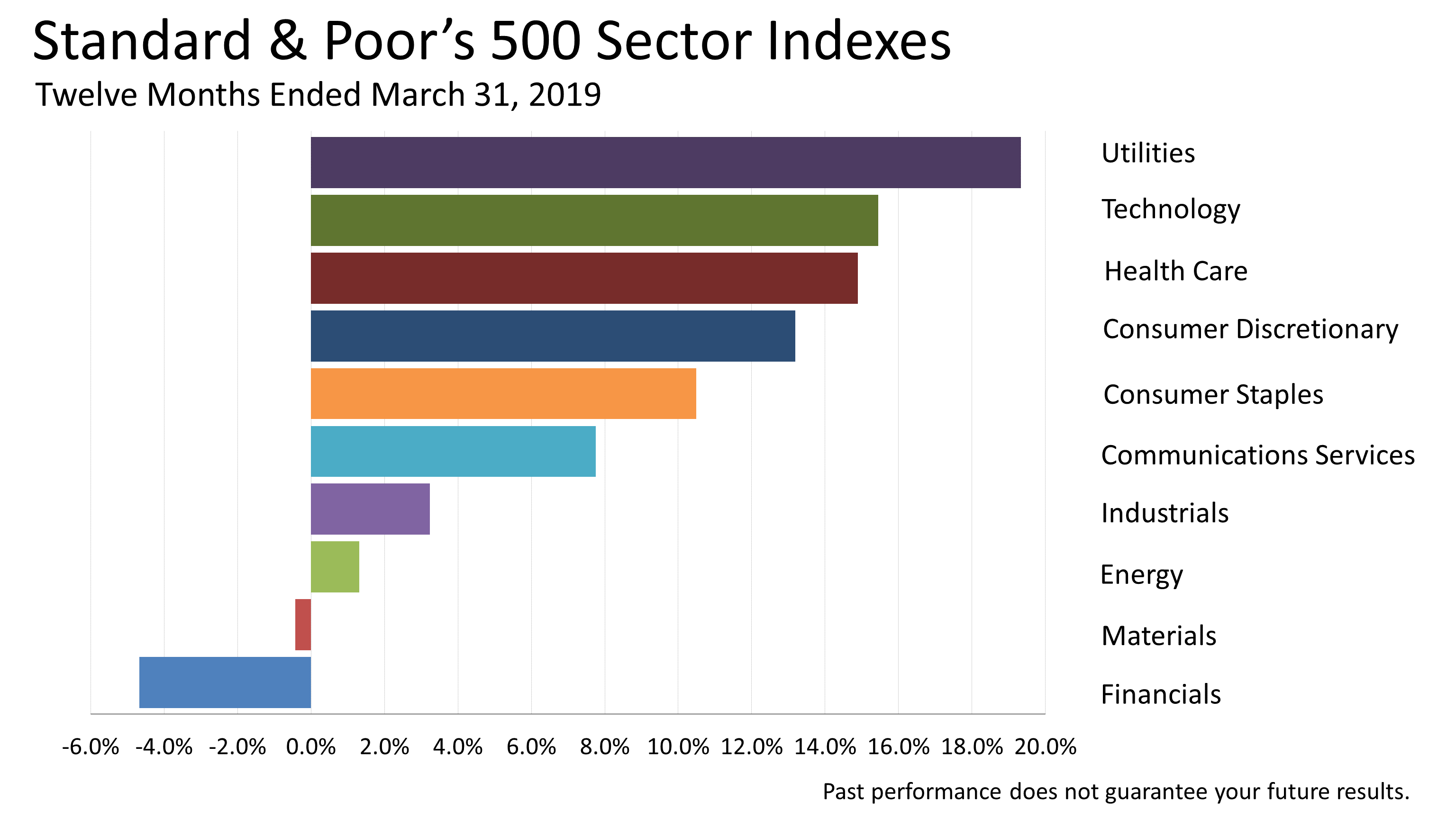

In the 12 months ended March 31st, 2019, growth stocks in the S&P 500 outperformed value by a 12.8% versus 5.9% margin.

Click image to enlarge

The yield of the 10-year U.S. Treasury bond dropped sharply, from 2.69% to 2.41%, during the quarter, which fueled a surge in Utilities. Utilities' yields track bond yields and made utilities stocks more attractive as an income vehicle to investors. The drop in interest rates caused the yield curve - the difference between 10 year T-bonds and 90-day T-Bills - to invert at the end of the year. That was perceived as very bad news for banks' earnings, causing a loss in bank sector stocks.

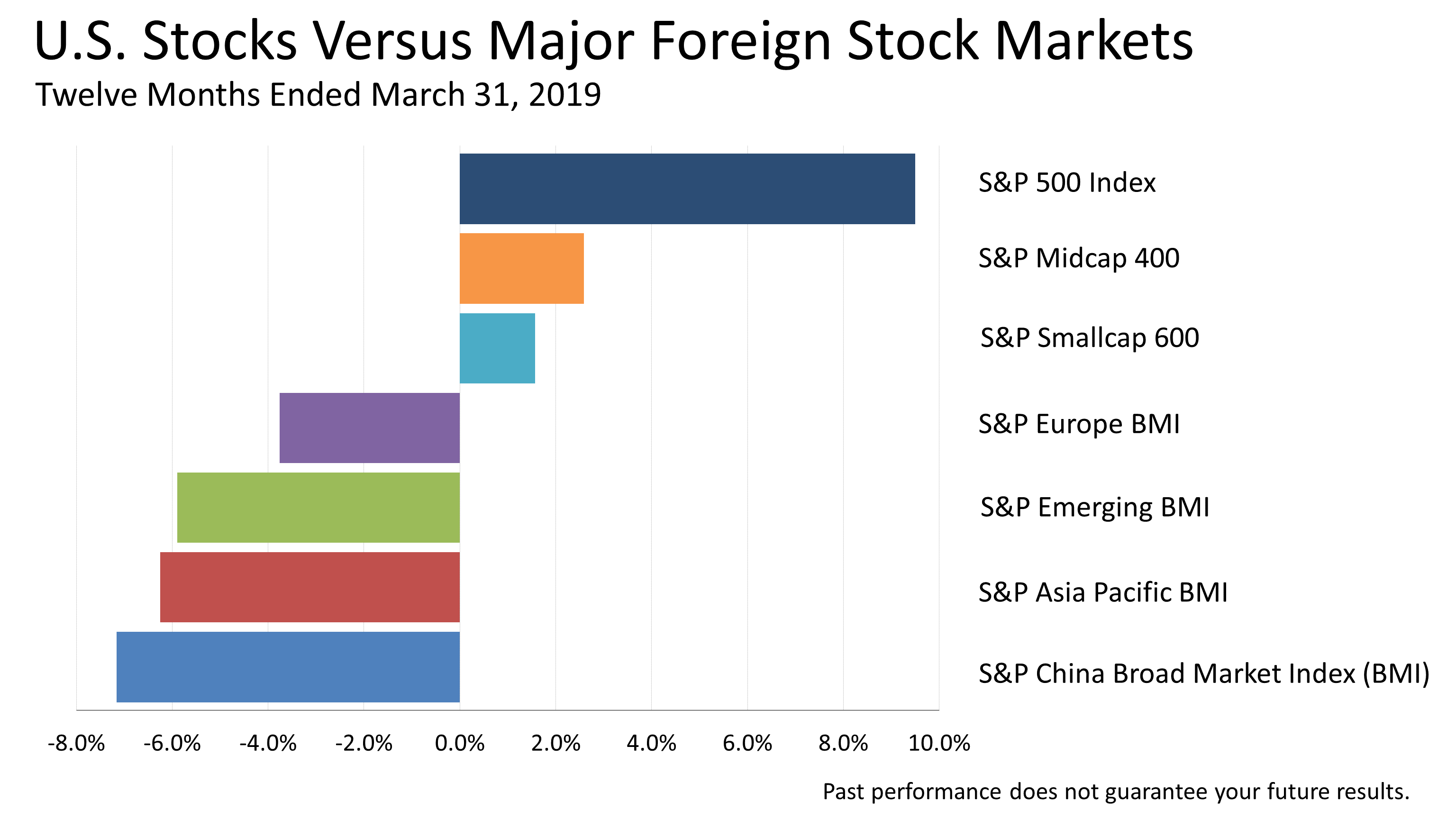

Over the one-year period ended March 31st, 2019, China was the laggard, as prospects of a trade war with the U.S. mounted.

While China's economy would shrink materially if exports to the U.S. were stopped, U.S. GDP was expected to suffer only fractionally from a China trade war. U.S. stocks in the 12 months showed a 9.5% total return.

European, emerging markets, and a stock index representing Asian stock prices showed losses, respectively, of 3.8%, 5.9% and 6.2%.

Click image to enlarge

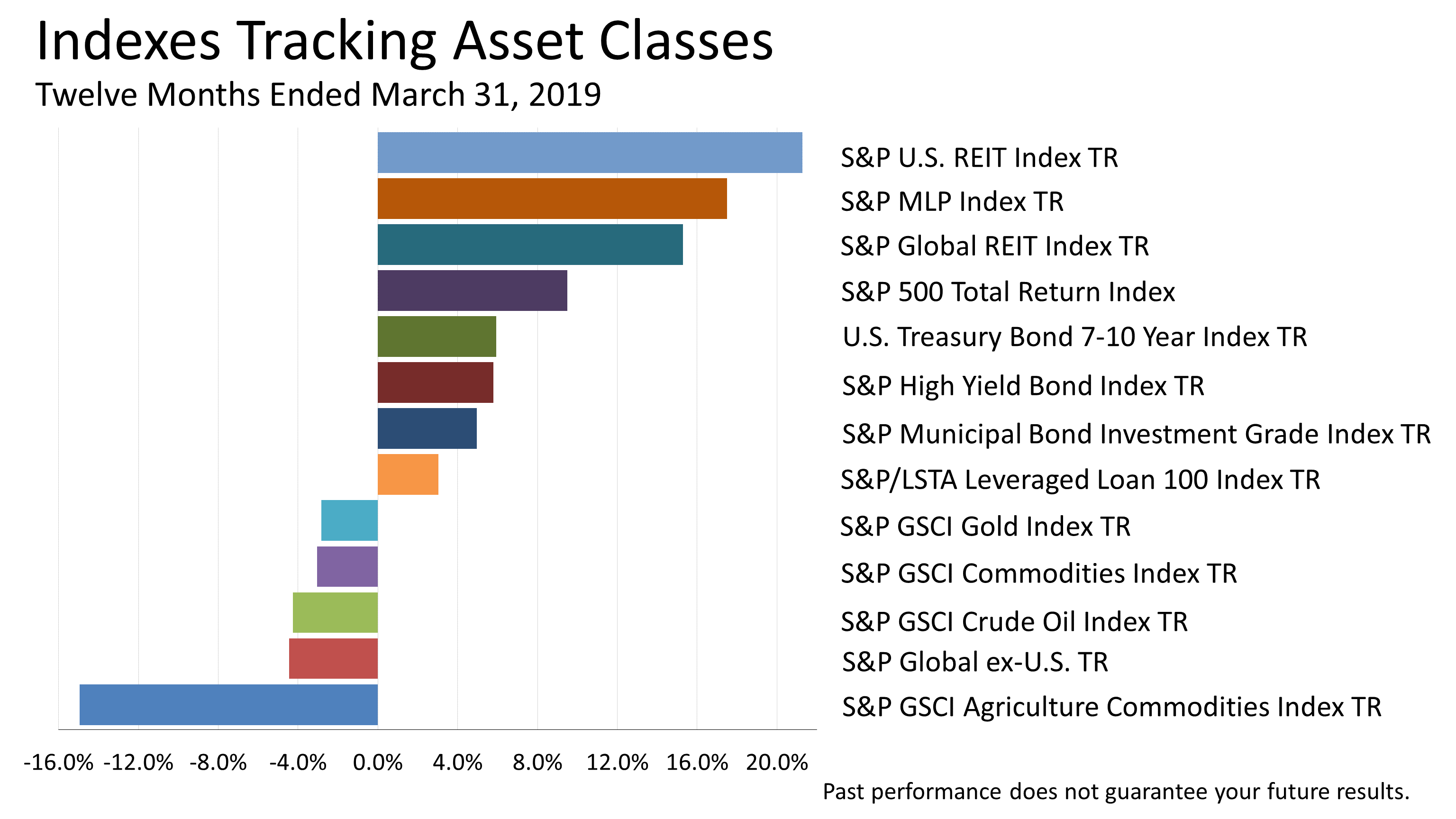

Here's a snapshot of how 13 indexes representing an array of indexes with distinct and different statistical characteristics historically performed in the one-year period ended March 31, 2019. Commodities were clobbered, including oil and gold as well as agricultural.

Also noteworthy is the 4.4% loss in stocks worldwide excluding the US, which highlights the exceptional performance of the U.S. compared to other stock markets across the world.

Click image to enlarge

After trading sideways in 2015 and most of 2016 - plunging twice along the way - the stock market broke out after the November 2016 election and rose steadily to an all-time peak on September 20, 2018, and then dropped -20% in value on fears an inverted yield curve was imminent and presaged recession, which is defined as two consecutive quarters of GDP contraction. That's two quarters of a shrinking economy; it's like going backwards.

Alas, unfolding economic reality was more nuanced than the neat definitions of the historical narrative.

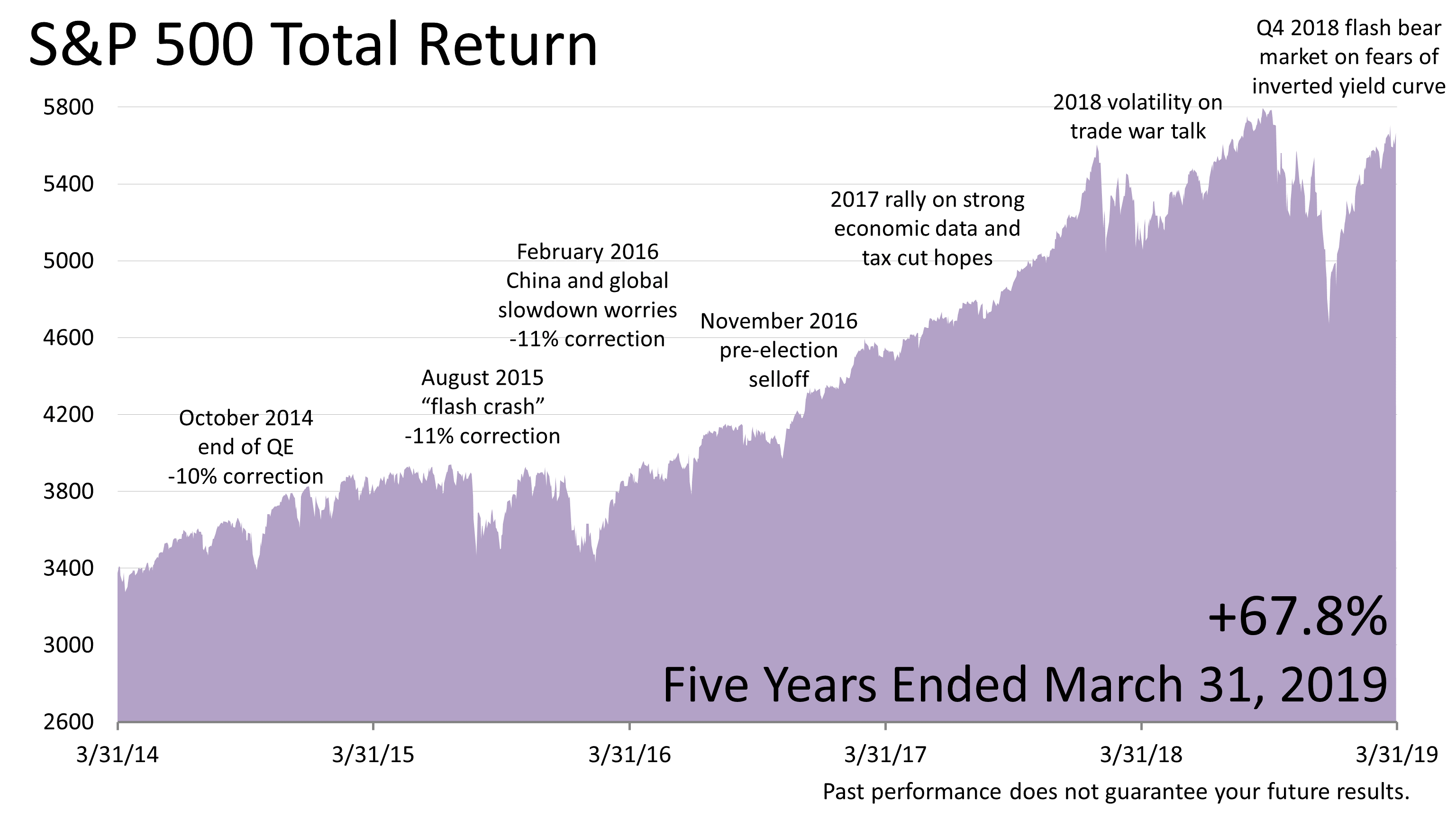

Over the last five years, including dividends, the S&P 500 total return index has gained +68%, as illustrated in this chart, compared with a gain of +51% for the commonly quoted S&P 500 price index, with the 17% difference being dividends reinvested.

The five-year gain of +68%, or +13.6% per year, is substantially greater than the stock market's long-term annual total returns of approximately +10% going back 200 years as described by Wharton professor Jeremy Siegel in his seminal book, Stocks for the Long Run, first published in 1994.

Click image to enlarge

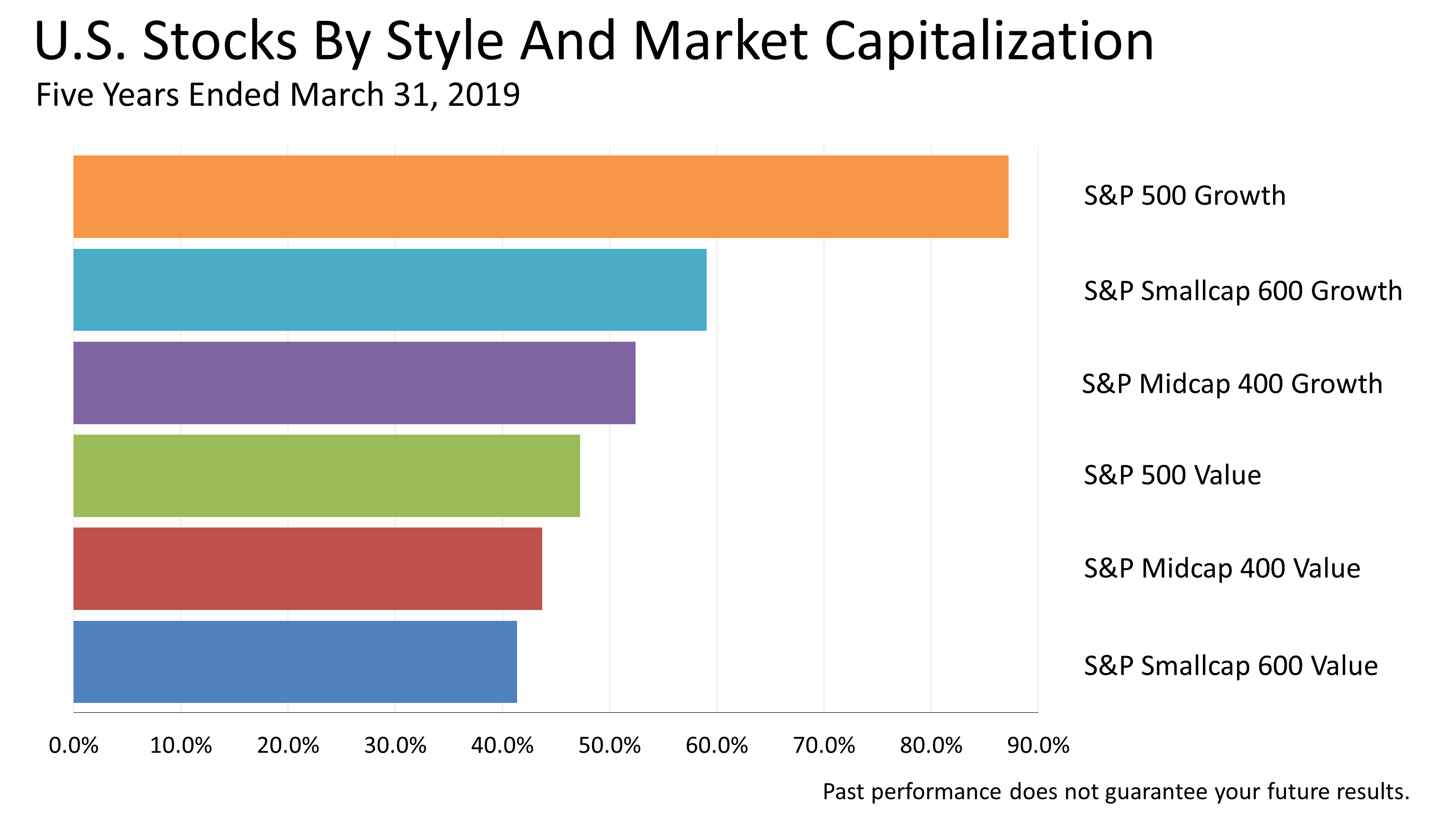

For the five years that ended March 31st, 2019 growth stocks outperformed value stocks in all three market-cap categories.

The big difference in growth versus value-priced companies in the S&P 500 is how you'd be invested without a discipline of rebalancing.

Ove the five years shown, growth stocks would have appreciated by 87.2% versus 41.4% for small company value shares. S&P 500 growth companies would have outgrown the five types of U.S. stocks in these five years left unmanaged. This is why rebalancing annually is important in avoiding growing overly weighted in one style of stocks or one asset class.

Click image to enlarge

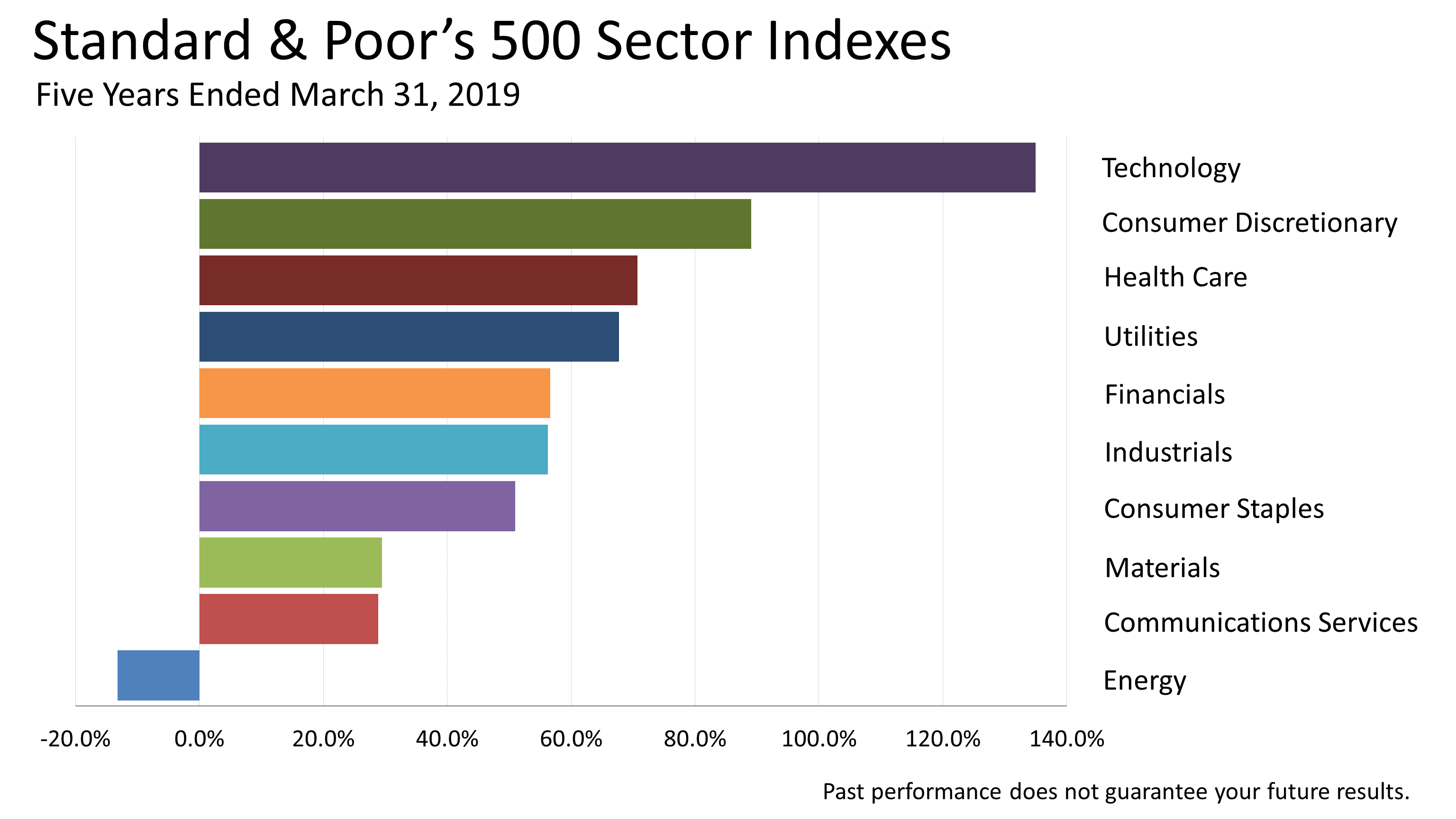

Strong earnings were favored by stock investors in the five years through March 31, 2019. The lagging sectors - energy, communications services, materials, industrials and consumer staples - consisted mainly of "value" stocks in industry sectors with slower earnings growth. The penchant for strong earnings growth drove huge gains in the FAANG stocks - Facebook, Apple, Amazon, Netflix and Google, plus Microsoft, propelling the surge in tech.

Prices of shares in the energy and material sectors were slammed by the collapse in crude oil and most other commodity prices. The price of crude oil, while up dramatically from its bottom in early 2016 of $26 per barrel, remained far below its peak 2014 price of $114 per barrel. The energy sector of the stock market is highly correlated with crude oil prices.

Click image to enlarge

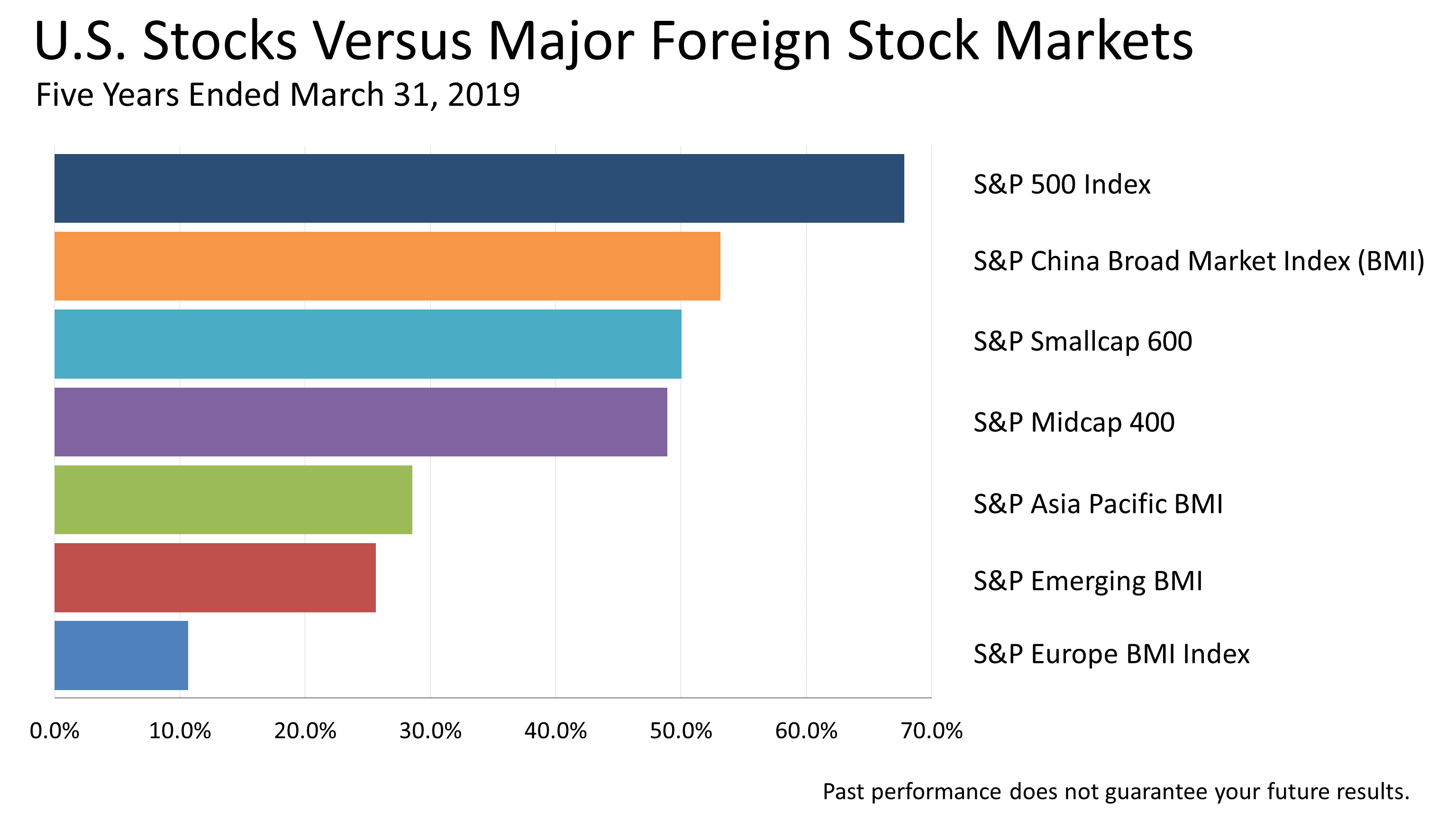

In the five years through March 31st, 2019, U.S. large cap stocks returned a very strong 67.8%. The U.S. stock market's performance led the world, as it has done consistently since the U.S. began emerging from the global financial crisis a decade ago.

China's stock market offers a fraction of the liquidity of the U.S. and the price of Chinese company shares are subject to less transparent and well-defined accounting standards as well as government influence or control, gained 53.1%. Developed-country stock markets in the Asian Pacific region of the world, which includes Japan, Australia, Korea and Hong Kong, returned 28.5% over the five years, and European stocks returned 10.7%.

U.S. stocks, the growth engine of a diversified retirement portfolio for Americans, delivered exceptional returns relative to the rest of the world.

Click image to enlarge

U.S. stocks also came out on top of this list of 13 securities investments representing different asset classes.

The S&P 500 index's total return of +68% over the past five years is almost four times the S&P Global ex-U.S. stock market's return of +18%. It is testament to how resiliently the U.S. economy came out of the last, severe global recession, compared to rest-of-world economies.

In last place, of course, is crude oil, its price having been broken by the surge in U.S. supply fueled by the shale-fracking revolution. Commodities and gold, too, have been money-losers over the past five years with very benign inflation, a strong dollar, and an ample supply of most commodities.

Click image to enlarge