Market Data Bank

Click image to enlarge

The second quarter of 2019 ended with the Standard & Poor's 500 repeatedly breaking new all-time highs amid signs of slowing economic growth.

Before beginning any discussion of portfolio performance, I just want to remind everyone of some prudent context.

Click image to enlarge

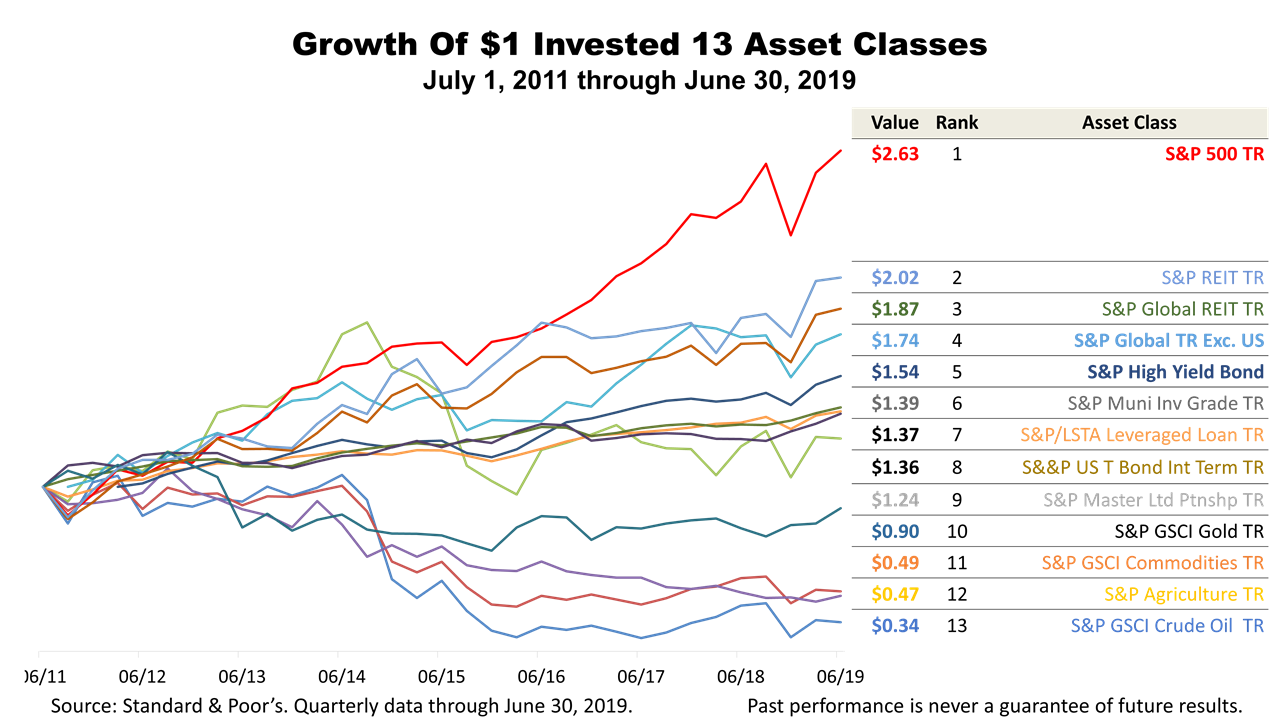

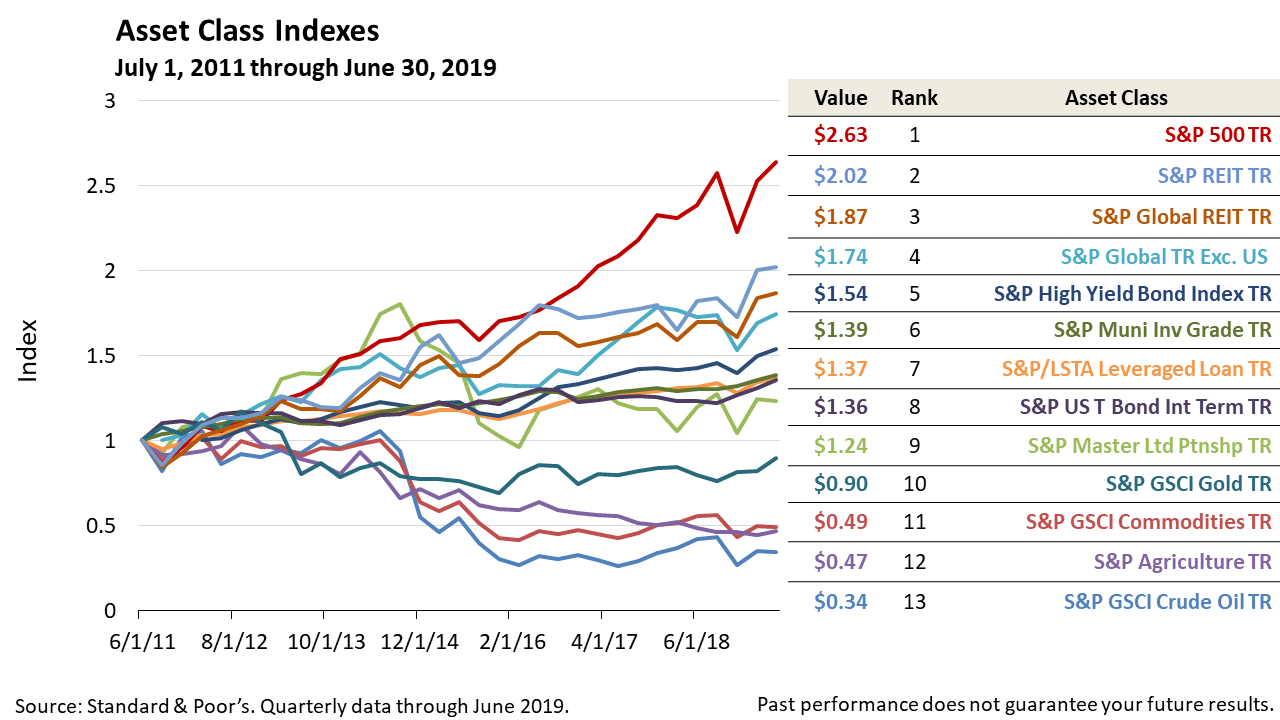

With the expansion on July 1st entering its eleventh year, what stands out most in this chart showing the performance of 13 assets since July 2011, is the towering performance of U.S stocks.

A $1 investment in global stocks excluding US stocks, grew to $1.74 versus the $2.63 return on America's blue-chips!

The U.S. has led the world's economic comeback since the global financial crisis in 2008!

Point is, investors in U.S. stocks in the period right after the financial crisis had no idea The Great Expansion and historic bull market was about to begin. They took a risk amid great uncertainty.

Today, in the midst of the longest economic expansion in modern U.S. history, with signs of slower growth appearing in recent data, uncertainty still prevails. No one knows if the bull market and expansion will continue. We do know that economic fundamentals indicate a recession is not on the horizon.

Click image to enlarge

Uncertainty about the future is a permanent condition. Successful long term investing means not just accepting perpetual uncertainty, but welcoming it. Wise investors are thankful for the uncertainty!

Click image to enlarge

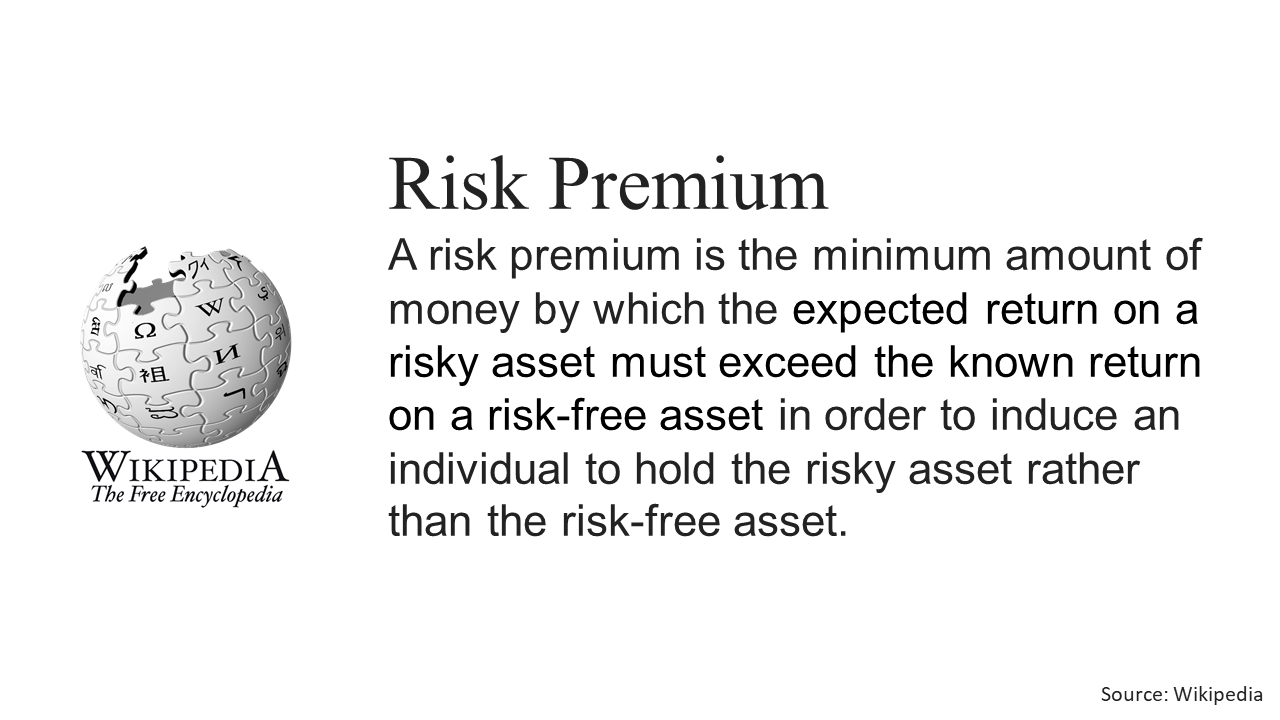

A rubric of modern portfolio theory taught at colleges and universities holds that investors get paid extra return for taking risk.

The risk premium is the amount you get paid for owning a risky asset.

Click image to enlarge

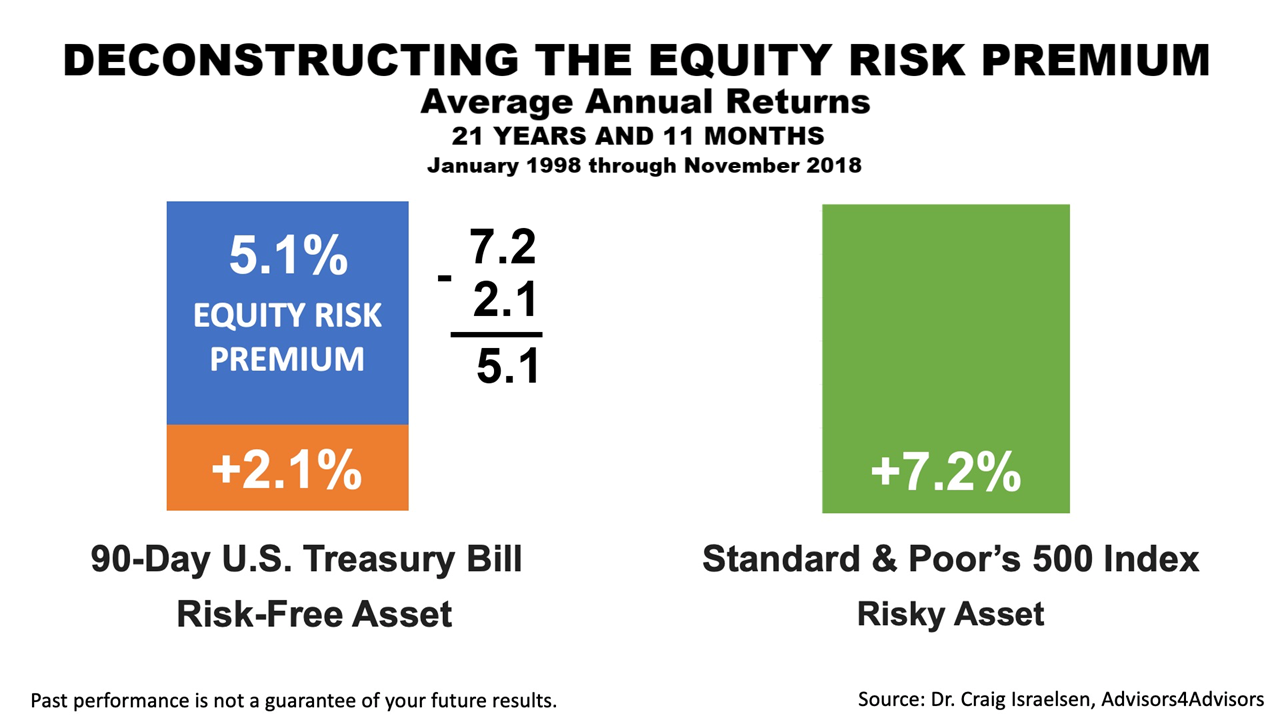

To quantify the risk premium for owning U.S. stocks, here are the numbers:

Over the 21 years and 11 months ended in November 30th, 2018, the risk-free 90-day U.S Treasury Bill averaged an annual return of +2.1%, compared to a +7.2% annualized return on the S&P 500 stock index.

This period of nearly 22 years encompasses two full economic and bear market cycles - the tech-bubble bursting in 1999 and the global financial crisis of 2008 - so it illustrates the equity premium through the best and worst of times.

Though past performance does not guarantee your future results, looking at the numbers lays bare crucial investment facts.

Click image to enlarge

The difference annually between the +7.2% average return on the S&P 500 index and the +2.1% return on a risk-free T-Bill was 5.1%.

To be clear, the extra return annually averaged on America's 500 largest publicly-held companies in the 21-year, 11-month period ended November 30th, 2018 - is the equity risk premium, 5.1%.

If uncertainty about the future were to somehow miraculously disappear - and we had perfect knowledge of what was about to happen - the equity risk premium would disappear. You would not get paid a premium for taking a chance on U.S. stocks rather than investing in Treasury Bills.

Click image to enlarge

Uncertainty about the future is a permanent condition. Successful long term investing means not just accepting perpetual uncertainty, but welcoming it. Wise investors are thankful for the uncertainty!

Click image to enlarge

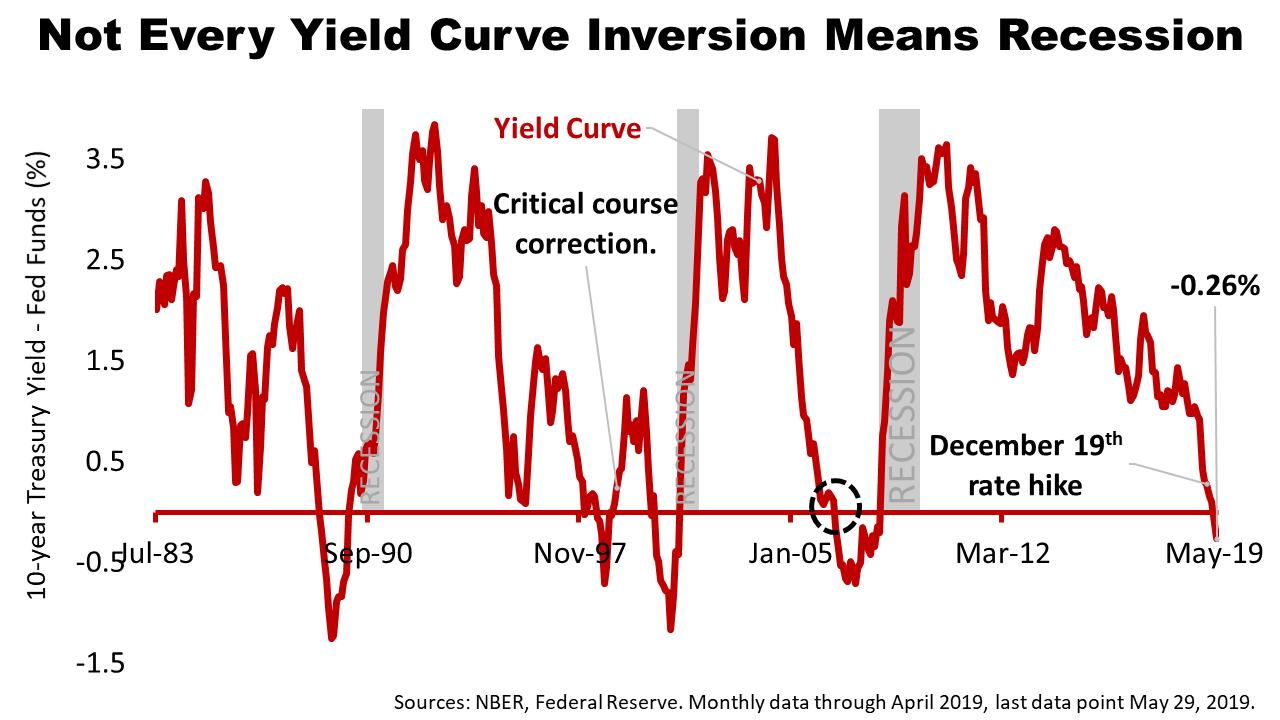

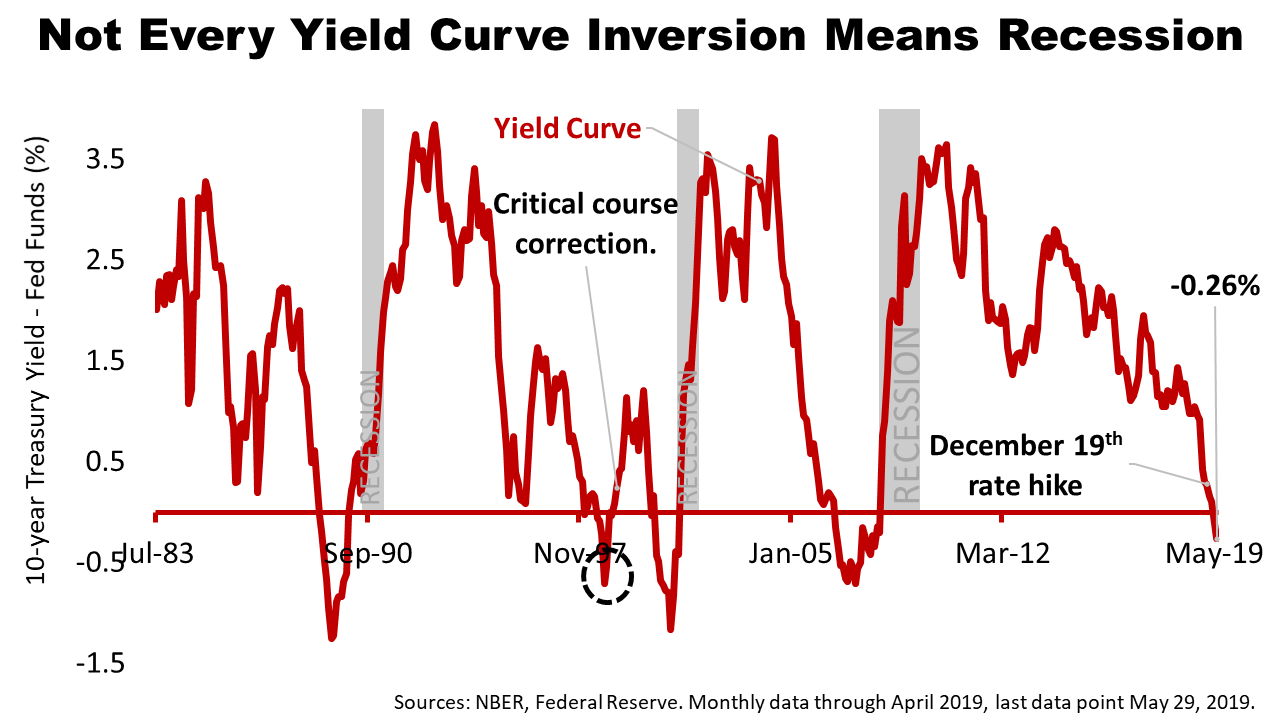

The biggest financial news of the second quarter was the inversion of the yield curve on May 14th.

Because inversions preceded every recession since 1954, it made investors nervous.

Let's try to end any confusion you may have about the yield curve. We can do it in a under two minutes - promise!

Click image to enlarge

The yield curve is the difference between the rate at which the Fed lends to banks and the rate on a 10-year U.S. Treasury bond.

The Fed lends money to banks at the three-month T-Bill rate and banks lend it to businesses at a higher, longer-term rate.

The inversion eliminates a bank's incentive to lend, which causes a general decline in economic activity.

Click image to enlarge

The last yield curve inversion was in July 2006.

Fifteen months later, in March 2007, The Great Recession began.

Click image to enlarge

So we want to put the recent yield curve inversion in perspective by emphasizing that, not every yield curve inversion causes a recession.

Click image to enlarge

For example, in June 1998, policy, shown in the dotted black circle, the yield curve inverted and it prompted the Fed to reserve policy.

Swift action by the Fed enabled the 1990s expansion to roll on for nearly three more years.

The same thing could happen again.

Click image to enlarge

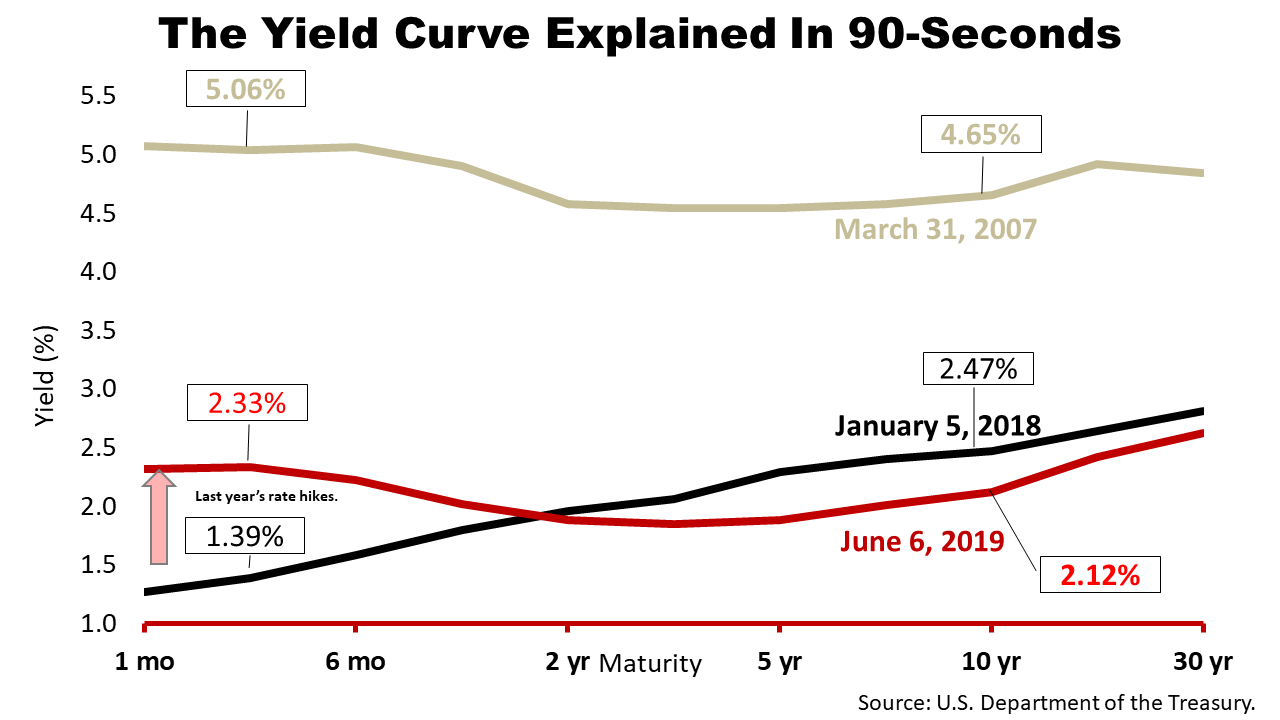

This chart shows the yield curve at three different dates.

The black line shows when the yield curve was steep and healthy, when the three month Treasury Bill yielded 1.39% versus the 2.47% on a 10-year Treasury Bond.

That's the way things should be: long term bonds pay a higher yield than shorter term issues because you're locking up your money and get paid a premium for taking that risk.

When the yield curve inverts, it means short-term Treasury Bills are yielding more than long-term bonds.

The gold line shows the last time the yield curve inverted, in March 2007, presaging The Great Recession. Then, the yield on a three-month Treasury bill was 5.05% versus the 4.65% on a 10-year Treasury Bond.

Finally, in red we've shown the yield curve as of June 6 2019, when the three-month Treasury bill recently was yielding 2.33% versus 2.12% yield on a 10-year Treasury Bond.

Click image to enlarge

Less than three weeks after the May 19 inversion, in a June 4th speech, the chairman of the Fed, Jerome Powell, did a complete about-face on the Fed's interest-rate policy.

Following a breakdown in U.S.-China trade talks and an announcement by President Trump of a plan to tax imports from Mexico, the Fed's reversal reassured markets.

Not a month had passed since the Fed had said it would planning to hold rates steady.

The Fed's policy change came after signs growth was slowing.

Click image to enlarge

One clear signal came from the Atlanta Federal Reserve's real-time forecast.

It plunged from a 3.1% growth rate in the first quarter of 2019!

By mid-June, the GDPNow forecast for second-quarter growth was slashed in half to 1.5%.

To be clear, the first quarter growth rate plunged by more than 50%!

Growth was slowing.

Click image to enlarge

Keep in mind, slower growth is not a recession.

Often in the media, slowing growth is confused with a recession.

As the third quarter began, the economy was still growing but at a slower rate.

Click image to enlarge

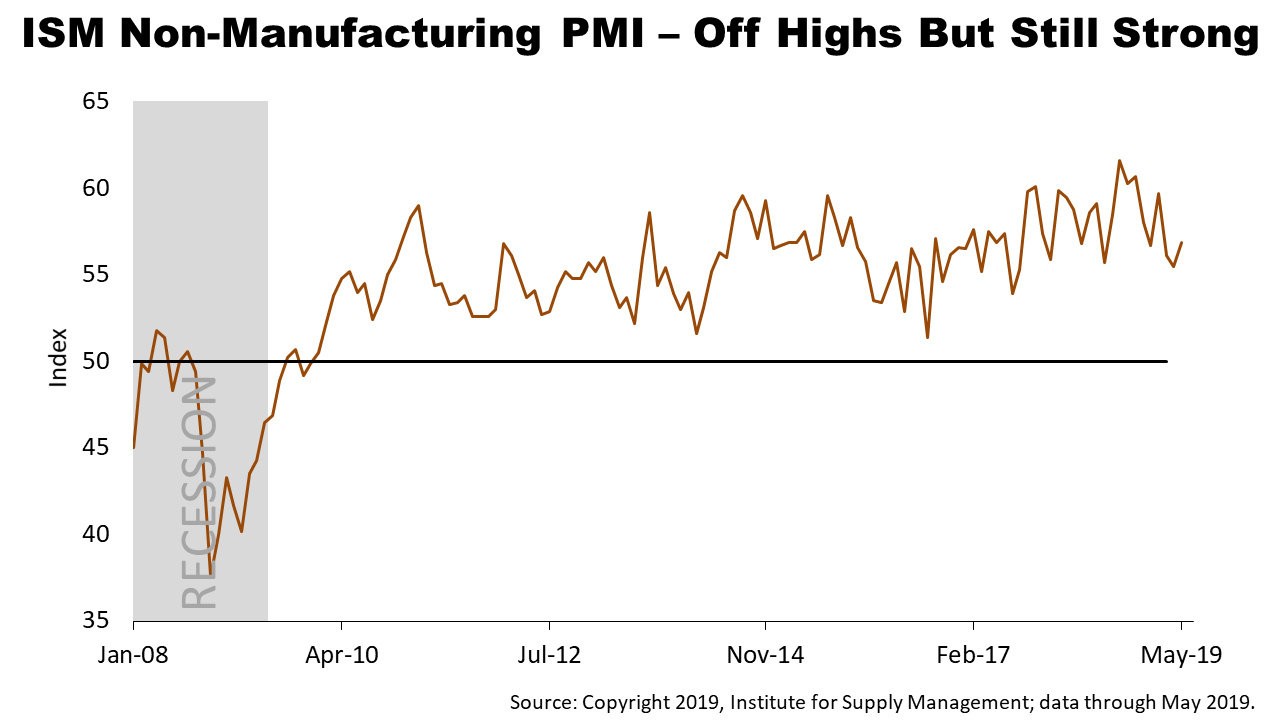

Not all fundamentals weakened in the second quarter.

An important indicator, the Institute for Supply Management's index of purchasing activity at non-manufacturing companies, ticked up in May, to 56.9.

Since non-manufacturing accounts for about 88% of U.S. economic activity, that was good news.

Click image to enlarge

As July Fourth closed in, amid a wave of crosscurrents, The Great Expansion entered its eleventh year.

From the depths of The Great Recession, a range of key indicators extended the star-spangled growth cycle, officially making it the longest expansion in U.S. modern history.

Click image to enlarge

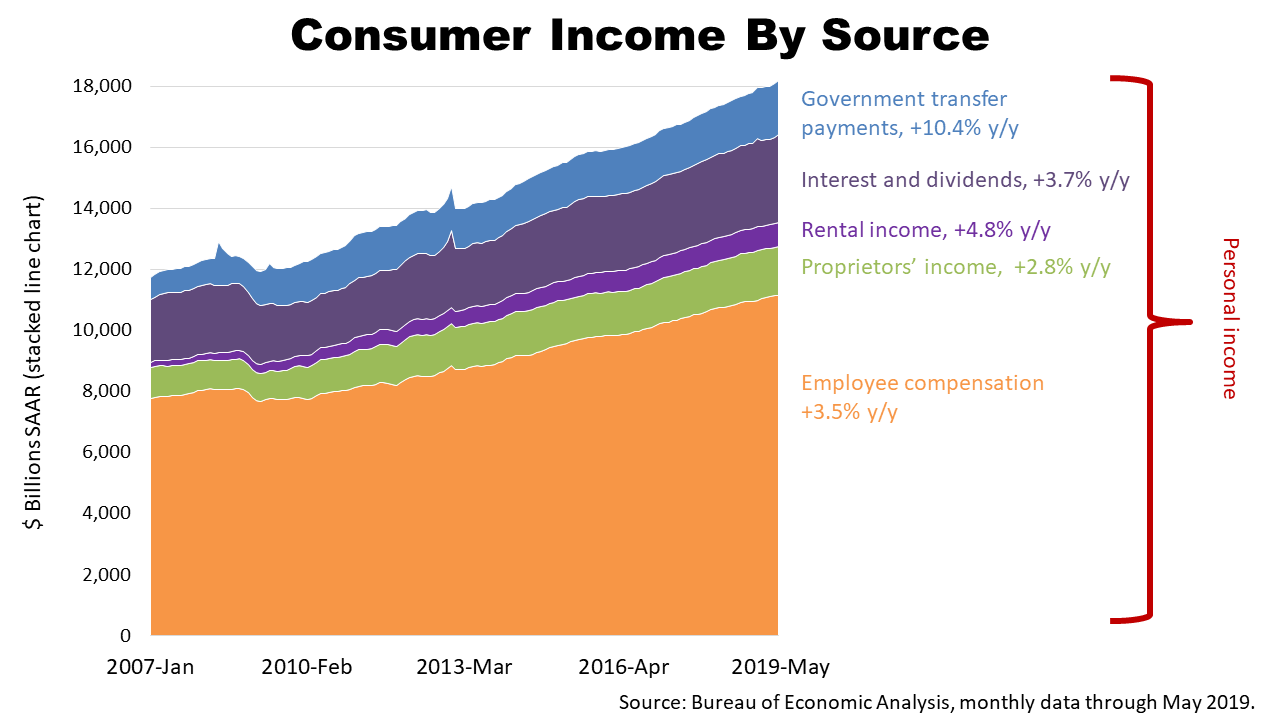

Consumer income, which drives of 70% of growth, rose at a strongly and broadly, over the 12 months ended May 31st, at a 4.1% annualized rate.

Personal income is mostly comprised of wages and benefits paid to employees, shown in orange here, but also includes interest, dividend, proprietor and rental income, as well as payments from Social Security, Medicare, and other government programs.

All categories of income tracked by the government grew at a strong rate in the 12 months through May 2019.

Real disposable personal income, after inflation and taxes, rose by +1.7% in the 12 months through May.

That's about as good as the peak five-year growth rate in real DPI in the last expansion.

May's +1.7% rate of growth in the amount consumers have in pocket available to spend was an improvement over April's +1.5%.

Click image to enlarge

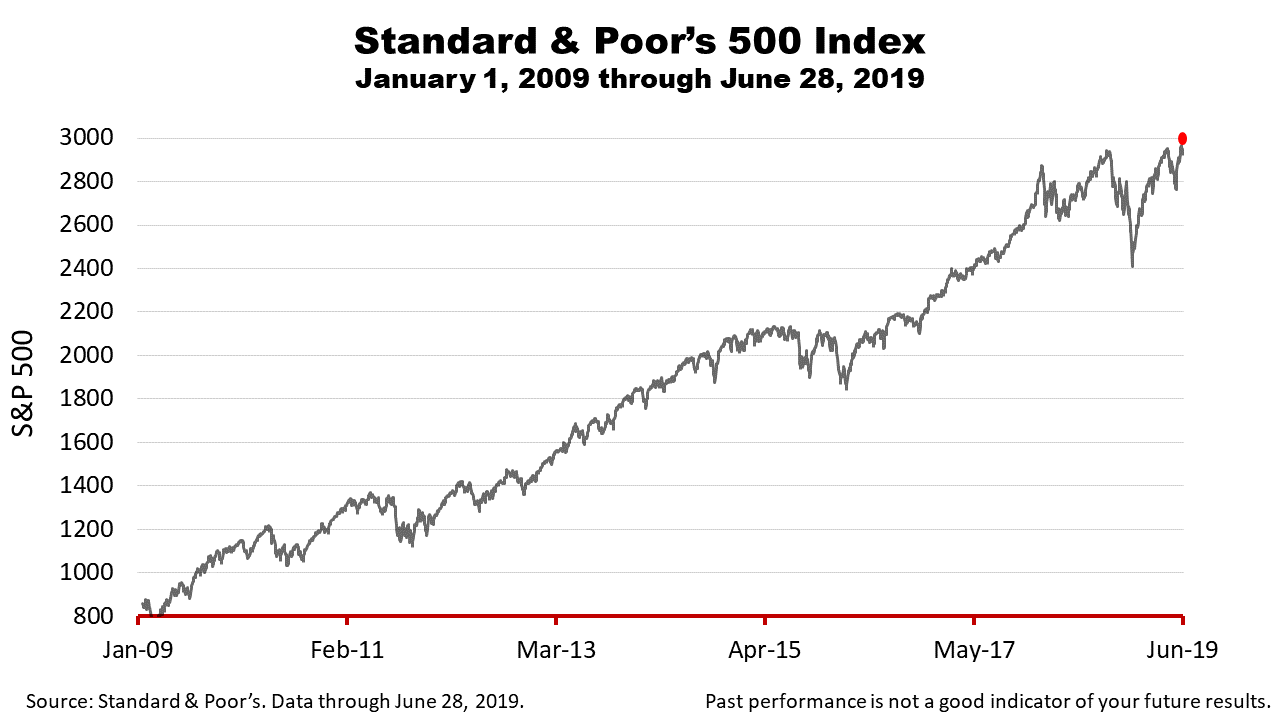

With the strength of the key drivers of the economy, share prices of American companies ended the quarter hovering around an all-time high.

Click image to enlarge

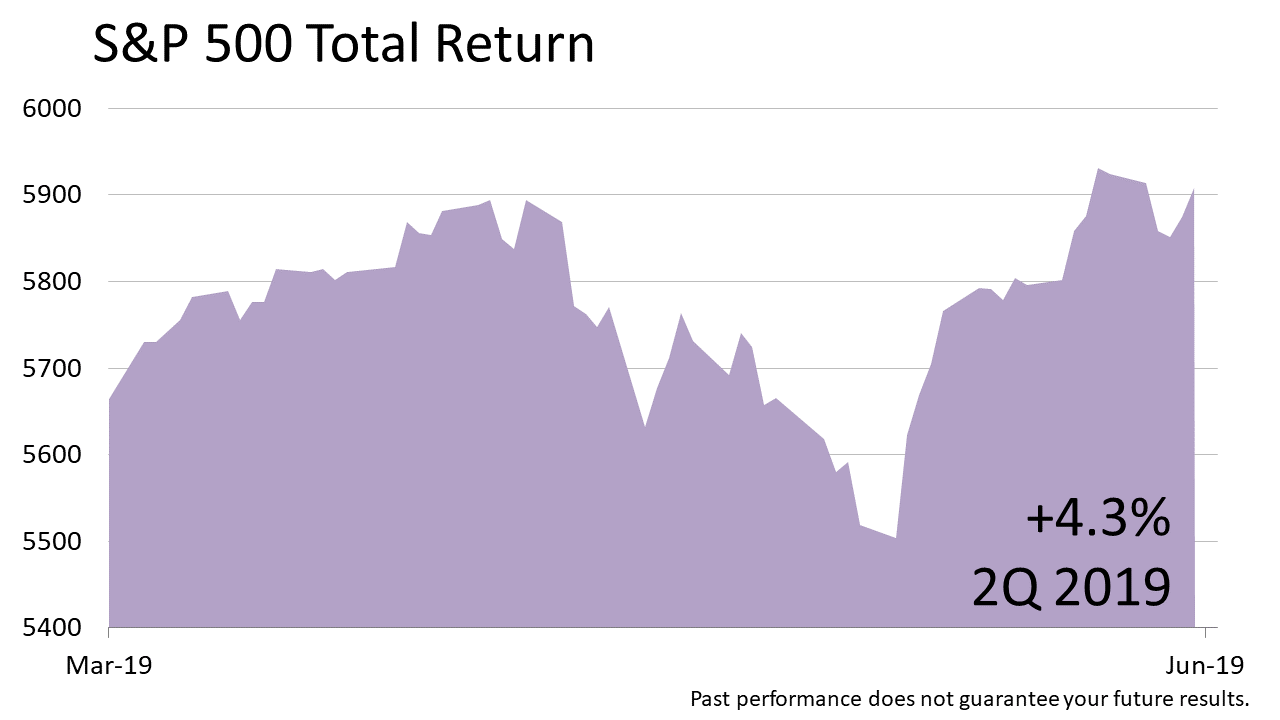

Stocks, as measured by the S&P 500, returned +4.3% in the second quarter of 2019 following the gigantic +13.7% return in the first quarter. The back-to-back growth completed a comeback from the humbling -13.5% loss sustained in the fourth quarter of 2018.

Click image to enlarge

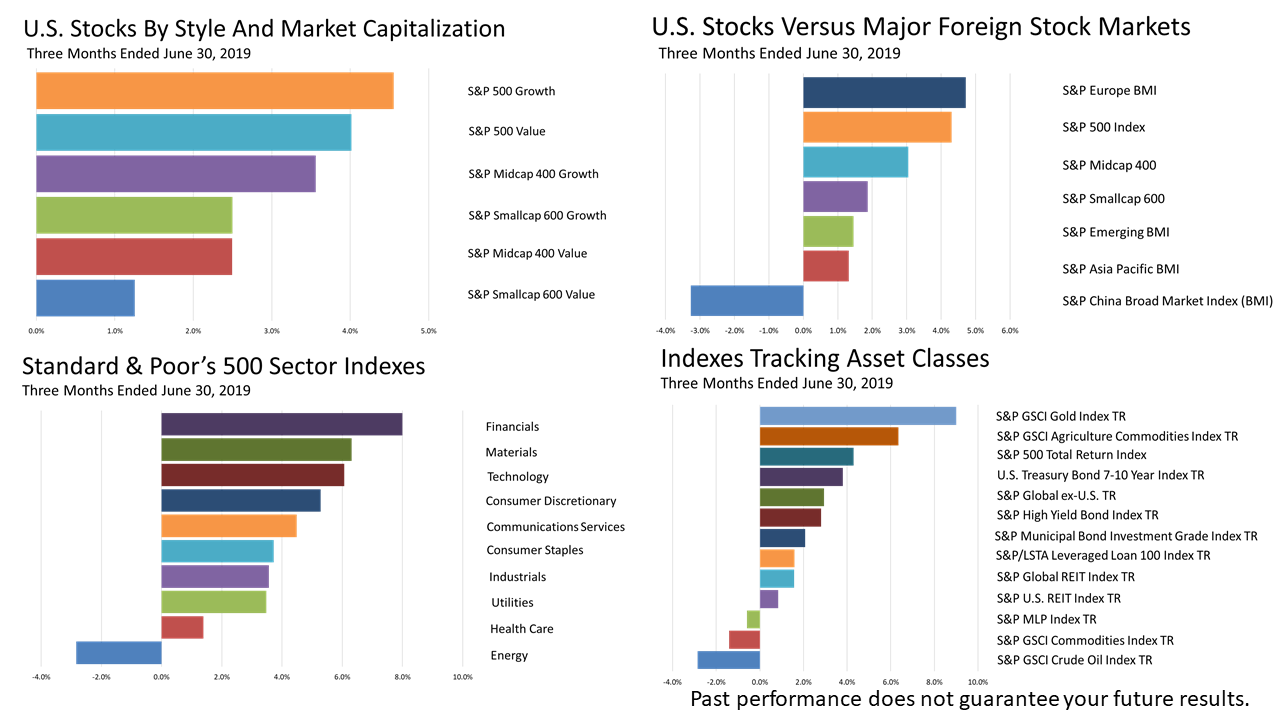

The four bar charts shown here are a snapshot of what happened in the three months ended June 30th, 2019.

Short term trends don't matter much to long term investors, but it's helpful to look at this group charts to spot new longer-term trends.

Beyond the outsize return on the S&P 500, some of the performance results that stand out include the fact that:

European stocks returned slightly more than the S&P 500

oil continued to be a poor asset class

large growth companies continued to be favored among the different types of U.S. stocks

China's fledgling stock market lost more than 3%

Click image to enlarge

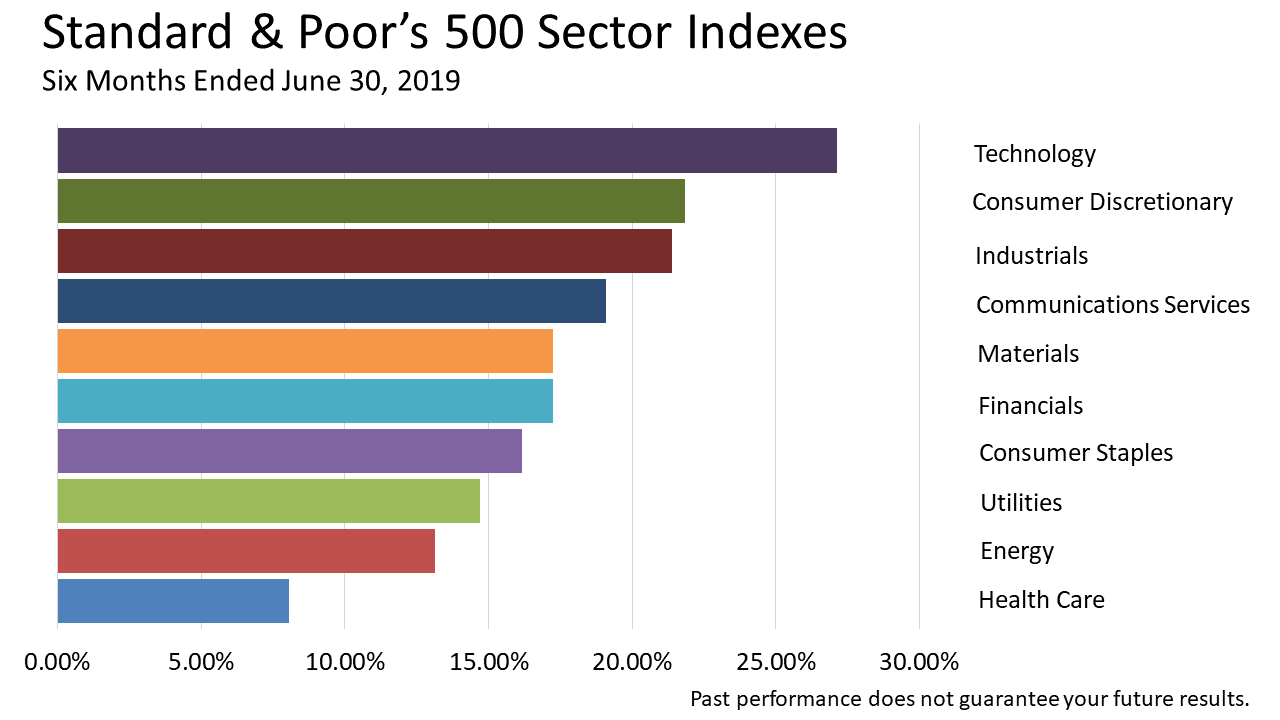

For the first half of 2019, the Standard & Poor's 500 index posted an +18.5% return.

That packed almost two years of returns into this six month period!

It was particularly timely in the aftermath of the stinging -13.5% loss of the fourth quarter of 2018.

Since almost no one ever remembers what happened in the stock market from one month to the next, let's remember that, in December 2018, a flash bear market drop of -19.8% occurred in reaction to a Federal Reserve rate hike amid the onset of a trade war with China.

Click image to enlarge

Since the era of the modern stock market began in 1926, large American company stocks annually averaged a return just less than 10%.

In just the first six months of 2019, share price appreciation on the S&P 500 and dividends totaled a +20.2% return, which is pretty spectacular.

Click image to enlarge

Tech stocks led the way in the first of the year, with a +21.7% return.

Consumer discretionary stocks were the runners up in this 40th consecutive quarter of the bull run, on the cusp of eclipsing the 10-year economic expansion in financial history.

Real disposable personal income has grown steadily for several years and consumer discretionary stocks would seem to have capitalized on the trend.

Click image to enlarge

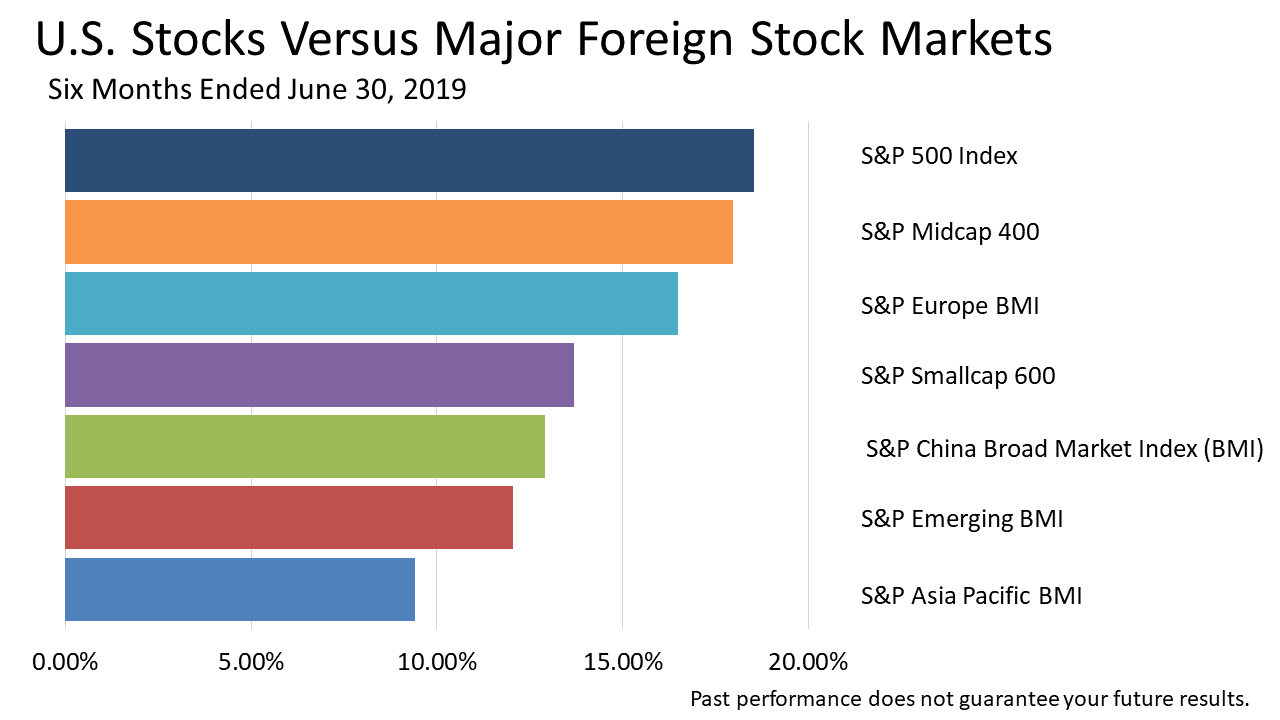

In the first half of 2019, U.S. stocks led the performance along a broad swath of regional global stock market indexes.

Keep in mind, global growth was jolted toward the end of this six month period, as fear of a trade war between the U.S. and China grew.

Click image to enlarge

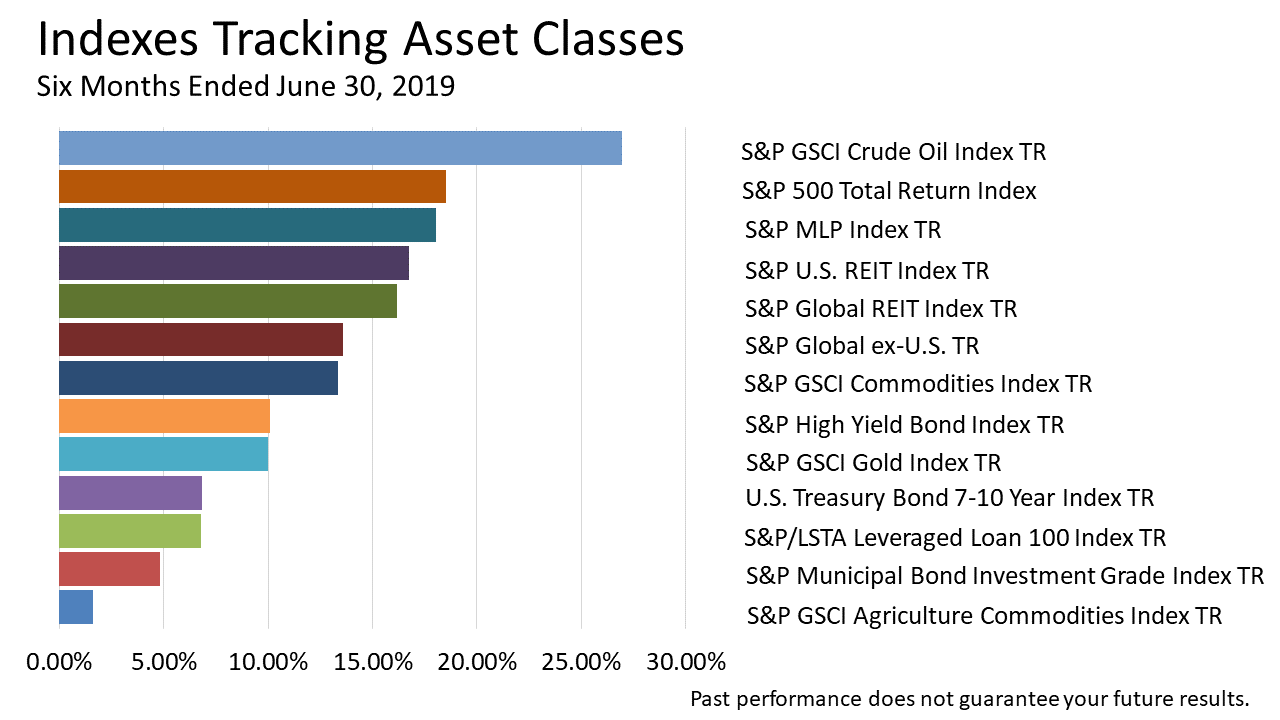

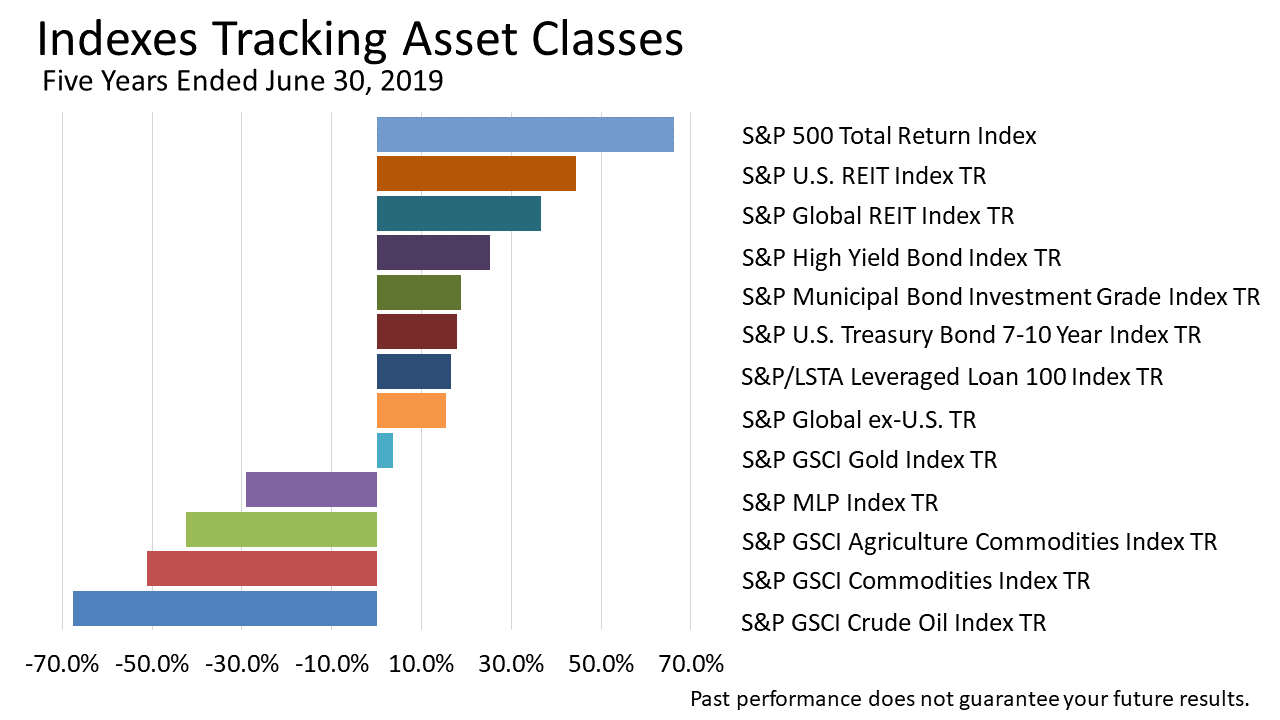

The volatility of oil prices is nothing new, but the strong return on U.S. stocks in the first six months of 2019 relative to 12 other asset classes is notable.

Click image to enlarge

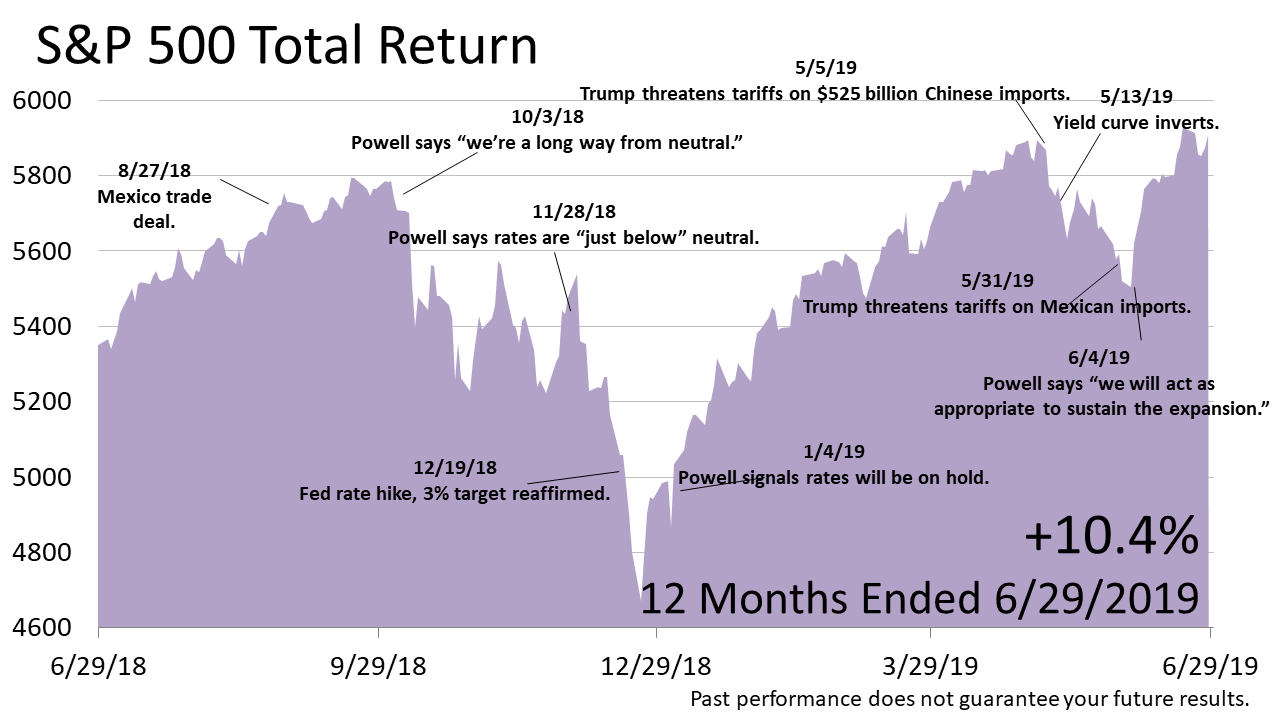

The 12 months ended June 30th, 2019 make for a dramatic picture and it has had a happy ending.

The S&P 500 hit a record all-time high on September 20th, 2018. However, on Christmas Eve low, after the Fed reaffirmed its plan to raise the fed funds target rate to 3% in 2019, stocks nosedived -19.8%.

Investors sold stocks because hiking the short term rate to 3% would lead to an inverted yield curve, which has been the key precursor to every recession in the post-WWII era.

Less than three weeks after its December 19th rate hike, the Fed signaled, on January 4th that it would no longer pursue rate hikes to its previously announced 3% target.

By May 14, 2019, however, the yield curve inverted. Coupled with President Trump's threat to impose tariffs on Mexican imports, the news sent stocks tumbling -6.9% from their April peak.

Abruptly, President Trump backed off from his Mexico tariff threat and Chairman Powell reaffirmed in June that he Fed will "act as appropriate to sustain the expansion." Seeming satisfied with the turn of events, stocks hit a new record all-time high late in June.

Click image to enlarge

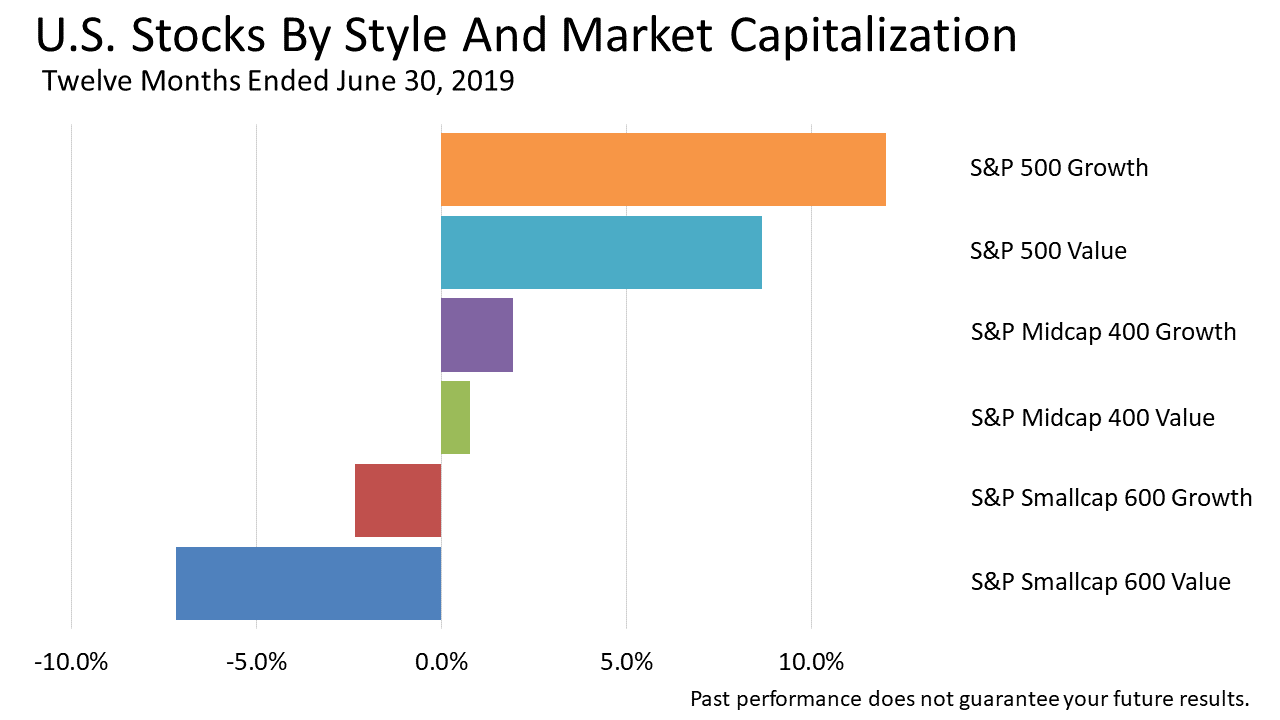

Large company growth stocks were favored in the 12 months ended June 30th, 2019.

Small value stocks were still net losers in this 12-month snapshot.

Click image to enlarge

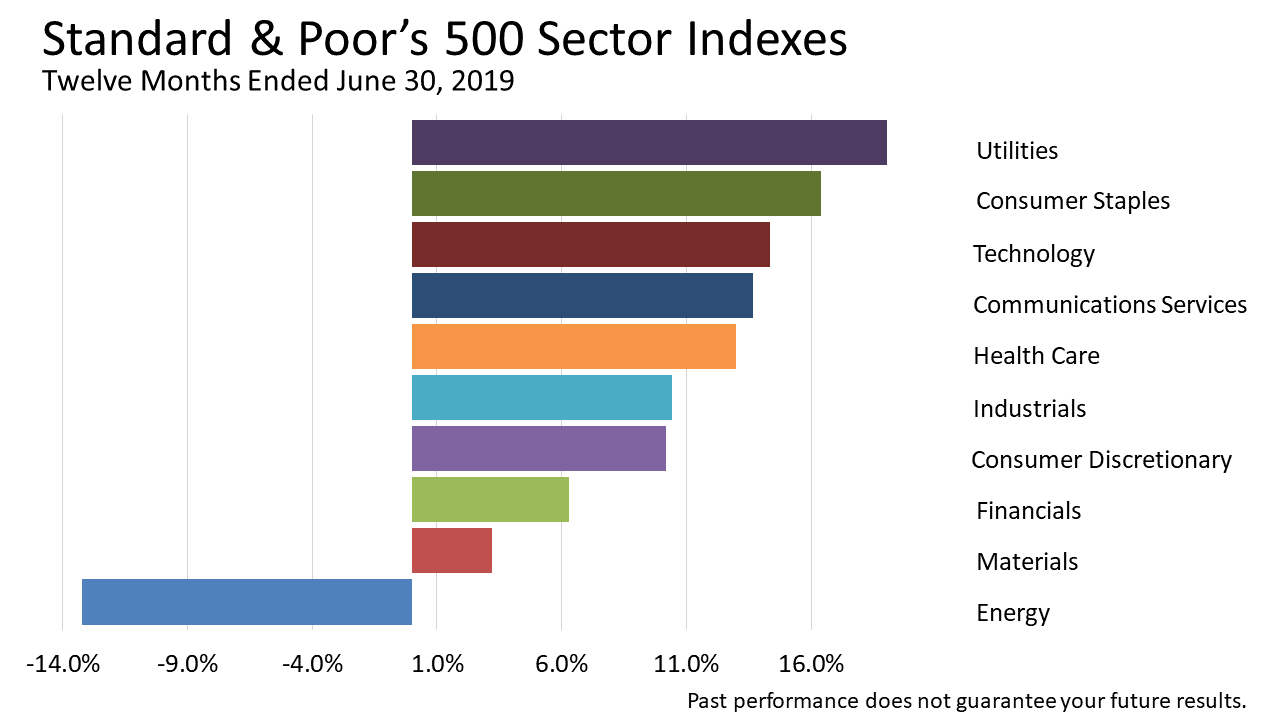

Nine of the 10 S&P 500 industry sectors returned a profit in the 12 months ended June 30th, 2019.

Energy stocks lost -13.2% in this one year period, but it was the only losing industry among the sectors.

Click image to enlarge

U.S. stocks, over the 12 months ended June 30th, 2019 showed a total return of +10.4%. But the one-year period was interrupted by a bear market drop.

Despite the wild ride, U.S. stocks for the 12 months far outperformed other major stock markets across the globe.

Emerging market stocks returned +3.1% and European bourses gaining +1.6%. While Asia Pacific stock markets were thrown for a -2.7% loss, and the fledgling Chinese stock market dropped in value by -7.1%.

The world stock markets were influenced largely in this 12 month period by the looming trade war between the U.S. and China. The threat of an economic slowdown in China, the world's manufacturer, reverberated across Asian markets. China's economic fortune depends much more on exports to the U.S. than the U.S. depends on China. Loss of trade with China could be expected to shave annual U.S. gross domestic product by two-tenths of 1%, according to independent economist Fritz Meyer.

Click image to enlarge

After trading sideways for approximately two years in 2015 and most of 2016 - hitting two air pockets along the way - the stock market broke out after the November 2016 election. Share prices rose fairly steadily to an all-time peak on September 20, 2018, whereupon the blue-chip index of America's largest public companies, plunged by -20% to a Christmas Eve low on investor fears that an inverted yield curve was imminent.

Over the last five years, including dividends, the S&P 500 total return index has gained +66%, as illustrated in this chart, compared with a gain of +50% for the commonly quoted S&P 500 price index. The 16-percentage point difference being dividends reinvested. The five-year gain of +66%, or +13.2% per year, is substantially greater than the stock market's long-term annual total returns of approximately +10% going back 200 years as described by Wharton professor Jeremy Siegel in his seminal book, Stocks for the Long Run, first published in 1994.

Click image to enlarge

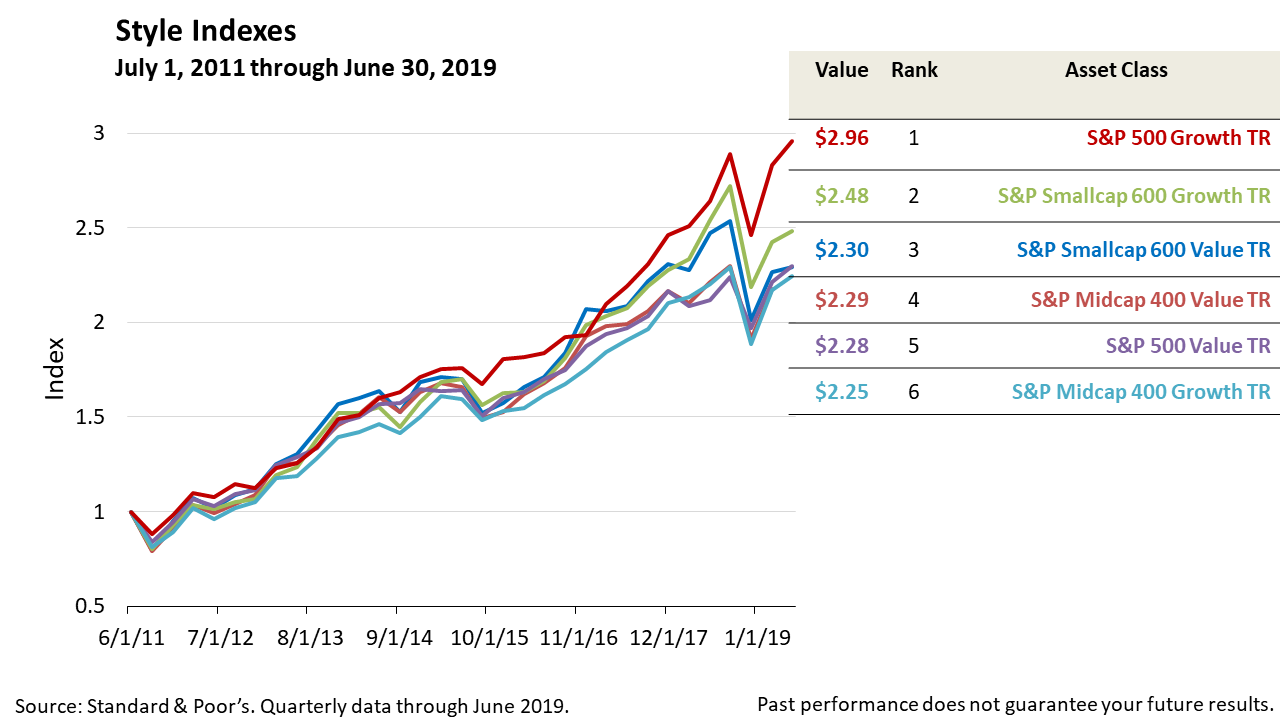

Growth stocks have outperformed value stocks. The difference in performance in styles of investing in vogue is more dramatic in this snapshot than usually seen over a five year period. This is why diversifying is important, to avoid underweighting or overweighting any single style or type of investment.

Click image to enlarge

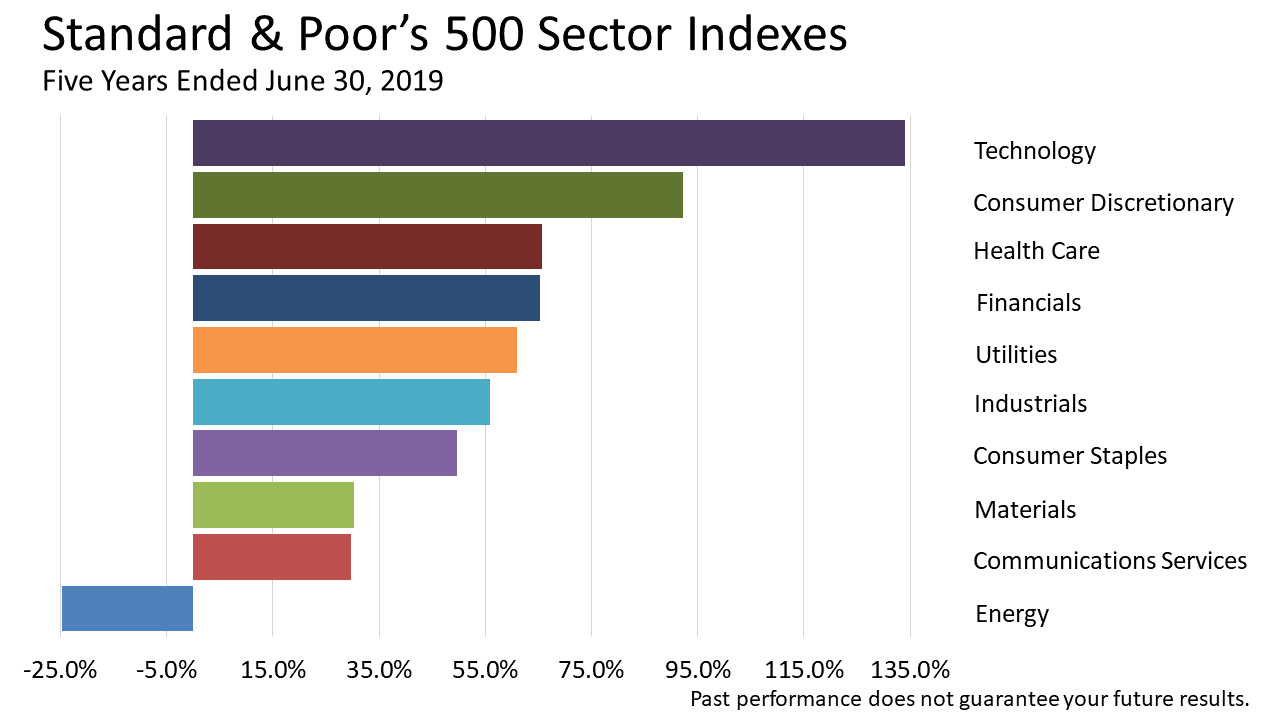

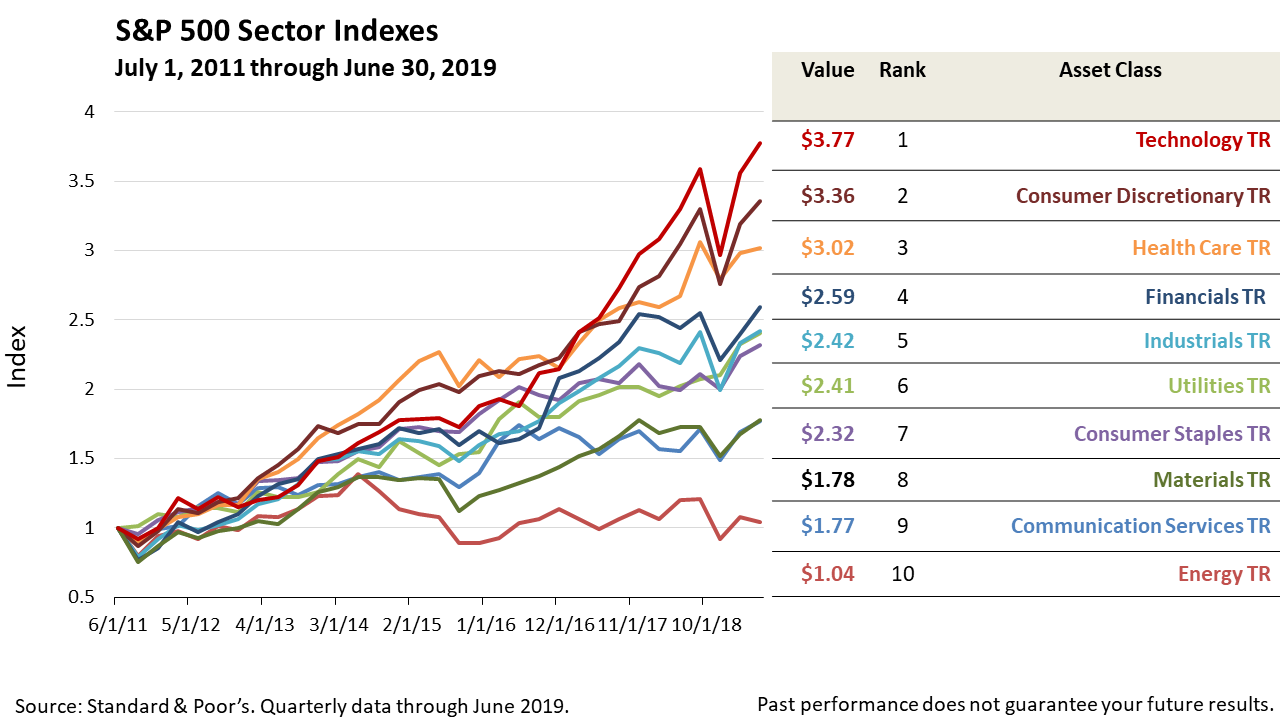

As is to be expected in an economic expansion, stocks with the best growth prospects led the results of Standard & Poor's industry in the five-year period ended June 30th, 2019. That's why technology stocks in the period, including dividends as well as share-price appreciation, returned +134%.

With real wages growing strongly for the five year period, Americans' have more money in their pockets to spend, which propelled consumer discretionary stocks to a +92.3% total return in the five years shown.

Click image to enlarge

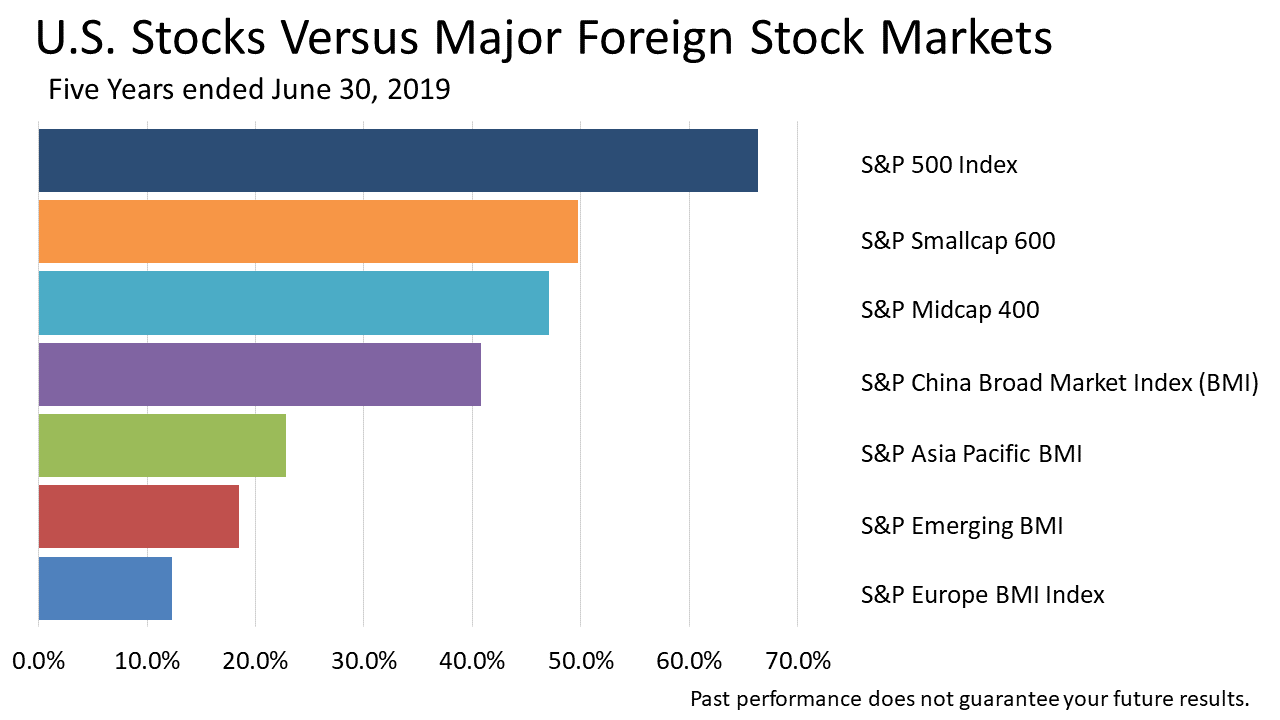

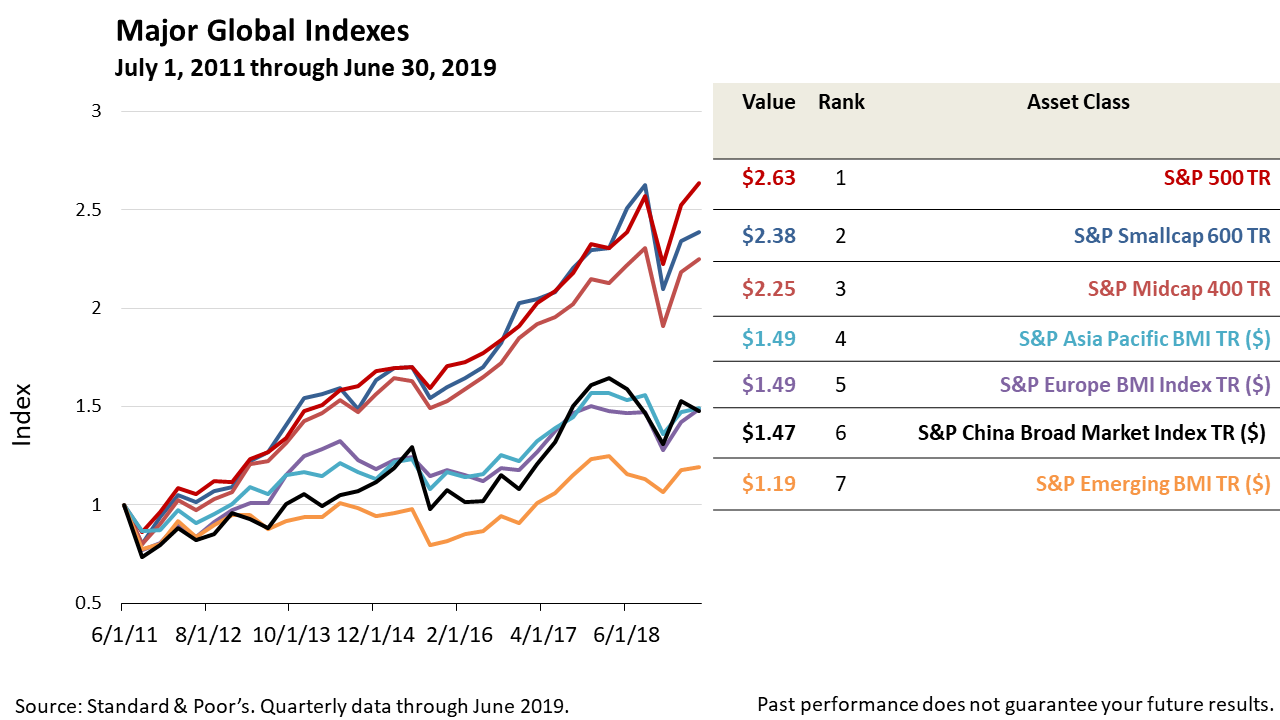

European stocks were the laggards over the five years ended June 30, 2019, returning +12.3%, as Europe's economic growth rate trailed other world regions. The five-year return on the Standard & Poor's 500 was +66.3%, as the second five years of the 10 year bull market and expansion rolled on.

Click image to enlarge

Click image to enlarge

Click image to enlarge

Click image to enlarge

Click image to enlarge

Click image to enlarge